Term Life Insurance: The Complete Guide to Coverage, Costs, and Choosing the Right Policy

What term life insurance covers, what it really costs at every age, how much you need, how long your term should run, and what happens at the end. All of it, in plain English.

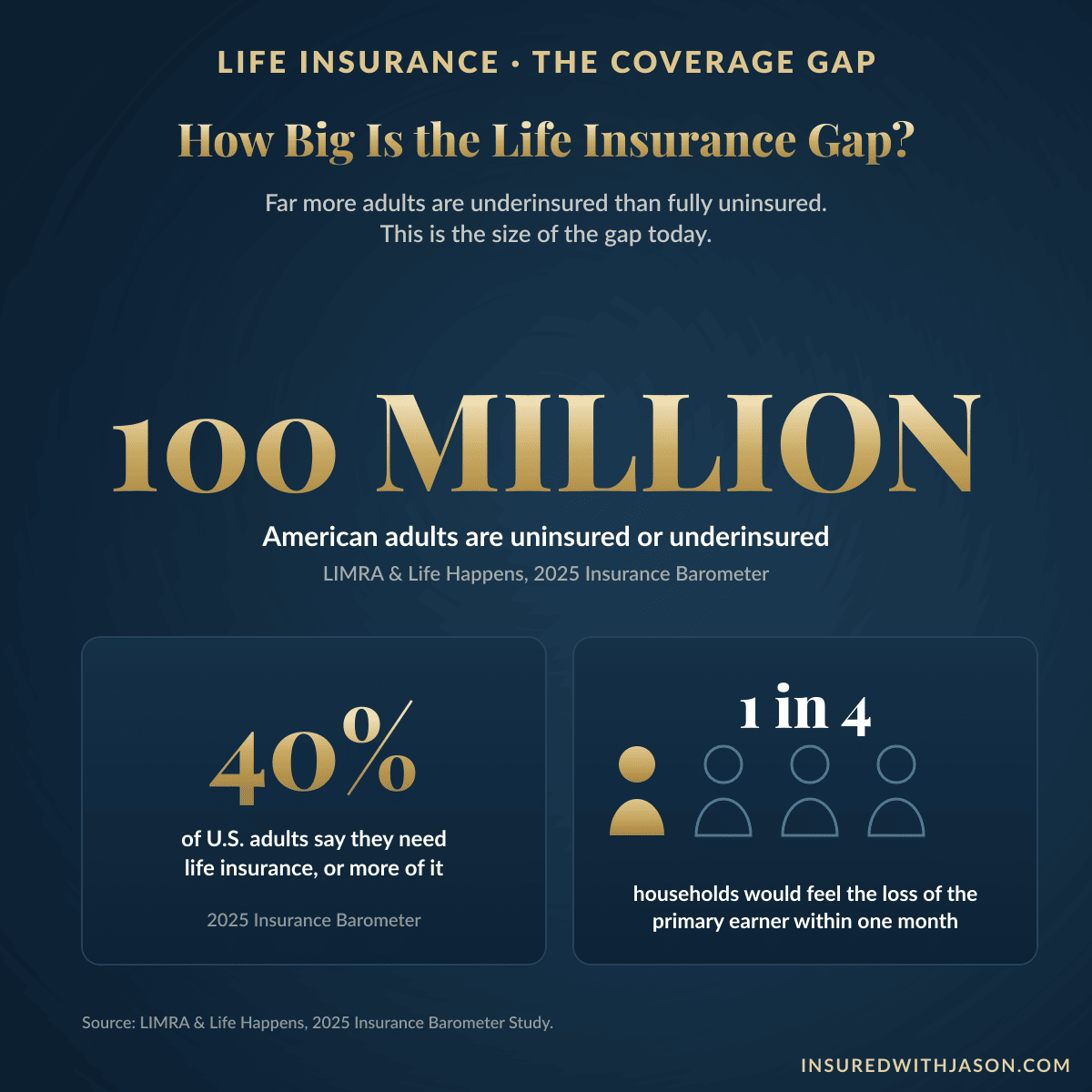

Here’s the question term life insurance answers: if your income stopped today, how long before your family felt it? For one in four American households, the honest answer is one month or less, according to LIMRA and Life Happens. The mortgage doesn’t pause. The grocery bill doesn’t shrink.

