Burial Insurance and Final Expense: The Complete Guide

Also called final expense or funeral insurance — what this whole life insurance covers, what it costs, who it fits, and how to buy it right.

If you’re looking into burial insurance — also sold as final expense insurance — you’re asking one quiet question: when I’m gone, will the people I love be okay, or left scrambling to find the money for my funeral?

Here’s the gap. A funeral with viewing and burial runs about $8,300 (National Funeral Directors Association), while the typical family keeps about $8,000 in checking (Federal Reserve), so one funeral can wipe out a family’s ready cash in a week — and 58% of adults say they’d have to borrow to cover it (CardRates). A final expense life insurance policy closes that gap, so the people you leave behind get to grieve instead of fundraise.

- Burial insurance, also called final expense insurance, is a small whole life insurance policy built to cover funeral and burial costs and other final bills. It never expires, and the premium never goes up.

- No medical exam. Most policies ask a few health questions, and some ask none at all.

- A funeral with viewing and burial runs about $8,300, according to the NFDA — and that’s before the cemetery, which can add a few thousand more.

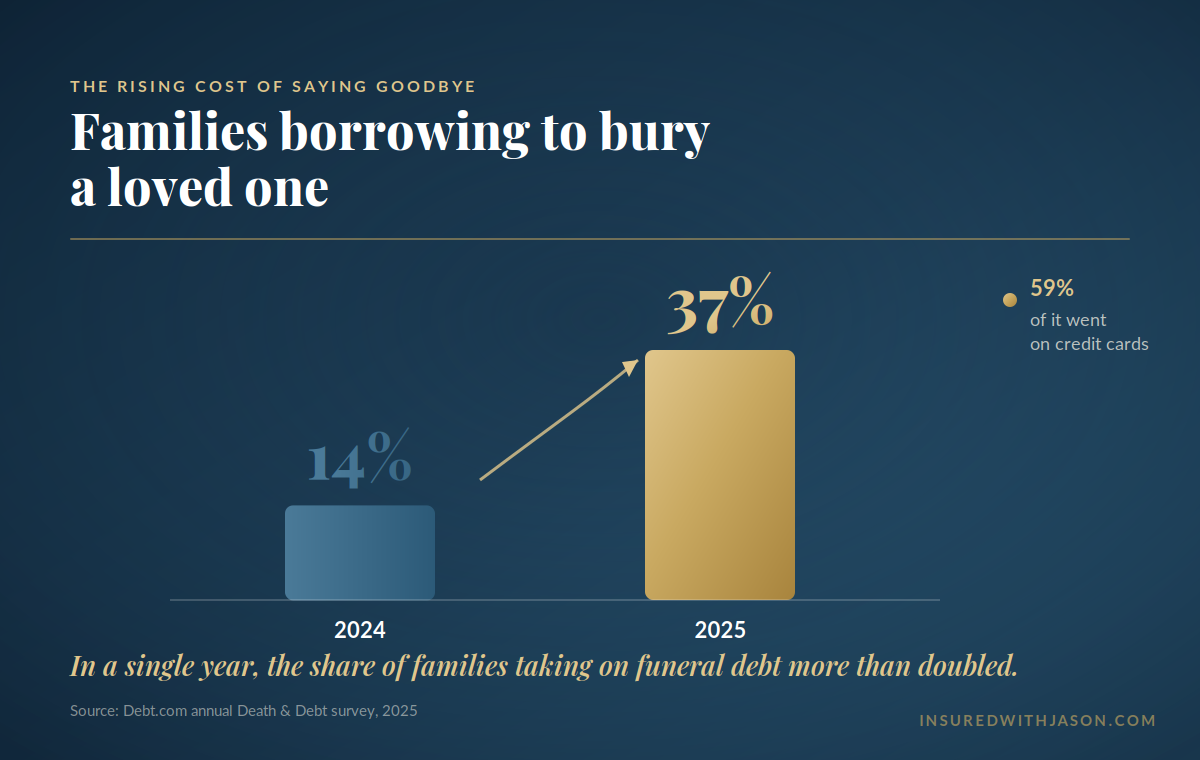

- The need is real and growing: 37% of families took on debt to bury a loved one in 2025, up from 14% the year before (Debt.com).

