What Is an Annuity? The Complete Guide to How Fixed, Indexed, and Income Annuities Work

Fixed, indexed, immediate, and variable annuities explained in plain English: how they work, what they pay, and how to choose the one that fits your retirement.

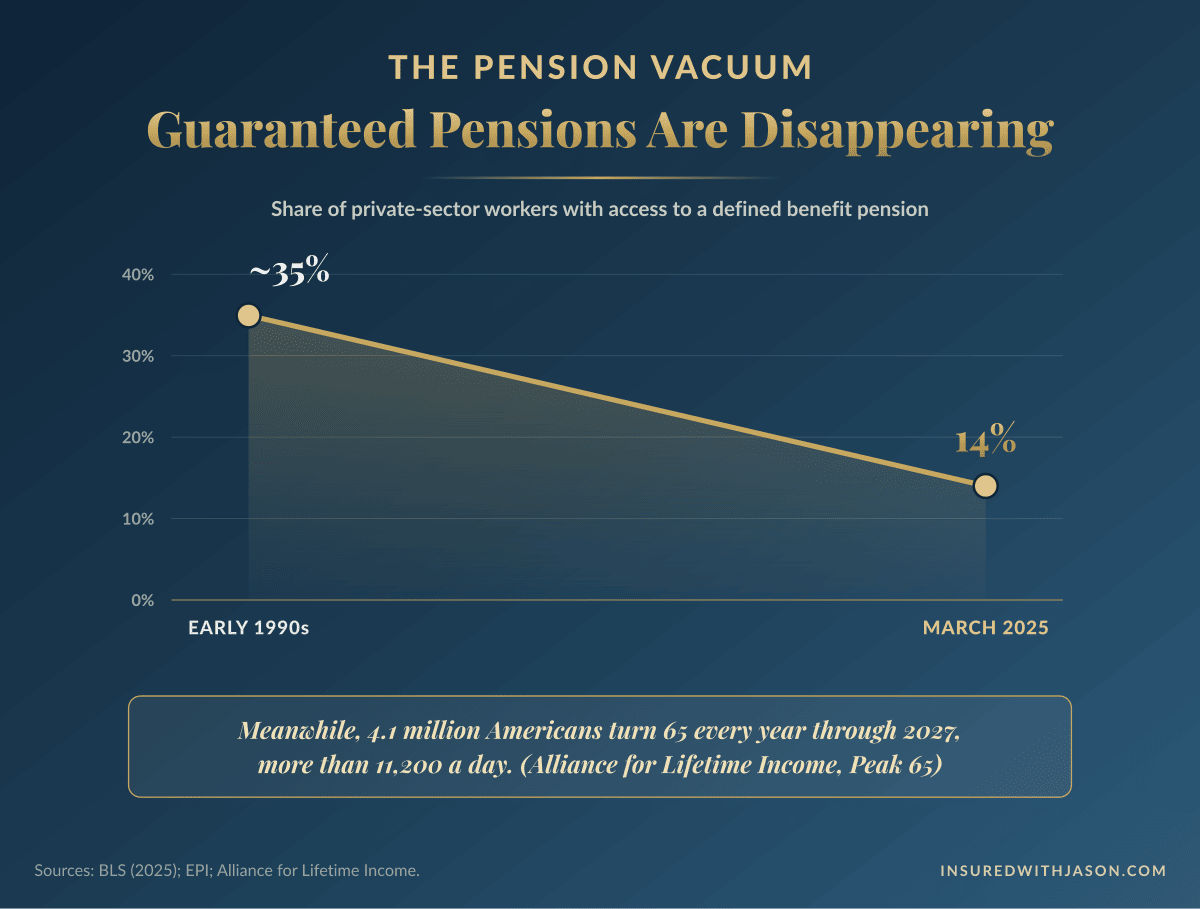

An annuity is the only financial product that can guarantee you a monthly check for as long as you live. It makes the same promise a pension used to make, back when people still got pensions. Today only 14% of private-sector workers have access to one, down from roughly a third in the early 1990s, and more than 11,000 Americans turn 65 every single day, most of them walking into retirement without it.

Now, somewhere along the way, somebody probably told you annuities are bad. Maybe it was a TV personality, maybe a brother-in-law, maybe an article with a headline like “Why I’d Never Buy an Annuity.” The fees. The fine print. The pushy salesman. And here’s the strange part: the warning was half right. That annuity exists. But it’s one product out of five, and it’s almost certainly not the one you were looking for. The annuity most people actually want pays a guaranteed rate, protects every dollar of principal, and writes that monthly check no matter how long you live. This guide separates the five types cleanly, shows you exactly where the horror stories come from, and helps you figure out which one, if any, belongs in your retirement.

What this guide covers, in eight facts

- An annuity is a contract with an insurance company, not an investment. Its one job is income you cannot outlive.

- When people say “annuities are bad,” they almost always mean variable annuities. Fixed annuities work completely differently.