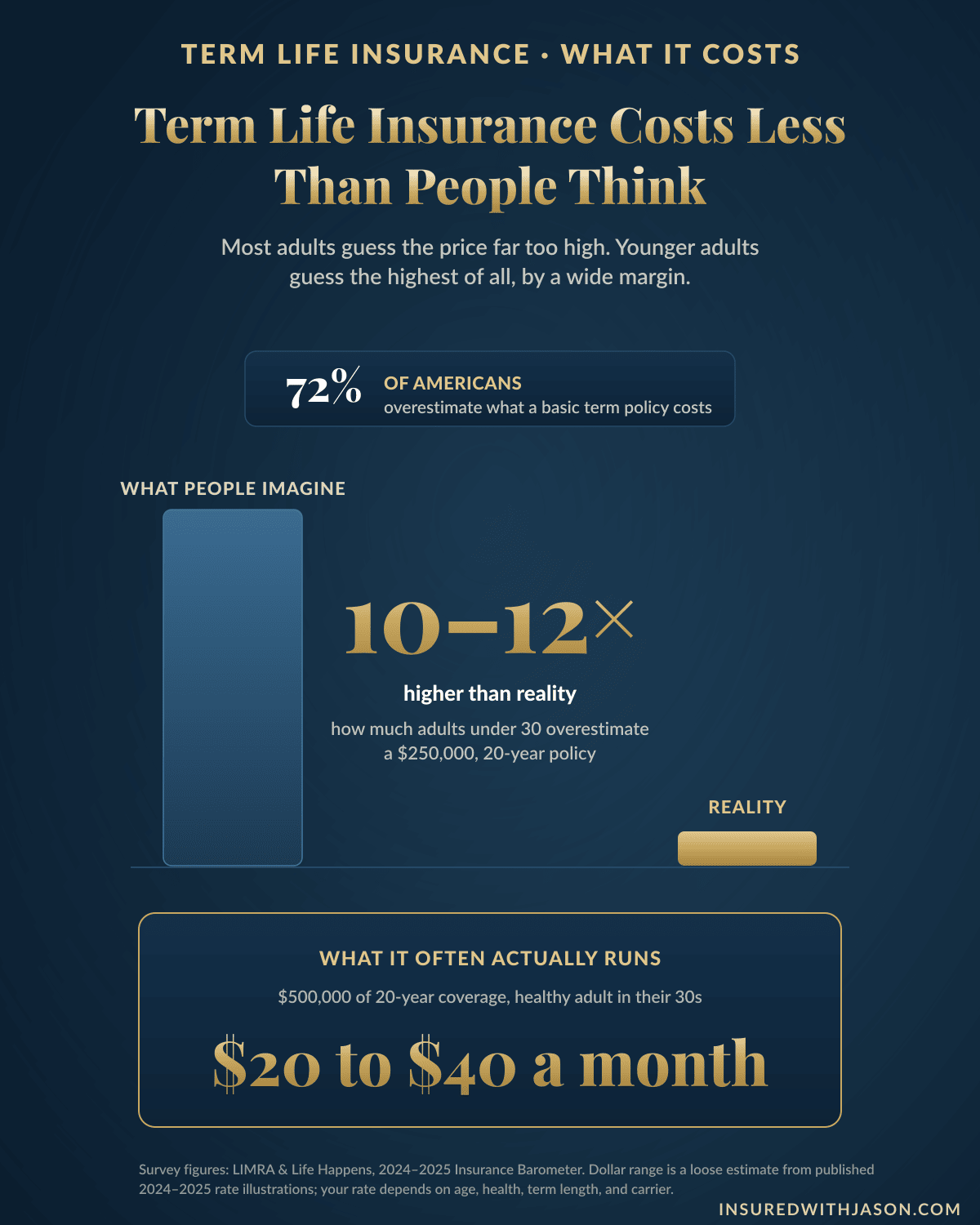

And here’s the strange part. Most people who need this coverage already know they need it. They’ve thought about it in the car, after the baby came, after the closing, after a friend’s funeral. What stops them is a number: the price they imagine, the one they never actually checked. Research shows most Americans overestimate what term life costs, and the youngest, healthiest buyers overestimate it by ten to twelve times. For a healthy adult in their thirties, the real price is often closer to a phone bill than a car payment.