- You can get covered with health conditions. Diabetes, high blood pressure, even past cancer often still qualify for coverage that starts right away.

- There are four types of burial insurance, sorted by your health. The healthier you are, the lower the cost and the sooner the full benefit is payable.

- You don’t need perfect health for the best rate. A good broker compares the best burial insurance companies and finds the one that treats your condition as its lowest risk.

- The money goes to a person you name, tax-free, usually within days, to spend on whatever the family needs most.

- Buying earlier costs less. Your rate is set by your age the day you start, and it’s locked there for life.

What Is a Burial Insurance Policy?

Burial insurance is a small whole life insurance policy designed to help cover funeral and burial costs, and to cover funeral and other final expenses at the end of life. You’ll also hear this type of life insurance called final expense insurance, funeral insurance, or burial life insurance. Whether you call it burial or funeral insurance, burial and funeral insurance, or something in between, it’s the same product wearing different names, so don’t let the wording trip you up.

Two words do the heavy lifting. Whole life means the coverage is permanent life insurance: it never expires as long as you pay, so it can’t run out before you need it. And small means the benefit is modest on purpose — usually between $2,000 and $25,000, where regular life insurance policies might be ten times that. You’re not insuring a mortgage here. You’re covering a funeral.

Here’s how it works. You pick a coverage amount, you pay a fixed premium, and you name a beneficiary — the person who receives the money. When you pass, that person files a short claim with a copy of the death certificate, and the insurance company pays them a tax-free lump sum, usually within days. There are no strings on the money: they can put it toward the funeral, the cemetery, a leftover medical bill, or whatever the family needs most. In short, burial insurance is designed to cover the cost of your funeral — a type of life insurance policy you keep for life, quietly handling a bill your family would otherwise face alone.

And because the benefit is small, the company keeps the application simple. Most policies ask a few health questions and skip the medical exam entirely.

One quick comparison, because people ask. A term life policy is like renting coverage for a set number of years — cheap while it lasts, but it expires, and if you outlive it you’re left with nothing. Burial insurance is yours for life. Since a funeral is the one bill every one of us is guaranteed to have someday, permanent coverage is the piece that fits.

Key burial insurance terms, explained

What Does Burial Insurance Cover?

Because it pays cash to a person instead of paying a bill directly, it can cover just about anything. There are no rules on how your beneficiary spends it. In plain terms, burial insurance can help cover funeral and burial costs — and the funeral and other final expenses that follow a death — with the money going straight to the person you name. That said, it’s built for the final expenses that hit when someone dies, and those are the ones most people have in mind.

The funeral and cemetery itself

The funeral home’s basic service fee, moving and preparing the body, the casket or urn, the viewing, the service, and transportation. Then the cemetery, which is a separate bill: the plot, the vault most cemeteries require, the headstone, and the fee to open and close the grave. Together these are the funeral and burial expenses people picture first.

The bills and gaps that come with it

Leftover medical or hospice bills, a small credit card balance, legal or probate costs, even travel for family coming in from out of town. Many people also size their coverage a little higher on purpose — to give the son or daughter handling the arrangements room to take a few days off work, to cover a small debt they’d rather not leave behind, or simply to leave their loved ones a thank-you. That’s a personal call, and a good one to think through.

What it’s not built for

Burial insurance isn’t meant to replace years of income, pay off a mortgage, or put kids through college. Those are big jobs for a larger term or whole life policy, or a traditional whole life insurance policy. This is a focused tool for a focused set of final expenses.

The flexibility is the quiet advantage. Because the money goes to your family and not to one specific funeral home, they get to choose where and how to lay you to rest, and they can shop around if they need to. Either way, burial insurance helps loved ones cover the burial expenses and the broader funeral and burial expenses without draining what savings they have.

Burial insurance pays cash to the person you name — who can use it for the funeral, the cemetery, and any final bills.

How Much Does Burial Insurance Cost?