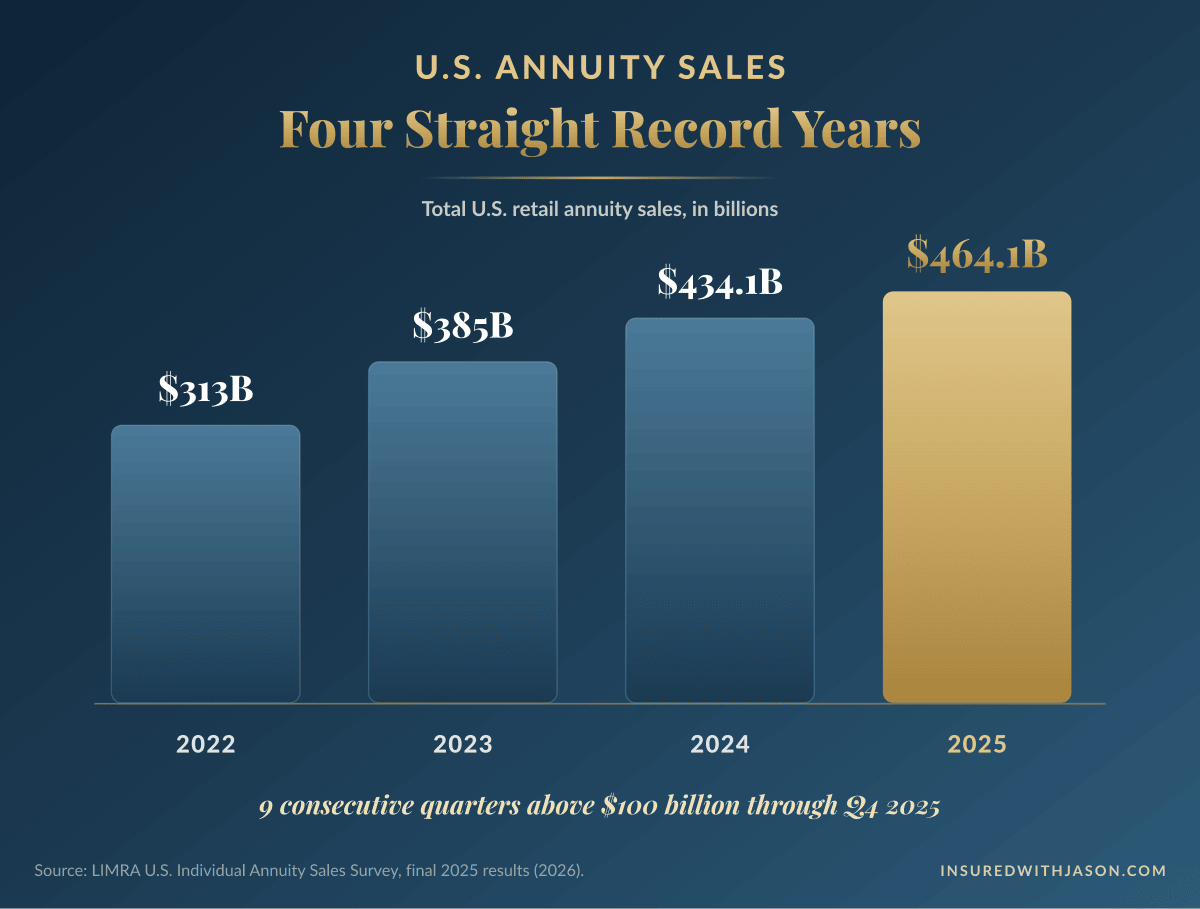

- Americans put a record $464.1 billion into annuities in 2025, the fourth record year in a row (LIMRA).

- Only 14% of private-sector workers still have access to a traditional pension (BLS, 2025). Annuities exist to fill that gap.

- A fixed annuity has no separately charged annual fees. A variable annuity typically stacks several, often topping 2–3% per year.

- Annuities are not FDIC insured. They’re backed by the insurer and by state guaranty associations, typically up to $250,000.

- All 50 states now hold agents to a best-interest standard when recommending an annuity.

- The right product depends on your goal: growth, income now, or income later. This guide maps each one.

What Is an Annuity?

An annuity is a contract between you and an insurance company. You hand the insurer a sum of money, as a lump sum or a series of payments, and in return the company guarantees to pay you back, either as growth at a stated rate or as a stream of income for a set period or for the rest of your life.

That last part is the whole reason annuities exist. Every other place you can put retirement money, a CD, a bond fund, a stock portfolio, can run out while you’re still alive. An annuity that pays lifetime income cannot. There are only three sources of income in America that you can’t outlive: Social Security, a pension, and an annuity. Two of those you can’t go out and buy. One you can.

Like other insurance policies, the promise is backed by the financial strength of the insurance company that issues it, not by the FDIC. State insurance departments regulate these contracts, and state guaranty associations provide a backstop, typically up to $250,000 per person, per insurer, if a company ever fails.

One more thing worth saying plainly, because it shapes everything that follows: an annuity is not an investment. It’s insurance for your income. Judging it like a stock fund misses the point, the same way judging your homeowners policy by its rate of return would.

An annuity is the only thing you can buy that pays you for being alive.

How Annuities Work

Every annuity has two phases: the time your money grows, and the time it pays you. The first is called the accumulation phase. You fund the contract, and the money grows tax-deferred, meaning you owe no income tax on the growth while it stays inside. The second is the payout phase, when the contract starts sending money back to you, on a schedule you choose.

Four parties make annuities work. The owner buys and controls the contract. The annuitant is the person whose life the payments are measured on, usually the same person as the owner. The beneficiary receives whatever the contract pays at death. And the insurer is the company guaranteeing it all.