This page walks you through all of it: what term life insurance is, how it works, what it tends to cost, how much coverage you need, and how to choose a policy you won’t second-guess. By the end, you’ll know enough to decide with confidence.

- Term life insurance is pure protection: it pays a tax-free death benefit to the people you name if you pass away during a set term, usually 10, 15, 20, or 30 years.

- It’s the most affordable life insurance there is. For the same coverage amount, whole life insurance can cost ten times more or higher, because part of every whole life premium builds cash value.

- Most people wildly overprice it in their heads. LIMRA and Life Happens found 72% of Americans overestimate the cost, and adults under 30 overestimate it by 10 to 12 times.

- Your premium locks in at the age and health you are the day you apply, and on a level term policy it never rises for the entire term.

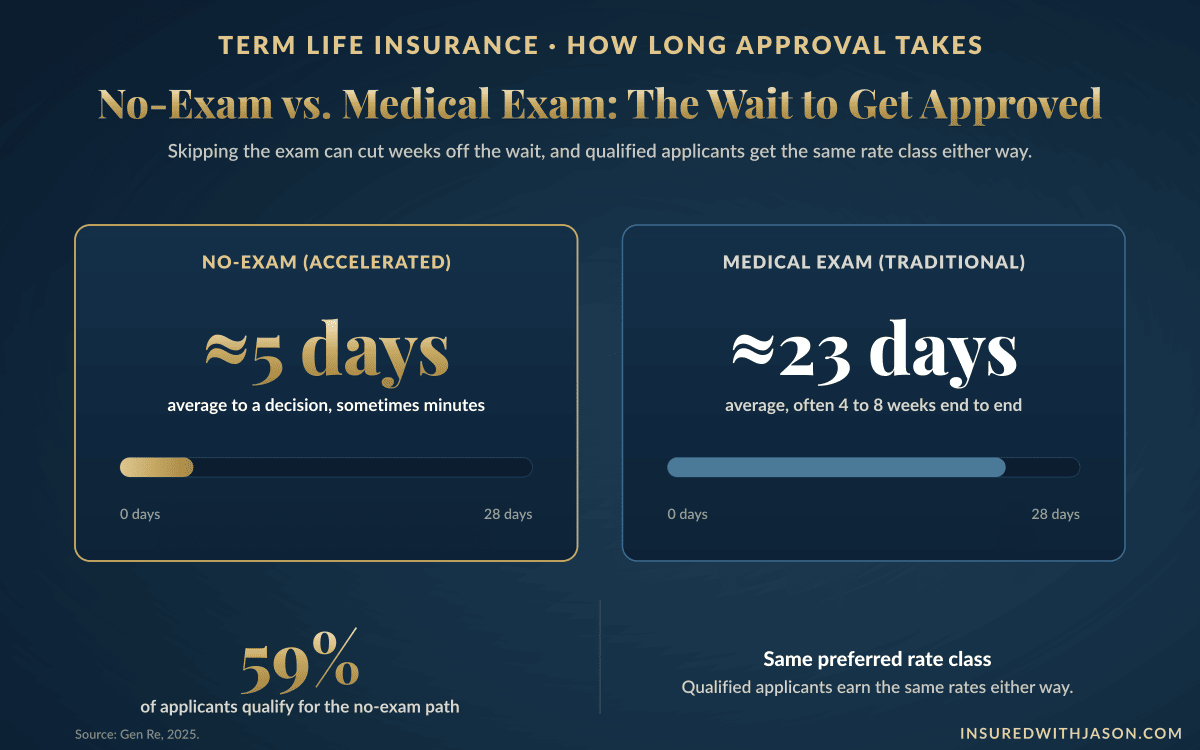

- About 59% of applicants now qualify for no-exam approval through accelerated underwriting, often in days instead of weeks (Gen Re, 2025).