The honest answer is that how much it costs depends on two things: what fits comfortably in your budget, and how much you want to cover. Anyone who throws a flat number at you before asking about either one is guessing. Burial insurance offers life insurance coverage built as insurance for final expenses — think of it as insurance for funeral costs and the bills around them, not income replacement. So let me give you the real way to think about it.

Start with what you can comfortably set aside each month. Some coverage is far better than none. I’d rather see you protect your family with a smaller policy you’ll keep for life than stretch for a big one you might have to drop. Pick a payment that fits your monthly income and won’t feel like a strain a few years from now.

Then think about how much you actually want to cover. For some people that’s just the funeral. For others it’s the funeral plus a cushion — a few days of missed work for whoever handles the arrangements, a small debt, a little left over as a thank-you. There’s no wrong answer here, only your answer, and it usually takes a real conversation to land on it.

As a general range, a burial or final expense insurance plan often runs anywhere from around $30 to $40 a month on the lower end up toward $150 a month if you want to cover more. Where you land comes down to your age, your health, the company, and the coverage amount you choose — which is exactly why a number off a chart isn’t worth much until we’ve talked about you.

Younger and healthier costs less — but here’s the part most people miss. You do not have to be in perfect health to get the best rate. Companies grade conditions differently, and a good independent broker’s real job is to compare the best burial insurance companies and find the highly rated one that already treats your condition as part of its lowest-risk group. When that match is made, you can get day-one coverage at the best discount instead of settling for a generic policy that skips the health questions and makes everyone wait.

A funeral averages around $8,300, and it lands on a family within days. A steady monthly payment means they never have to scramble to find it.

How Much Burial Insurance Coverage Do You Need?

Enough to cover the kind of send-off you want, plus a small cushion. The trick is to build that amount up from the actual bill, not down from whatever an ad is selling. Start with what you’re really planning.

If you’re planning a traditional burial, start with the median cost of a funeral with viewing and burial — about $8,300, according to the NFDA — then add the cemetery: the plot, the vault, the headstone, and the fee to open and close the grave. Add a vault and the NFDA puts the cost of funeral services closer to $9,995, and the cemetery items push it higher still.

If you’re leaning toward cremation, the math is gentler. The NFDA puts a full cremation service with a viewing around $6,280, and a simple direct cremation costs far less. About 63% of families now choose cremation, versus roughly a third who choose burial, and the NFDA expects cremation to top 80% by 2045 — so the type of burial or cremation you choose changes your number, and you may need less coverage than the burial figures suggest.

Then add a little cushion. Funeral costs creep up over time, and you may want a bit left over for the cost of final medical bills, a small debt, or a gift to your family. A little padding above today’s cost of funeral keeps the policy from falling short a decade from now.

A typical funeral now runs about $8,300 — roughly what the average family keeps in checking. That’s the gap burial insurance closes.

How to figure out how much coverage you need

Build the amount up from the real bill, not down from whatever an ad is selling.

- 1Start HereDecide: burial or cremation?

That single choice swings the cost of your funeral the most.

- 2Get The Real NumberAsk a local funeral home for an itemized price list

By law (the FTC Funeral Rule), they have to give you one when you ask.

- 3Don’t Forget ThisAdd the cemetery costs separately

Plot, vault, headstone, and the fee to open and close the grave.

- 4Build In RoomAdd a cushion

For any final bills, small debts, lost work for the family, and a few years of rising prices.

- 5SubtractTake out what you’ve already set aside

Savings or an existing policy earmarked for this.

- 6Your AnswerWhat’s left is your target coverage amount

That’s the number to shop with.

People size their policy to the funeral home’s bill and forget the cemetery is billed separately.

That’s how a family ends up with the service covered but comes up short on the burial. Count both from the start.