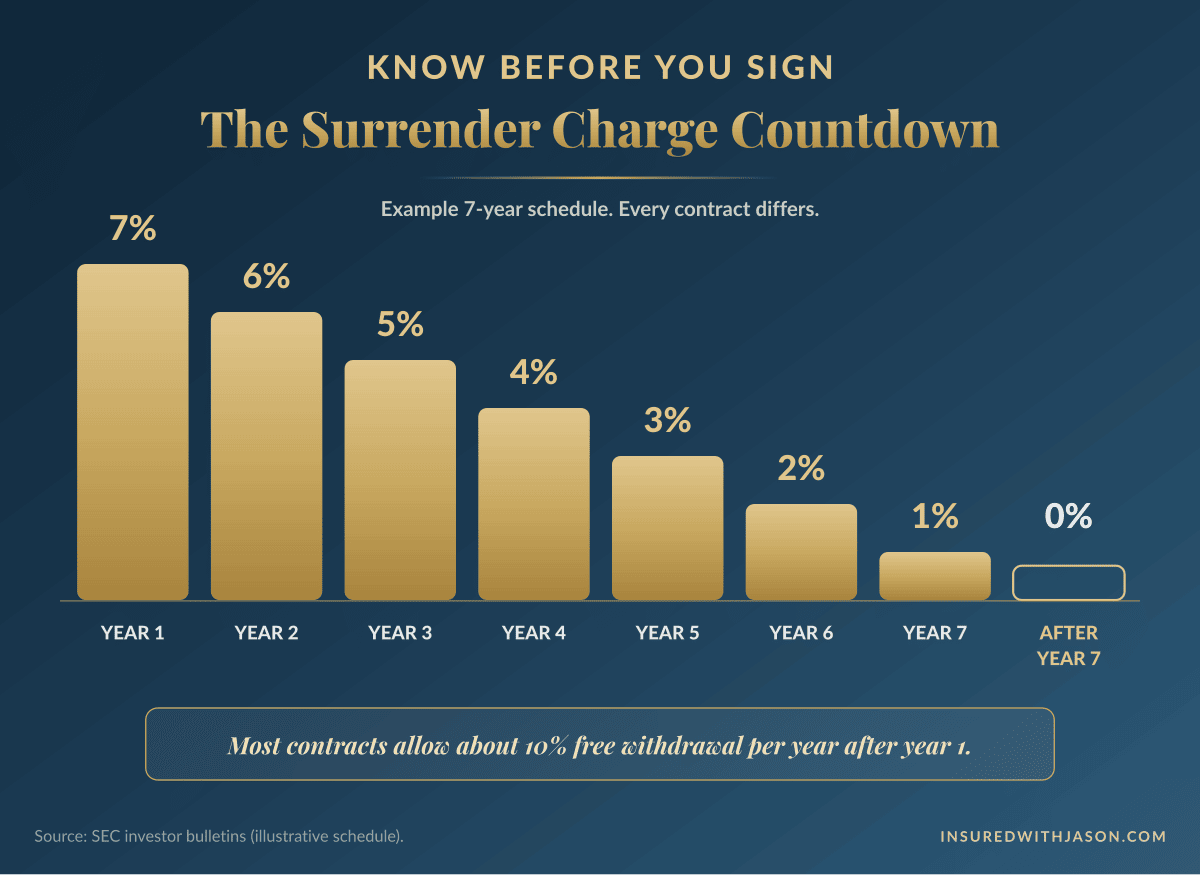

The flow is simple. You pick the type of annuity that matches your goal. You pay the premium. The contract is issued, and a surrender period begins, a stretch of years when pulling out more than the free amount triggers a charge. Your money grows according to the contract’s rules. Then, when you’re ready, you turn on the income, take withdrawals, or let it keep compounding.

Four straight record years: U.S. annuity sales climbed from $313 billion in 2022 to $464.1 billion in 2025.

What Are the Different Types of Annuities?

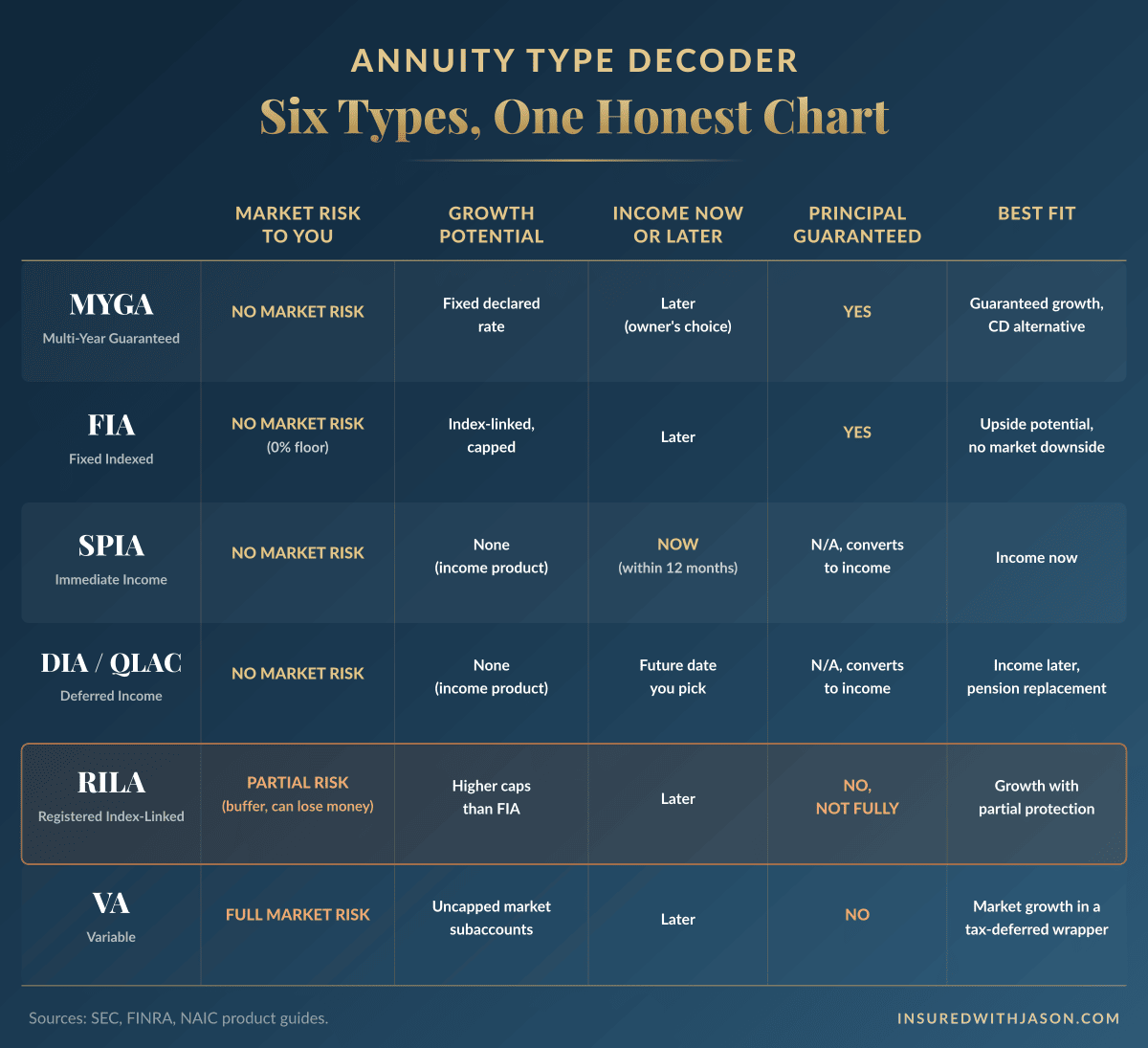

There are five common types of annuities, and they solve very different problems. The variety of annuities available is exactly why the topic feels confusing: people lump all these kinds of annuities together when the products barely resemble each other. Here is each one, plainly.