- Work coverage is a floor, not a plan. Group life is usually one to two times salary, and it typically ends the day the job does.

- If you outlive the term, coverage simply ends. You can renew, convert, or shop a new policy, and the smart move is deciding years before the end of the term, not at it.

- An independent broker shops many insurance companies at once, which usually means more coverage for your budget or the same coverage for less.

What Is Term Life Insurance?

Term life insurance is a type of life insurance that pays your loved ones a lump sum of money if you pass away during a set period of time, called the term. You pick the coverage amount and the term length, usually 10, 15, 20, or 30 years. You pay a monthly or yearly premium. If you die while the policy is in force, the insurance company pays the full death benefit, generally income-tax-free, to the people you name. If you outlive the term, coverage ends and that’s that.

That last part is the whole design. Term insurance has no savings account inside it and no cash value. It does one job, protecting the years when other people depend on your income, and because it does only that one job, it’s the most affordable life insurance you can buy. Regulators describe it the same plain way: the NAIC’s Life Insurance Buyer’s Guide calls term coverage lower-cost protection for a specific period of time.

And it’s not a niche product. Term policies made up about 72% of all individual life insurance coverage issued by dollar amount in 2024, according to the American Council of Life Insurers. When American families buy protection, this is overwhelmingly what they buy.

How Does Term Life Insurance Work?

Term life insurance works as a straightforward trade: you pay a level premium, and the insurance company guarantees a fixed death benefit for the entire term. On a level term policy, the most common type of term life insurance plan, the premium you lock in on day one is the premium you pay in year twenty. It never rises during the policy’s term, no matter what happens to your health along the way.

A few built-in protections are worth knowing before you buy, because they answer the questions people are sometimes afraid to ask.

The grace period and the free look

Miss a payment and coverage doesn’t vanish at midnight. Most term life policies include a grace period of about 31 days to catch up, and if the insured were to pass away inside that window, the claim is still paid, minus the overdue premium. There’s also a free-look period when a new policy arrives, usually at least 10 days, when you can return it for a full refund. No questions, no penalty.

The two-year contestability period

For the first two years, the insurer can review a claim against the application to check for material misstatements. This is not a waiting period, and it does not delay honest claims. It exists to keep dishonest applications from raising everyone else’s life insurance rates. Answer every question truthfully and it never touches you.

Key term life insurance terms, explained

How much healthy adults under 30 overestimate the cost of a basic term life policy. Across all ages, 72% of Americans guess too high.

Source: LIMRA & Life Happens Insurance Barometer Study, 2024–2025

Why Buy Term Life Insurance?

People buy term life insurance to make sure the life they’ve built keeps standing if their income stops for good. The death benefit replaces a paycheck for years, pays off a mortgage, keeps kids in their home and on track for school, and clears debts so they never land on someone you love. Those are the classic reasons, and they’re reason enough. But after years of doing this, I can tell you the people purchasing life insurance are a much wider group than newlyweds with a stroller.

I see divorce decrees that require a policy to back up child support or alimony, because a court order is only as good as the income behind it. I see families who just watched a health scare up close and want their own house in order while they can still qualify. And I see parents of children with special needs who carry larger term life coverage than anyone, because if they’re not there to be the guardian, the money has to build the framework of support that keeps that child safe and living a rewarding life. Different stories, same problem: a window of years where someone depends on you, and the need to protect your loved ones through it.

The scale of the unmet need is real. About 100 million American adults say they have no life insurance coverage or not enough of it, per LIMRA’s 2025 study.

The coverage gap in one picture: roughly 100 million adults need life insurance or more of it, and one in four households would feel a lost paycheck within a month.

Who Is Term Life Insurance Right For?

Term life insurance fits anyone whose death would leave a financial hole during a specific stretch of years. That covers far more people than most articles admit.

- Have children at home, a spouse, or anyone who depends on your income or your caregiving. Stay-at-home parents count; replacing that work costs real money.

- Carry a mortgage or other large debts someone else would have to handle.

- Are required to carry coverage by a divorce decree backing child support or alimony.

- Have a child with special needs who will need funded support and guardianship if you’re gone.