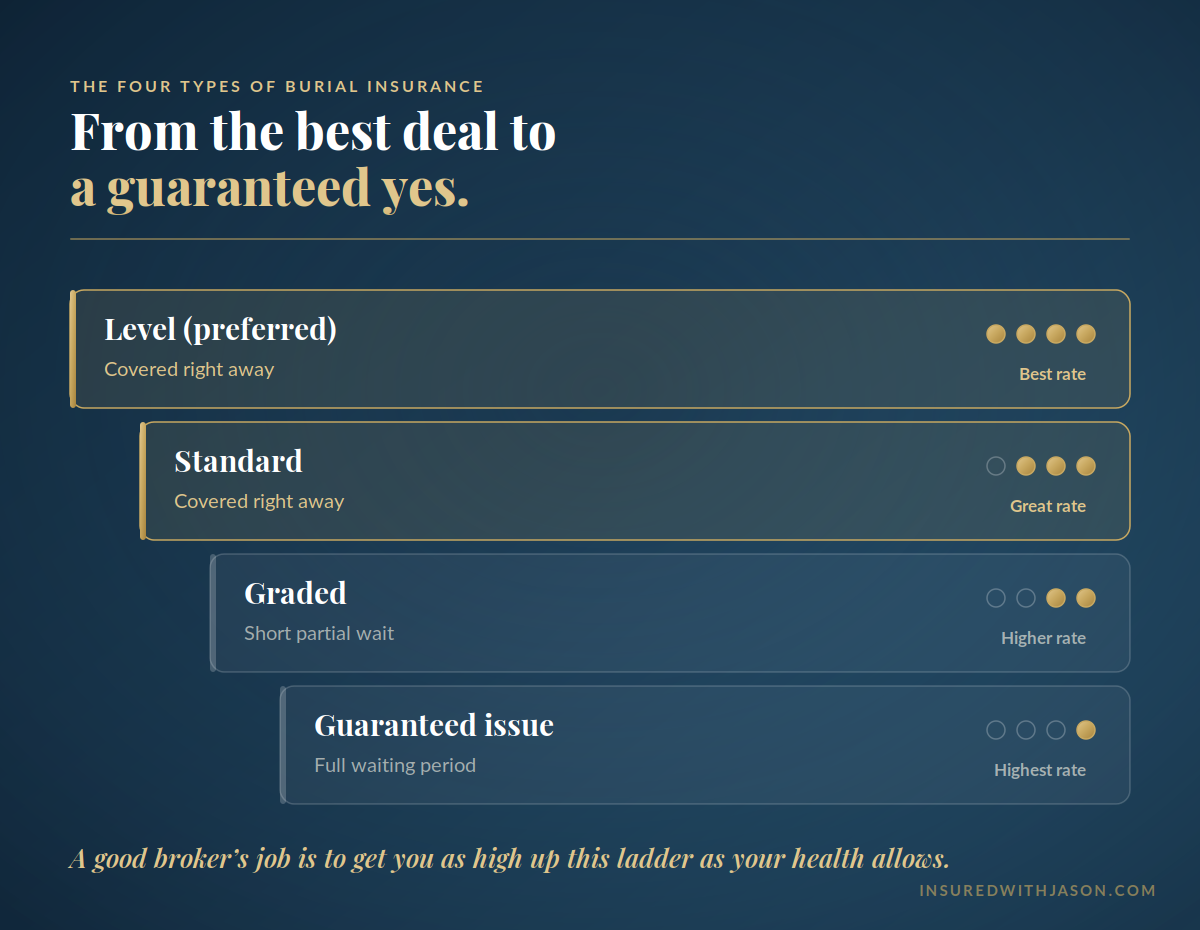

Types of Burial Insurance

There are four types of burial insurance, and which one you get comes down to your health. The healthier you are, the less you pay and the sooner the full benefit is payable. The key thing to understand across all four is the waiting period — whether the company pays the full amount right away, or makes you wait a couple of years first.

Level (preferred) coverage — no waiting period

The best tier, for people in good health who can answer no to most health questions. The full benefit is payable from day one, at the lowest cost for a given amount of coverage. There’s still no medical exam — just the questions and a records check.

Standard coverage — no waiting period

For people with minor, well-managed conditions. The full benefit is still payable immediately. The premium is a bit higher than level coverage.