Fixed Annuities

Fixed annuities are the simplest of the bunch, and the kind most income-minded savers are actually looking for. The insurer pays you a guaranteed rate, and your principal is never exposed to the market. The most popular version is the MYGA, a multi-year guaranteed annuity. A MYGA is a fixed deferred annuity that locks in a fixed interest rate for a set term, commonly three, five, or seven years. It works a lot like a CD issued by an insurance company, with one big difference: the growth is tax-deferred. Traditional fixed annuities work similarly but declare a new rate periodically instead of locking one for the full term.

Immediate Annuities (SPIAs)

Immediate annuities skip the growth phase entirely. You pay a single lump sum, and income starts within a year, often within 30 days. The product’s formal name is the single premium immediate annuity, or SPIA. Its purpose is income now: you trade a sum of money for a paycheck that arrives every month, for a fixed period or for life.

Fixed Indexed Annuities

Indexed annuities, also sold as fixed index annuities or equity-indexed annuities, sit between fixed and variable in growth potential, but on the safe side of the line in risk. Your money is never invested in the market. Instead, the insurer credits interest based on the performance of a market index, such as the S&P 500, limited by a cap or participation rate. The floor is 0%: in a year the index falls, you earn nothing, but you lose nothing. Because your principal is protected, fixed indexed annuities are regulated as insurance products, not securities.

Variable Annuities

Variable annuities are where the market risk lives, and where most of the criticism comes from. Your premium goes into subaccounts, each working much like a mutual fund, and your account value rises and falls with the market. You can lose principal. Because of that, variable annuities are regulated as securities by the SEC and FINRA on top of state insurance oversight. They carry layered annual fees, which we’ll put under a bright light in the next section. They do serve a real purpose for some savers who want tax-deferred market growth with no contribution limit, but they are a fundamentally different animal from everything above.

A newer cousin deserves a mention: registered index-linked annuities, or RILAs. They credit interest from an index like an FIA does, but with only a partial buffer against losses instead of a full floor. A RILA can lose money. It is not a principal-protected product, and it should never be confused with one.

What Are the Different Types of Deferred Annuities?

Deferred annuities are any annuity where the payout starts later, and the deferral is the point: time makes the eventual income bigger. The deferred family includes the MYGA and FIA above, plus the deferred income annuity (DIA), where you pay today and lock in income that begins at a future date you choose. The longer you defer, the larger every payment becomes. A specialized version called the QLAC lives inside an IRA or 401(k) and carries a bonus: the money you put in is excluded from your required minimum distribution calculation, up to $210,000 in 2026 (IRS).

Every major annuity type, decoded: market risk, growth, income timing, and principal protection side by side.

Fixed Annuity vs. Variable Annuity: What’s the Real Difference?

The difference comes down to who carries the market risk, and who pays the fees. In a fixed annuity, the insurance company carries the risk and earns its money quietly, inside the rate it offers you. There is no separate annual fee subtracted from your account. In a variable annuity, you carry the market risk and you pay for the wrapper: a mortality and expense charge that the SEC notes typically runs around 1.25% per year, administrative fees, the expenses of each subaccount, and optional rider charges on top. Industry research from Morningstar has put the average all-in cost of a variable annuity with a living-benefit rider at roughly 3.33% per year.

That fee stack is the source of nearly every “annuities are terrible” story you have ever heard. The critics aren’t wrong about the math. They’re wrong about the scope. The gap between fixed and variable annuities is so wide that condemning one because of the other is like swearing off all vehicles because motorcycles are dangerous.

State insurance departments oversee insurance and annuity products like MYGAs and FIAs. Variable annuities answer to the SEC and FINRA as well, because your money is genuinely in the market. That regulatory split is the clearest tell of all: regulators themselves treat these as different products.

| Fixed Annuity | Variable Annuity | |

|---|---|---|

| Principal protected from market losses | Yes, guaranteed by the insurer | No, account value can fall |

| How it grows | Guaranteed rate, or index-linked crediting with a 0% floor | Market subaccounts, uncapped up and down |

| Separately charged annual fees | None; the insurer’s margin is built into the rate | M&E (~1.25%) + admin + subaccount + rider charges |

| Who regulates it | State insurance departments | State insurance + SEC and FINRA |

| Typical surrender period | About 3–10 years | About 6–10 years |

| Best fit | Principal safety and guaranteed income | Tax-deferred market growth with no contribution limit |

Fee figures from SEC investor bulletins and Morningstar research. Every contract differs; read yours.

When people say annuities are bad, they almost always mean variable annuities.

How Do Annuities Pay Out Income?

You choose how an annuity pays you, and the choice shapes both the size of the check and what happens after you’re gone. Life annuities pay until the day you die, no matter how far away that is. The main payout options:

Life only pays the largest monthly amount because payments stop at death, with nothing left to heirs. Life with period certain guarantees payments for your life or a minimum stretch, often 10 or 20 years, whichever is longer, so an early death still sends the remaining guaranteed payments to your beneficiary. Joint and survivor covers two lives, typically spouses, paying until the second person passes. And deferred contracts can also pay through simple withdrawals or a full lump sum once the surrender period ends.

The engine underneath lifetime income is something called mortality credits, and it’s worth thirty seconds to understand. When you buy an income annuity, you join a pool of thousands of policyholders. Those who pass away earlier than expected leave behind payments they never collected, and that money funds the checks of those who live longest. No bond, CD, or dividend stock has access to that engine, which is why an income annuity pays more per dollar than a do-it-yourself withdrawal plan ever safely could. It is also why every birthday raises your payout rate.