- Want the most death benefit per dollar during your peak earning and obligation years.

- Need coverage that lasts your entire life for estate planning or a lifelong dependent. That points toward permanent insurance.

- Mainly want to cover funeral and final costs later in life. A small burial insurance policy is built for exactly that.

- Have no dependents, no significant debts, and assets that already cover everything you’d leave behind.

The Different Types of Term Life Insurance Policies

There are several different types of term life insurance policies, and they differ in how the premium and the death benefit behave over time. Knowing the handful of types of term life policies on the market keeps you from buying the wrong shape of coverage.

Level term

The workhorse, and what most people mean when they say term insurance. The premium and death benefit both stay fixed for the whole term. The 20-year term is the most popular length sold in America, with roughly 40% of the market according to LIMRA sales data.

Annual renewable term

An annual renewable term policy, sometimes called yearly renewable term, renews every year with a premium that climbs as you age. It starts cheap and gets expensive. Today this type of term mostly shows up as the renewal structure after a level term ends, not as something you’d buy on purpose for the long haul.

Decreasing term

The death benefit shrinks over time while the premium stays level, designed to track a falling mortgage balance. It’s a niche mortgage-protection tool now, since level term usually delivers more value for similar money.

Return of premium term

A level term policy that refunds the premiums you paid if you outlive it. It costs meaningfully more, and it has a real, loyal audience. There’s a full section on it below.

Convertible term

Most quality term life policies include a conversion privilege: the right to convert to permanent coverage with no new medical exam, inside a set window. It’s a feature riding along on your policy, not a separate product, and it matters most if your health changes mid-term.

Group term

The group life coverage you get through work. It’s usually small and usually not portable, and it gets its own honest section further down, because relying on it is one of the most common mistakes I see.

Term vs. Whole Life Insurance: Which Is Better?

Term life insurance is better for covering a temporary need with maximum coverage per dollar, while whole life insurance is better when you need coverage that lasts your entire life. Neither one wins outright; they’re different tools. The difference between term and whole life comes down to two things: how long the coverage lasts, and whether the policy builds cash value.

A whole life insurance policy is permanent life insurance. It covers you for life, the premium never changes, and part of each payment builds cash value you can borrow against. That permanence and savings engine is why whole life coverage is so much more expensive than term, often ten times the premium or more for the same death benefit. Universal life insurance is the other major family of permanent life insurance policies, with more flexibility and more moving parts. If you’re weighing term vs. permanent coverage, the honest first question is never which product is best, it’s how long the need actually lasts.

For a 30-year mortgage and kids who’ll be independent in 25 years, the need is temporary, and term wins on math. For a lifelong dependent, estate planning, or final expenses in later life, a permanent policy earns its higher premium because it’s guaranteed to be there.

| Term Life Insurance | Whole Life Insurance | |

|---|---|---|

| How long it lasts | A set term: 10 to 30 years | Your entire life, as long as premiums are paid |

| Premium | Level for the term, lowest cost available | Level for life, but far higher; often 10x or more for the same coverage |

| Cash value | None; it’s pure protection | Yes, grows over time and can be borrowed against |

| Death benefit | Paid only if you pass away during the term | Paid whenever you pass away |

| Best for | Income replacement, mortgages, raising kids: big needs with an end date | Lifelong needs: estate planning, a lifelong dependent, final expenses |

| Complexity | Simple and easy to compare | More features, more decisions |

Both are valuable tools. The right one depends on how long your need lasts, not on which product is fashionable.

How Much Term Life Insurance Coverage Do You Need?

A solid starting point is ten times your annual income, and then you adjust it to your real life. If you earn $75,000, that’s $750,000 of term life insurance coverage. It’s a rule of thumb, not gospel, but it gets most families surprisingly close, and it’s far better than guessing low. For a sharper answer than any online life insurance calculator gives you, walk through the DIME method.

DIME stands for the four things the money has to handle: Debt (everything but the house), Income (your annual income times the number of years your family needs it replaced), Mortgage (the full payoff balance), and Education (what you intend to fund for each child). Add those up, then subtract savings and any existing coverage that would truly be there. What’s left is your number.