Graded coverage — partial waiting period

For people with more moderate health issues. There’s a two-year waiting period, but it’s partial: if you pass from natural causes in the first couple of years, your family receives a portion of the benefit — often a smaller share in year one, more in year two, and the full amount after that.

Guaranteed issue life insurance — full waiting period

For people with serious conditions who can’t qualify any other way. There are no health questions and no exam — acceptance is guaranteed within the age range. The trade-off is a two-to-three-year waiting period for natural causes, during which your family gets all premiums back plus interest rather than the full benefit. Accidental death is often covered in full from day one. This tier costs the most for a given amount of coverage.

The four types of burial insurance, sorted by health — from day-one level coverage down to guaranteed issue.

Burial Insurance Features

Beyond the basic payout, a final expense insurance policy comes with a handful of features worth knowing before you buy. Most exist to make the coverage steady and predictable, which is exactly what you want for a bill this important.

Your premium never rises, and your benefit never shrinks. Whatever rate you start at is the rate you pay at 70, 80, and beyond. The company can’t raise it or cut your coverage as you age. As long as you pay, the policy can’t be canceled.

It builds a little cash value. A small savings amount grows inside the policy over time, at an interest rate spelled out in your policy. You can borrow against it in a pinch, though anything you borrow comes out of the benefit later.

Useful riders are often available. Many policies include a living benefit that lets you draw part of the money early if you’re diagnosed with a terminal illness. Some offer an accidental death rider that pays extra, or a small rider to cover children or grandchildren. Ask which ones come built in.

You can time the payment to your income. Many companies let you line up your premium with the day your Social Security deposit lands, which makes budgeting on a fixed income a lot simpler.

A handy safety net: some policies will quietly borrow from your own cash value to cover a payment you miss, so one rough month doesn’t wipe out years of coverage. Confirm whether yours does this before you count on it.

Does Burial Insurance Require a Medical Exam?

No — this coverage doesn’t require a medical exam. No blood draw, no urine sample, no nurse coming to your home. That’s one of the main reasons people choose this type of insurance. The company manages its risk a different way.

Here’s what happens instead. You answer a short set of yes-or-no health questions, usually on a quick phone call or online. The insurance company checks your prescription history and the Medical Information Bureau, a shared record of past insurance applications. From that, they can size you up without ever drawing blood, and a decision often comes back in minutes.

And if you can’t pass the questions, there’s still a door. Guaranteed issue policies ask nothing at all — no questions, no records check. You trade that for a higher premium and a waiting period, but coverage is there.

One important warning: answer the health questions honestly. During the first two years, the company can review a claim, and an answer that doesn’t match your records can cost your family the benefit. The truth always protects them better than a guess.

Can You Get Burial Insurance With Health Conditions?

Yes — and this is the part that gets me, because it’s where this coverage does its best work. This coverage was designed for older adults who can’t get traditional life insurance anymore. Having a health condition rarely shuts the door. It usually just decides which type of policy you start with.

The questions look back a set window, not your whole life. Most applications ask about the past 12, 24, or 36 months — not “ever.” So if you had cancer years ago and have been in remission past that window, you can honestly answer no and may qualify for coverage that starts right away.

Many common conditions still get day-one coverage: well-controlled type 2 diabetes, high blood pressure or cholesterol on medication, COPD depending on severity, cancer in remission past the lookback window, and a past stroke once enough time has gone by.

Some conditions usually mean graded or guaranteed-issue coverage instead: insulin-dependent diabetes, active cancer treatment, congestive heart failure, a recent heart attack, or kidney failure on dialysis. You can still get covered — you just start with a waiting period.

Here’s the truth most people never hear. Different life insurance companies grade the same condition differently, so the best life insurance companies for you are the ones whose rules treat your condition most favorably. The exact diabetes that puts you in a two-year waiting period at one company might qualify for day-one coverage at another. Being turned down by one company does not mean no coverage exists. It usually means that company simply was not the right fit for your health.

That’s the real value of working with an independent broker. Because I’m not tied to one company, I can take your specific health picture to the highly rated carrier whose rules treat it best — the one that puts your condition in its lowest-risk group. For someone with a condition or two, that’s often the difference between waiting two years and being fully covered tomorrow, at the better rate.