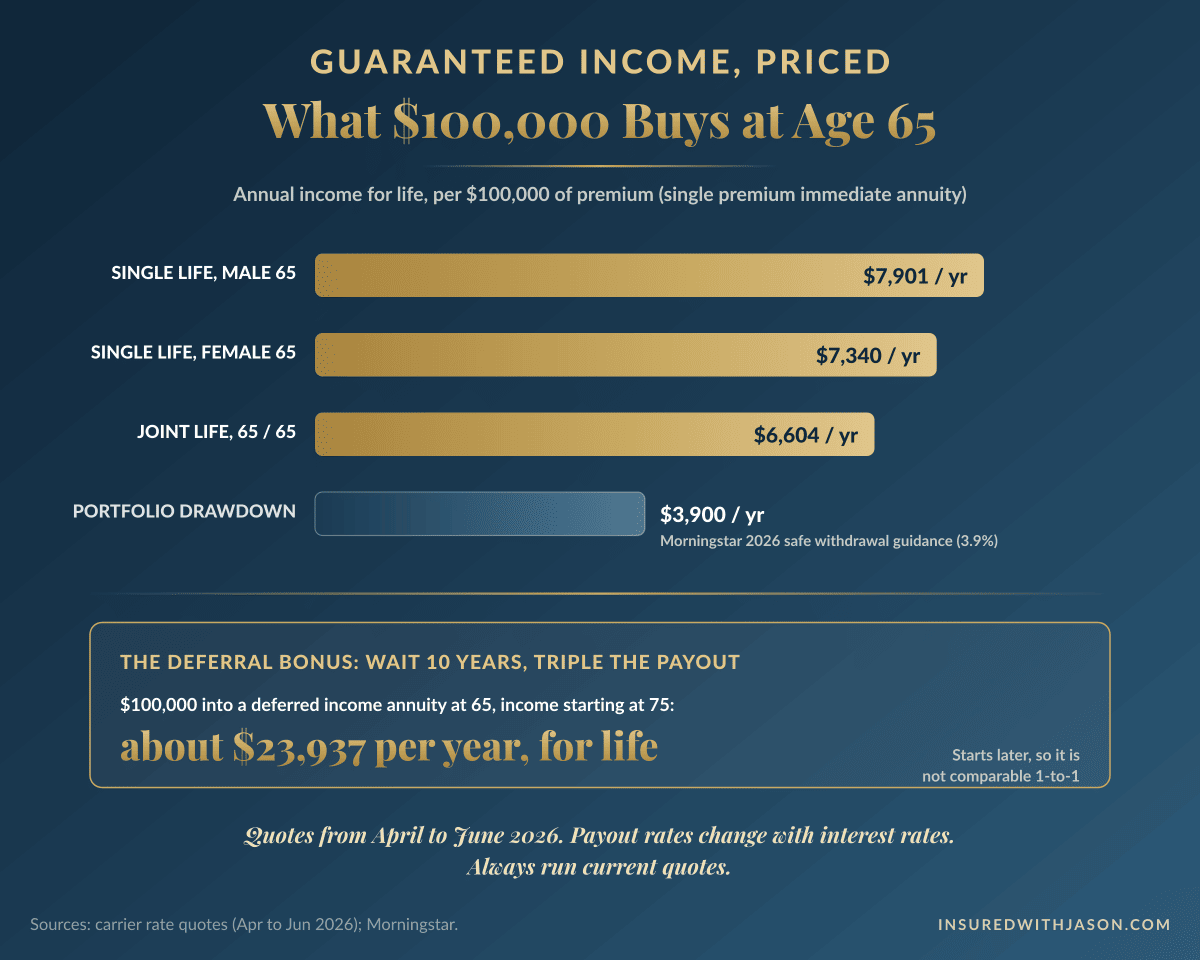

How much does an annuity pay? At payout rates quoted in spring 2026, a $100,000 single premium immediate annuity for a 65-year-old man paid roughly $7,900 a year for life, around $658 a month; about $7,340 a year for a 65-year-old woman; and around $6,600 a year for a couple covering both lives. Defer the start date and the numbers jump dramatically: that same $100,000 placed in a deferred income annuity at 65 with payments starting at 75 was quoting near $23,900 a year. These figures move with interest rates and differ by insurer, so treat them as a snapshot, not a promise.

What $100,000 buys at 65: guaranteed annuity income compared against the safe withdrawal rate, side by side.

Could an Annuity Strengthen Your Retirement Plan?