Two adjustments people miss. First, a stay-at-home parent needs coverage too; childcare and household management have a real replacement cost the surviving parent would have to pay for. Second, Social Security survivor benefits help, but they rarely come close to replacing a full income, and they come with their own rules and limits. You can see what your family might receive at the Social Security Administration’s survivor benefits page, and then let your policy cover the rest of your financial obligations.

How Long Should Your Term Length Be?

Your term should last as long as your longest obligation: the mortgage, the years until your youngest child is independent, or the years until retirement savings can carry your spouse, whichever runs longest. Match the coverage window to the need and the policy does its job completely, then steps aside.

In practice that sorts people quickly. A new 30-year mortgage or a newborn usually points to a 30-year term. Kids in elementary school and a mortgage that’s half paid often point to a 20-year term life insurance policy, the single most popular choice in the country. Someone in their fifties bridging the last stretch to retirement may only need 10 or 15 years of term coverage.

One piece of math worth knowing: when in doubt, go longer. Buying a 20-year term life policy now and a new term at 50 almost always costs more in total than buying a 30-year term today, because the second policy is priced at an older age and whatever health you have then. The initial term you choose is the cheapest coverage window you’ll ever get.

A couple in their early thirties, a new baby, and a new 30-year mortgage.

This is the most common story that crosses my desk. Both parents work, the house runs on both paychecks, and until the baby came, life insurance never made the to-do list. We matched the term to the obligations: a 30-year term on each of them, sized near ten times income, locked in at the youngest and healthiest they will ever be. The monthly cost for both policies together landed in the range of a couple of streaming bundles, a fraction of what they’d braced for.

The best time to buy a term life policy is when the obligation starts, because your rate is set by the age and health you bring to the application, and it’s locked from that day forward.

What Factors Influence the Cost of Term Life Insurance?

The cost of term life insurance is set by factors like your age, your health, whether you use tobacco, and how much coverage you want for how long. Insurance companies are pricing one thing, the statistical risk of paying your claim during the term, and everything they ask flows from that.

Age leads the list, and it’s relentless: every birthday you wait, the same policy costs more, roughly doubling each decade for most healthy applicants. Health comes next; blood pressure, weight, cholesterol, and your medical history set your rate class, and the rate class sets your price. Tobacco and nicotine are the heavyweights, often doubling or tripling the premium, and yes, that includes vaping. Gender matters too, since women statistically live longer and pay a bit less. Then come occupation, hazardous hobbies, your driving record, the coverage amount, and the term length: a 30-year term costs more per month than a 10-year, because the insurer is on the hook through more of your life.

Here’s the encouraging part. A higher premium at one company is not a higher premium everywhere, because every carrier weighs these factors differently. That’s the whole reason shopping the market works, and it’s where a broker earns their keep. More on that below.

The biggest barrier to term life insurance isn’t the price. It’s the price people imagine.

How Much Does Term Life Insurance Cost?