An independent broker matches your health to the company that grades it best — often day-one coverage at a lower rate.

Two clients, two common conditions, both covered from day one.

One had type 2 diabetes. Another had mild COPD. Each assumed their health would force them into a guaranteed-issue policy with a two-year wait. It didn’t. For both, I found a company that issued full coverage starting on day one, at a premium quite a bit lower than a guaranteed-issue plan would have cost.

With one of these conditions, day-one coverage is usually well within reach. The key is matching you to the company that treats it best.

Worried a health condition will hold you back?

No exam · No pressure · A real answer

Who Qualifies for Burial Insurance?

Burial insurance is typically available to people between 50 and 85, and some companies stretch that range from 40 to 90. Beyond age, the bar is low: you need to be a U.S. resident and able to pay the premium. That’s really it.

Plenty of things that feel disqualifying simply aren’t. Diabetes, a history of heart trouble, cancer in remission, COPD, a long list of medications, even a past decline from another company — none of these shut you out. There’s always a path, all the way down to guaranteed issue, which accepts anyone in the age range.

The one thing working against you is time. Your rate is set by your age the day you apply and locked there for life. Every year you wait, the price goes up and a few more options close. If you’re going to do this, the cheapest day to start is today.

Is Burial Insurance Worth It?

For most middle-income people without a big cushion, yes — burial insurance is worth it because it turns an unpredictable five-figure bill into a small, steady payment your family never has to scramble for. But whether it’s worth it depends on your situation, so let me give you the honest math, both sides.

The case for it. A recent CardRates survey found that 58% of adults say they’d have to borrow to pay for a funeral. And the share of families who actually took on debt to bury a loved one jumped from 14% in 2024 to 37% in 2025, according to Debt.com, most of it on credit cards. For a fixed monthly payment, a final expense insurance policy takes that risk off your family’s shoulders. This isn’t about how much life insurance you can buy; it’s about covering one certain bill. And if your health keeps you from getting regular life insurance, final expense insurance may be the only coverage you can actually get.

The honest other side. If you live a long time, the premiums you pay can add up to more than the benefit. That sounds like a bad trade until you remember what insurance is for: if you pass early, a few months of premiums becomes the full benefit, paid right away. You’re buying certainty, not a return.

When it may not be the right fit. If you’ve got substantial savings your family could reach quickly, you might simply cover the funeral yourself. And if you’re young and healthy enough to qualify for traditional life insurance, you’ll often get more coverage per dollar from a term or whole life policy. Be honest with yourself about which camp you’re in.

The share of families who took on debt to bury a loved one jumped from 14% in 2024 to 37% in 2025 (Debt.com).

Is Burial Insurance Right for You?

Burial insurance is a strong fit if you’re between 50 and 85, have little or no life insurance coverage, and don’t have a comfortable cushion set aside for your final expenses.

- Are between 50 and 85 with little or no life insurance in place.

- Don’t have savings your family could easily reach to cover final costs.

- Have health conditions that make traditional life insurance hard to get or too costly.

- Live on a fixed income and need a payment that never changes.

- Want to make sure your spouse or children never have to borrow to bury you.

- Have substantial savings already earmarked and reachable for final costs.

- Can still qualify for and afford traditional life insurance policies with a larger benefit.

- Are mainly looking to replace income or leave a large inheritance — that’s a different product.

How to Buy Burial Insurance the Right Way

Figure out how much you need, then compare more than one insurance company — ideally through an independent broker who can shop them all — and never buy on price alone. The cheapest policy on paper can be the wrong one if it comes with a two-year wait you didn’t need. Here’s the order I’d walk you through.

Buying a final expense insurance plan, step by step

Never buy on price alone — the cheapest policy on paper can be the wrong one.

- 1Size ItSet your coverage amount

Use the sizing steps above to land on your target.

- 2Price ItEstimate your real costs

From a local funeral home’s itemized price list.

- 3CheckSee what you already have

Savings or an existing policy may shrink what you need.