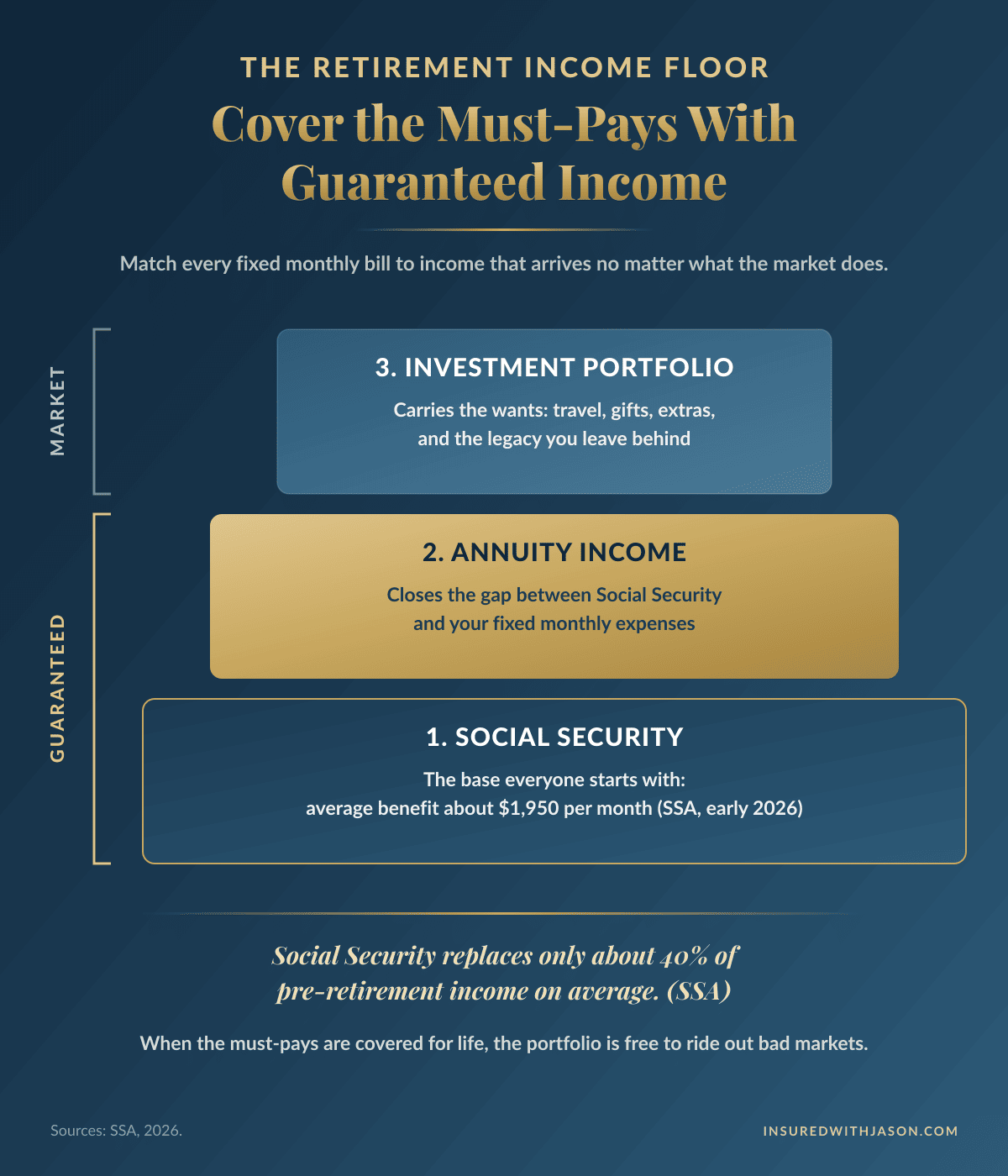

For most people without a pension, yes, and the reason is a strategy called the income floor. The idea is simple: cover every fixed, non-negotiable monthly expense, housing, utilities, food, insurance, with income that is guaranteed to arrive no matter what markets do. Social Security is the first layer of that floor. For the 86% of private-sector workers without a traditional pension, an annuity is the only way to build the second.

Here’s why the floor matters so much. Social Security replaces only about 40% of the average worker’s pre-retirement income, with the average check running near $1,950 a month in early 2026 (Social Security Administration). The gap between that check and your real monthly bills has to come from somewhere, and if it comes from selling investments during a downturn, the damage compounds. Researchers call this sequence-of-returns risk: big losses in the first years of retirement, paired with withdrawals, can permanently cripple retirement savings even when the market eventually recovers.

Guaranteed income neutralizes that risk for the expenses that matter most. When the floor covers your bills, your portfolio never has to sell at the wrong time, which means it’s free to ride out downturns and keep growing. That’s what annuities offer that no allocation strategy can: a retirement plan where the essentials are simply not the market’s business.

The income floor: guaranteed sources cover your fixed expenses, so your portfolio never has to sell at the wrong time.

Guaranteed-income access in the private sector fell from roughly 35% of workers in the early 1990s to 14% in 2025.

Curious what an income floor would look like with your numbers?

No pressure · No obligation · A real answer

Annuities vs. Other Retirement Options: Pros & Cons

Annuities trade liquidity for certainty. Whether that trade wins depends on what you’re comparing them against.

Against CDs: the MYGA is the natural matchup. Industry data from LIMRA shows that deferred fixed annuity rates have, on average, run higher than comparable CD rates in recent years, and the MYGA adds tax deferral on top, since CD interest is taxed every year whether you touch it or not. The CD wins on FDIC insurance and easy access; the MYGA typically wins on yield and taxes.

Against bonds and bond funds: bonds can lose value when rates rise, and no bond ladder can pay you for being alive at 96. An income annuity removes the price risk and adds mortality credits. Bonds win on liquidity and on the ability to sell anytime.

Against staying fully invested: the market offers the highest long-run growth, and for money you won’t need for decades, it’s hard to beat. But a portfolio paying your grocery bill is exposed to sequence risk, and Morningstar’s 2026 research puts the safe withdrawal rate at just 3.9% per year. An annuity converts a slice of savings into income at a far higher rate, precisely because it stops being a pile of money and becomes a paycheck.

And the honest cons, because every product has them: your money is committed during the surrender period, usually with about 10% a year accessible free. A level payout slowly loses ground to inflation over a 25-year retirement. And the guarantee is only as strong as the insurer behind it, which is why company financial strength matters so much. We cover how to check it below.

| MYGA | Bank CD | |

|---|---|---|

| Rate, recent years | Historically higher on average (LIMRA) | Lower national averages (FDIC) |

| Taxes on growth | Deferred until withdrawal | Taxed every year as earned |

| Backed by | Insurer + state guaranty association (typically $250,000) | FDIC (up to $250,000) |

| Access to funds | ~10% free per year; surrender charge beyond that | Early withdrawal forfeits interest |

| Lifetime income option | Yes, can convert to income | No |

Annuity rates and CD averages change constantly. Compare live quotes before deciding.

Annuities and Taxes

Annuities grow tax-deferred, and how the money comes out determines how it’s taxed. Tax-deferred growth means no annual tax bill while the money compounds inside the contract. Deferred is not tax-free, though. The IRS gets paid eventually, and the rules below decide when and how much.

Qualified vs. non-qualified. A qualified annuity is funded with pre-tax retirement money, like an IRA rollover, so every dollar that comes out is taxed as ordinary income. A non-qualified annuity is funded with money you already paid tax on, so only the growth is taxable.