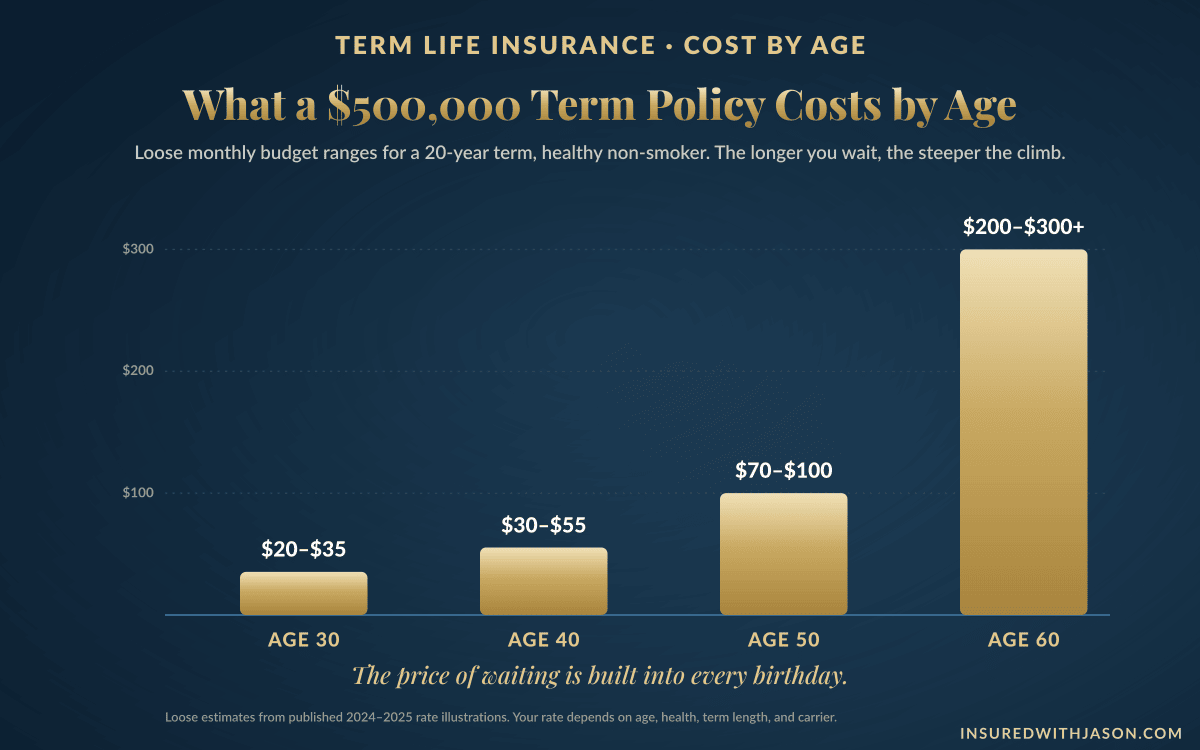

For a healthy non-smoker in their thirties, a $500,000, 20-year term policy often runs somewhere around $20 to $40 a month. That’s the figure that surprises almost everyone, and it’s why the cost of a term policy deserves real numbers instead of vague reassurance. Here’s roughly what that same $500,000 of coverage tends to run by age, based on published 2024 to 2025 rate illustrations. Treat these as loose budget ranges, not quotes; what you actually pay for term life insurance depends on your health, your term length, and the company.

Around age 30, plan on roughly $20 to $35 a month. Around 40, roughly $30 to $55. By 50, the range climbs to about $70 to $100, and by 60 it can run $200 to $300 or more. Term life insurance premiums climb steeply with age because every year of waiting hands the insurance company more risk. Read that progression once more and the lesson writes itself: the policy gets more expensive every year you think about it.

Smokers should expect two to three times these ranges, and anyone with health conditions will land somewhere that depends heavily on which carrier reviews the application. That spread between companies is real money, and it’s exactly why I shop the market rather than guess.

The same $500,000 policy, priced at four ages. The climb is the argument for buying now.

Curious what your real number looks like?

No exam needed to ask · No pressure · A real answer

Can You Get Term Life Insurance Without a Medical Exam?

Yes, and these days it’s the norm rather than the exception: about 59% of individual life insurance applications now qualify for a no-exam approval path called accelerated underwriting. Instead of needles and a nurse visit, the insurer checks your application against prescription history, motor vehicle records, and industry databases. Qualified healthy applicants get decisions in about five days on average, sometimes in minutes, and they earn the same preferred rate classes as exam-takers (Gen Re, 2025). Faster, not weaker.

Two other no-exam routes exist for different situations. Simplified issue uses a short health questionnaire and skips the databases’ deeper dive, trading a modestly higher premium for speed and simplicity. Guaranteed issue asks no health questions at all, accepts almost everyone in its age range, and charges the most per dollar of coverage with smaller limits; it’s a final-expense tool, not an income-replacement one.

Here’s how I’d frame the choice. If you’re healthy and patient, full underwriting with the exam usually buys the rock-bottom price. If you want $400,000 of coverage without blood work and weeks of waiting, there are strong products for exactly that, for a little more money. It comes down to your tolerance for hoops, and there’s a right answer for every tolerance level.

Two paths to the same policy: about five days without an exam versus about 23 days with one, and most applicants now qualify for the fast lane.