- 4Be HonestTake stock of your health

It decides which tier you’ll qualify for.

- 5Shop WideWork with an independent broker

Not a captive insurance agent tied to one company — someone who can compare many companies, not just one.

- 6CompareWeigh more than price

Compare the type, the waiting period, and the benefit across the best burial insurance companies.

- 7ApplyExpect a short, simple process

A few health questions, a prescription-history check, and a short phone interview.

- 8ReviewUse your free-look period

When the policy arrives, read it over and cancel for a full refund if it’s not right.

- 9Tell SomeoneTell your beneficiary the policy exists

And where to find it.

Those cheap-sounding TV and mailer policies usually cost more for less — and most people don’t even need them.

The heavily advertised “as low as $9.95” offers are almost always guaranteed issue: no health questions, but a two-year waiting period for everyone and a higher price for every dollar of coverage. Here’s what stings — most people who buy them could have qualified for day-one coverage at a lower price if they’d simply answered a dozen health questions and let a broker match them to the right company. Two more to sidestep: naming your estate as beneficiary instead of a person sends the money through probate, and applying with just one company when another would treat your health better leaves money and time on the table.

Special Situations for Burial Insurance

A few situations deserve their own word, because the standard answer doesn’t quite cover them. Here are the ones that come up most.

Can you buy burial insurance for a parent?

Yes — and it’s one of the most caring things an adult child can do when planning for funeral expenses. If you’re the one who’d be planning the funeral and footing the bill, a policy on your parent makes sure that day isn’t a financial blow on top of a loss. Your parent has to be part of it: they’re the insured, so they need to know about the policy, agree to it, and answer the health questions themselves. From there, you can be the owner who controls the policy, the payor who covers the premiums, and the beneficiary who receives the money. Because their funeral costs would fall to you, you have what’s called an insurable interest, which is exactly what lets you set this up.

Burial insurance benefits for veterans

The VA does help, but it rarely covers everything. For a service-connected death the VA pays up to $2,000 toward burial. For a non-service-connected death — for deaths on or after October 1, 2025 — it pays up to $1,002 for burial plus a separate $1,002 plot allowance, and a plot and headstone in a national cemetery come at no cost. The catch is that the funeral home’s bill is usually separate and larger — and that gap is exactly what a burial policy is built to fill.

What Social Security pays toward a funeral

Many people are surprised to learn Social Security pays a one-time death benefit of just $255, a figure that hasn’t changed since 1954, which is rarely enough for funeral expenses. It covers only a sliver of a typical funeral. It’s a nice gesture, not a plan.

Burial insurance on a fixed income

This is where this coverage shines. It turns a sudden five-figure expense into a steady monthly payment you can line up with your Social Security deposit. Predictable is the whole point. And if you live alone or without close family nearby, a small policy keeps the arrangements in your own hands, set up exactly the way you want them.

The one-time Social Security death benefit — unchanged since 1954. It covers only a small fraction of today’s median funeral.

Source: Social Security Administration

How Burial Insurance Compares to Other Options

Compared with the common alternatives — a preneed funeral plan, plain savings, or term life insurance — it trades a little efficiency for a lot of certainty and flexibility. Here’s how they stack up.

Burial insurance vs. preneed funeral insurance

A preneed funeral plan — sometimes written preneed funeral insurance — locks in today’s prices, which is its real strength. If you’re choosing between burial or preneed insurance, that price lock is the main draw. But the money is tied to one specific funeral home. If that home closes, gets sold, or you move to be near family, transferring it can get complicated. Burial insurance pays cash to your family, who can use any funeral home anywhere.

Burial insurance vs. saving the money yourself

On paper, saving is the most efficient — no insurance company in the middle. The problem is time. It takes years to set aside enough, and if you pass before you get there, the account is short and the family is stuck. Insurance creates the full amount the moment your first payment clears.

Burial insurance vs. term life insurance

A term life policy is cheap for a big benefit, but it expires — often right around the age when a funeral becomes likely. Outlive the term and you’re left with nothing after years of payments. Because a funeral is a certainty, a permanent life insurance policy is the piece that fits this particular bill.