The exclusion ratio. When you convert a non-qualified annuity into an income stream, the IRS treats part of every payment as a tax-free return of your own principal and only taxes the growth portion. Depending on your age and contract, a healthy majority of each check can arrive tax-free for years.

The withdrawal trap. Take casual withdrawals from a non-qualified deferred contract instead of annuitizing, and the IRS applies last-in-first-out treatment: gains come out first and are fully taxable until they’re exhausted.

The age 59½ rule. Pull taxable gains out before age 59½ and a 10% federal penalty generally applies on top of the tax, with limited exceptions. Annuities are retirement tools; the tax code enforces that.

What heirs receive. Beneficiaries owe ordinary income tax on any untaxed gain, and unlike inherited stocks or real estate, annuities receive no step-up in basis. Naming a real person as beneficiary lets the money bypass probate. Required minimum distributions apply to qualified contracts starting at age 73 for those born before 1960, and 75 after.

CD interest can raise the tax on your Social Security. Deferred annuity growth cannot.

Interest from CDs counts toward the income formula that determines how much of your Social Security benefit gets taxed, even if you never spend a dime of it. Growth inside a deferred annuity stays out of that formula until you withdraw it. For retirees holding large CD balances, that difference quietly changes the April tax bill.

When Should I Purchase an Annuity?

The strongest window for most people runs from about age 50 to 70. Before 50, the surrender period and the age 59½ rule make the fit awkward for most savers. After 70, income payouts are at their richest, thanks to mortality credits, but the de-risking benefits of the deferral years have passed. Inside that window, the right timing depends on the product and your retirement goals.

The 55-to-65 stretch is the classic de-risking window for MYGAs and indexed annuities. You’ve spent decades accumulating, retirement is close enough that a bad market year would genuinely hurt, and locking in a guaranteed rate on a slice of savings takes that risk off the table. For immediate income, most people purchase at or just after retirement. For a deferred income annuity, buying in your early-to-mid 60s with income starting in your 70s captures the biggest deferral payoff.

One timing note on rates: annuity rates follow the broader interest rate environment, so the guaranteed rate you can lock today won’t be the rate available next year, in either direction. Locking a good rate is a fine reason to act. But the guarantee, not rate-chasing, should drive the decision. If you’re weighing the timing question for your own situation, the companion piece on when an annuity makes sense walks through it from the decision side.

There’s no IRS limit on how much you can put into a non-qualified annuity.

IRAs cap you at a few thousand dollars a year. A non-qualified annuity has no federal contribution limit at all, which is why savers who have maxed their other accounts use one for additional tax-deferred growth. And inside an IRA, a QLAC lets you defer required distributions on up to $210,000 (2026 IRS limit) until as late as age 85.

Which Annuity Is Right for You?

Start with your goal, and the type of annuity picks itself. Different annuities solve different problems, so the question is never “are annuities good,” it’s “what job am I hiring one to do?”

If the job is guaranteed growth, a better rate than the bank with zero market risk, the MYGA is built for it. If the job is growth potential without market losses, the fixed indexed annuity gives you a piece of the index’s good years and a 0% floor in the bad ones. If the job is income starting now, the immediate annuity converts a lump sum into the biggest possible lifetime paycheck. If the job is income starting later, the deferred income annuity or QLAC manufactures a future paycheck at rates no immediate product can match. And if the job is market growth in a tax-deferred wrapper with money you can afford to risk, that’s the one job where a variable annuity genuinely competes, fees and all.

Match the product to your financial goals, not the other way around, and most of the complexity in this topic simply disappears.

A new retiree, a $1,400 monthly gap, and a portfolio that gets to stay invested.

Picture a 67-year-old whose Social Security pays $2,100 a month while fixed expenses run $3,500. That’s a $1,400 gap that would otherwise come out of investments every single month, in good markets and bad. At 2026 payout rates, a premium in the low $200,000s placed in an immediate annuity could generate income in that neighborhood for life, with exact figures depending on age, payout options, and rates at purchase. The floor gets covered. The rest of the portfolio stays invested without ever being forced to sell in a downturn.

The point of an annuity isn’t to replace your portfolio. It’s to protect it by taking the monthly bills off its back.

Not sure which type fits your situation?

Independent advice · Dozens of insurance companies compared

Who Shouldn’t Buy an Annuity?

Plenty of people, and a good broker will tell you so before you sign anything. An annuity may be the wrong tool entirely if any of these describe you.

Annuities for retirement work brilliantly for the right person and poorly for the wrong one. Here’s the honest split.

- Are between 50 and 70 and want to protect part of what you’ve built from market drops.

- Have no pension and want guaranteed income covering your fixed monthly expenses.

- Hold CD money you’d like earning a better guaranteed rate, tax-deferred.

- Worry about outliving your savings through a 25- or 30-year retirement.

- Want part of your retirement income to arrive no matter what markets do.

- Might need the full amount back within the next 5–7 years; surrender charges punish early exits.

- Already have guaranteed income exceeding your expenses; you’ve solved the problem annuities solve.

- Are focused on leaving the largest possible inheritance; life insurance transfers wealth far more efficiently.

- Would be committing most of your liquid savings to one contract.

What Should I Consider Before Buying or Replacing an Annuity Contract?

Five things decide whether an annuity contract serves you well: the insurer’s strength, the surrender schedule, the free-withdrawal terms, any riders, and, if you’re replacing, whether the switch truly leaves you better off.

Insurer strength first. Annuity guarantees are only as solid as the company making them, so check the insurer’s financial strength rating before anything else. Look for highly rated companies for any long-term contract, and remember the state guaranty backstop, typically $250,000, sits behind the insurer, not in place of choosing a strong one.

Know your surrender schedule. A typical schedule starts around 7% and declines a point a year until it hits zero. Most contracts free up about 10% per year for withdrawal without penalty after the first year, and many annuities also waive surrender charges for nursing home confinement or terminal illness. Read those provisions before you fund, not after.