A little less efficiency for a lot more certainty and flexibility.

| Burial insurance | Preneed plan | Savings | Term life | |

|---|---|---|---|---|

| Who controls the money | Person you name | The funeral home | You / your estate | Person you name |

| Medical exam | No | No | — | Sometimes |

| Tied to one funeral home | No | Yes | No | No |

| Premium fixed for life | Yes | Varies | — | During term only |

| Lasts your whole life | Yes | Yes | — | No — expires |

| Locks today’s funeral price | No | Yes | No | No |

After You Buy Your Policy

A few simple steps after you buy make sure the policy actually does its job when the time comes. The coverage only works if the right person knows about it and the payments keep going.

Tell your beneficiary. A lot of benefits go unclaimed every year simply because no one knew the policy existed. Tell the person you named the company’s name, the policy number, and where you keep the paperwork.

Name a backup. Always name a contingent beneficiary in case your first choice passes before you do. And never name your estate — that drags the money through probate. The National Association of Insurance Commissioners publishes free consumer guidance on naming and updating beneficiaries.

Keep the payments going. Most policies give you a grace period of about a month if you miss one, and some will borrow from your cash value to cover it. Lining the payment up with your Social Security deposit is the easiest way to never miss.

Check in now and then. Funeral costs rise over time. A policy you bought years ago may not stretch as far today, so it’s worth a look every few years to make sure the coverage still fits.

How your family files a burial insurance claim

The benefit is usually paid within days.

- 1GatherGet several certified copies of the death certificate

You’ll need more than one.

- 2CallPhone the insurance company’s claims line

The number is on the policy.

- 3CompleteFill out the company’s claim form

Short and straightforward.

- 4SubmitSend the form with a certified death certificate

That’s the full package.

- 5ReviewThe company reviews the claim

Usually within days.

- 6PaidThe benefit is paid to your beneficiary

By check or direct deposit.

Burial insurance: frequently asked questions

The questions people ask me most, answered plainly.

Is burial insurance the same as life insurance?

Yes. Burial insurance is a type of whole life insurance — it is life insurance. You’ll also see it sold as final expense insurance or funeral insurance; the names just describe what it’s for, not a different kind of product.

Can the money be used for anything besides the funeral?

Yes. Your beneficiary gets a cash payment with no restrictions. They can put it toward funeral and burial costs, medical bills, debts, or anything else the family needs.

Can I buy burial insurance for my parent?

Yes. Your parent has to know about it, agree, and answer the health questions, since they’re the insured. From there you can own the policy, pay the premiums on the final expense insurance plan, and be the beneficiary. Because their funeral would fall to you, you have an insurable interest, which is what allows it.

What if I pass during the two-year waiting period?

It depends on the type. On a guaranteed issue life insurance policy, the company refunds all your premiums plus interest. On a graded policy, your family gets a portion of the benefit. Accidental death is often paid in full from day one.

Will my premium go up as I get older?

No. Your premium is locked at the rate in place the day the policy starts. It can’t rise as you age or if your health changes.

Does “no medical exam” mean I’m automatically approved?

Only on guaranteed issue policies. With simplified issue, “no exam” means no physical — the insurance company still reviews your health answers and records, so you can still be placed in a waiting-period tier.

Will my family owe taxes on the money?

Generally no. Life insurance benefits are typically paid income-tax-free. For very large estates, it’s worth a word with a tax professional.

When is the worst time to buy burial insurance?

When you’re older and in poor health. Rates are highest then and your options are fewest. The best time is as early as you’re willing — the rate locks in lower and stays there.

Let’s find the coverage that fits you

You came here to make sure the people you love won’t be left scrambling, and now you know enough to do exactly that. The next step is simple: let’s look at your real situation and find the burial or final expense insurance that fits, at a price that locks in today. Remember, the rate is set by your age right now — so the cheapest day to start is the one you’re standing in.

This article is for educational purposes only and is not legal, tax, or financial advice. Coverage, costs, and rules for life insurance plans vary by person, company, and state. Please speak with a licensed professional about your specific situation before making a decision.