Replacing a contract: the 1035 exchange. The tax code lets you swap one annuity for another with no tax bill through a direct insurer-to-insurer transfer. Sometimes that’s genuinely smart, like moving out of a fee-heavy older contract once its surrender period ends. But every replacement starts a brand-new surrender clock, and regulators repeatedly flag replacements where the main beneficiary was the person selling it. All 50 states now require agents to document that any annuity recommendation, especially a replacement, is in your best interest. Make whoever proposes a swap show you the math. When you compare annuities side by side, feature by feature, the right answer tends to be obvious.

How buying an annuity actually works

From first conversation to funded contract, the process is more protective than most people expect.

- 1Start With The GoalDefine the job: growth, income now, or income later

The goal picks the product. Everything else follows from this answer.

- 2Shop The MarketCompare contracts across multiple insurance companies

Rates, terms, and features vary widely for the same product type. This is where an independent broker earns their keep.

- 3The PaperworkApplication and best-interest review

Your agent must document that the recommendation fits your age, finances, liquidity needs, and goals. Required in all 50 states.

- 4Your Escape HatchUse the free-look period

After delivery, you get a window, typically 10 to 30 days depending on your state, to cancel for a full refund. Read everything.

- 5Fund ItFund the contract and file it with your important papers

Confirm the rate, the term, the surrender schedule, and your beneficiary designation are exactly what you agreed to.

An income rider’s “benefit base” is not money you can withdraw.

Income riders advertise a benefit base that grows at an attractive rate, sometimes 7% or more. That number exists only to calculate your future income payments. It is not your cash value, and if you surrender the contract, you receive the cash value, which can be far lower. Always ask for both numbers, in writing, before you buy.

Are Annuities a Good Investment for Retirement?

It’s the wrong question, and the right answer starts by fixing it. An annuity isn’t an investment, so measuring it by rate of return alone is a category error. It’s insurance against the one retirement risk you cannot diversify away: living longer than your money lasts. You can spread market risk across a thousand stocks. You cannot spread the risk of your own longevity across anything, except a pool of other policyholders, which is precisely what an annuity does.

The numbers make the risk concrete. According to the Social Security Administration’s life tables, a 65-year-old woman has roughly a one-in-three chance of reaching 90, a man about one in five. Plan a portfolio to last to 85 and you’ve built a plan that fails exactly the people who need it most: the ones who live long.

So the honest answer: as an investment, an annuity will underperform a good stock portfolio over most long stretches, and anyone who tells you otherwise is selling too hard. As insurance for your income, nothing else on the market does the job at all. Most strong retirement plans use both, the portfolio for growth, the annuity for the floor. If you’re weighing annuities for retirement, that’s the frame that makes the whole decision simple. The information about annuities in this guide gives you the map; a conversation about your actual numbers draws the route.

The chance that at least one member of a 65-year-old couple lives to age 90.

Source: American Academy of Actuaries

A typical surrender schedule steps down each year until it reaches zero, with about 10% free to withdraw annually after year one.

Most people who call me about annuities arrive already convinced they’re bad.

And almost every time, what they heard about was a variable annuity with stacked fees, while what they actually wanted was a guaranteed rate and a check that never stops. Watching good people walk away from the one product built for their exact problem, because of a warning about a different product, is what put this guide on my list.

I represent my clients, not any insurance company, so I have no stake in which type you choose, or whether you choose one at all. My only stake is that you decide with the full picture in front of you.

Key annuity terms, explained

Annuities: frequently asked questions

The questions people ask me most, answered plainly.

Can you lose money in a fixed annuity?

Not to market losses. A fixed annuity guarantees your principal and a stated rate, and an indexed annuity credits 0% in a down year rather than a loss. You can lose money two other ways: surrender charges if you withdraw too much too early, and inflation slowly eroding a level payout’s buying power. The guarantee itself rests on the insurer’s financial strength, backed by state guaranty associations, typically up to $250,000.

What happens to my annuity when I die?

It depends on the contract and payout option. A life-only payout stops at death. Life with period certain sends remaining guaranteed payments to your beneficiary. Joint and survivor continues paying a surviving spouse. A deferred annuity that hasn’t been annuitized passes its value to your named beneficiary as a death benefit, bypassing probate. Heirs owe ordinary income tax on any untaxed gains, since annuities receive no step-up in basis.

Are annuities FDIC insured?

No. Annuities are insurance contracts, not bank deposits. They are backed first by the financial strength of the issuing insurer, which is why ratings matter, and second by state guaranty associations, which protect annuity benefits typically up to $250,000 per person, per insurer, with limits varying by state. Savers placing more than that often spread it across multiple highly rated insurance companies.

How much income does a $100,000 annuity buy?

At rates quoted in spring 2026, a $100,000 immediate annuity for a 65-year-old paid roughly $612 to $658 a month for life depending on gender, and around $550 a month covering a couple. Defer the start date ten years and the same premium was quoting near $1,990 a month. These are snapshots: payouts change with interest rates, age, and options, so always run current quotes before deciding.

Can I get my money out of an annuity early?

Usually yes, within limits. Most contracts allow about 10% of the value per year penalty-free after year one. Beyond that, a declining surrender charge applies during the surrender period, and the IRS adds a 10% penalty on gains withdrawn before age 59½. Many contracts waive surrender charges for nursing home confinement or terminal illness, and every new contract includes a free-look window to cancel entirely.

Talk to an independent annuity broker

You now know more about annuities than most people ever will. The next step is seeing your own numbers. As an independent broker, I shop dozens of carriers rather than one company’s shelf, which means more choices, a better shot at a higher rate, a broader selection of contracts, and the possibility of a product suited to your exact situation that a captive agent could never show you. The advice works for you, not on behalf of any insurance company. Tell me your goal, and I’ll show you what the market is actually offering for it right now.

This article is for educational purposes only and is not legal, tax, or financial advice. Annuity rates, payouts, features, and rules vary by person, company, and state, and change over time. Please speak with a licensed professional about your specific situation before making a decision.