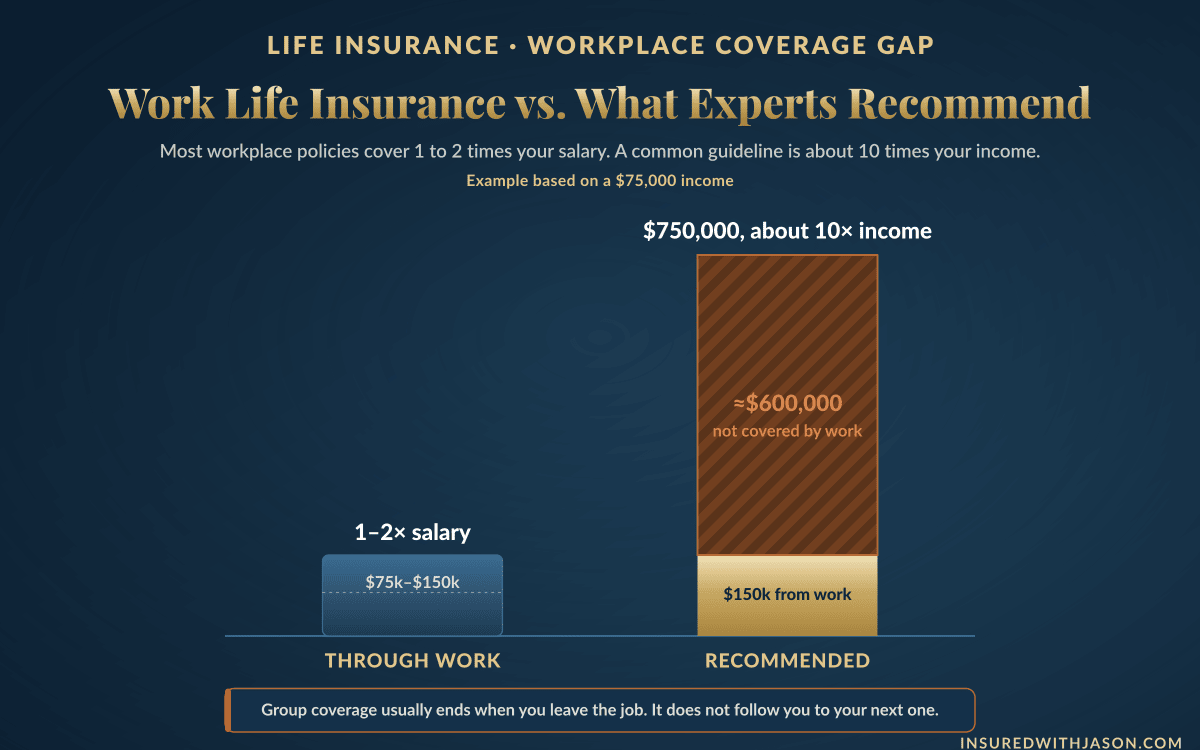

Is Life Insurance Through Work Enough?

For almost every family, no. Group life insurance through work is a nice benefit and a poor plan. The typical employer policy covers one to two times your salary, sometimes just a flat amount, while a family’s real need usually runs near ten times income. And the deeper problem isn’t the size. It’s that the coverage is welded to the job.

Think it through. If a serious illness ends your career, the diagnosis that makes you uninsurable is the same event that takes your group life away, right at the moment your family needs it most. In practice, coverage that disappears when you get too sick to work functions almost like accidental-only protection. I saw this up close in my railroad days, where the group coverage was a small amount, the kind of money that helps with a funeral and little else. Every employer is different, and that’s exactly the point: go find out what you actually have. Most people have never checked.

The fix is simple. Keep the free work coverage as a bonus, and own an individual term life insurance policy that follows you through every job change, layoff, and chapter of your life.

Group life insurance usually ends the day your employment does, and a serious diagnosis can take your job and your coverage in the same year.

By then, new coverage may be expensive or out of reach. Own a policy that belongs to you, not to your job, while you’re healthy enough to get it.

One to two times salary versus the roughly ten times experts recommend. The gap is the part your family would live with.

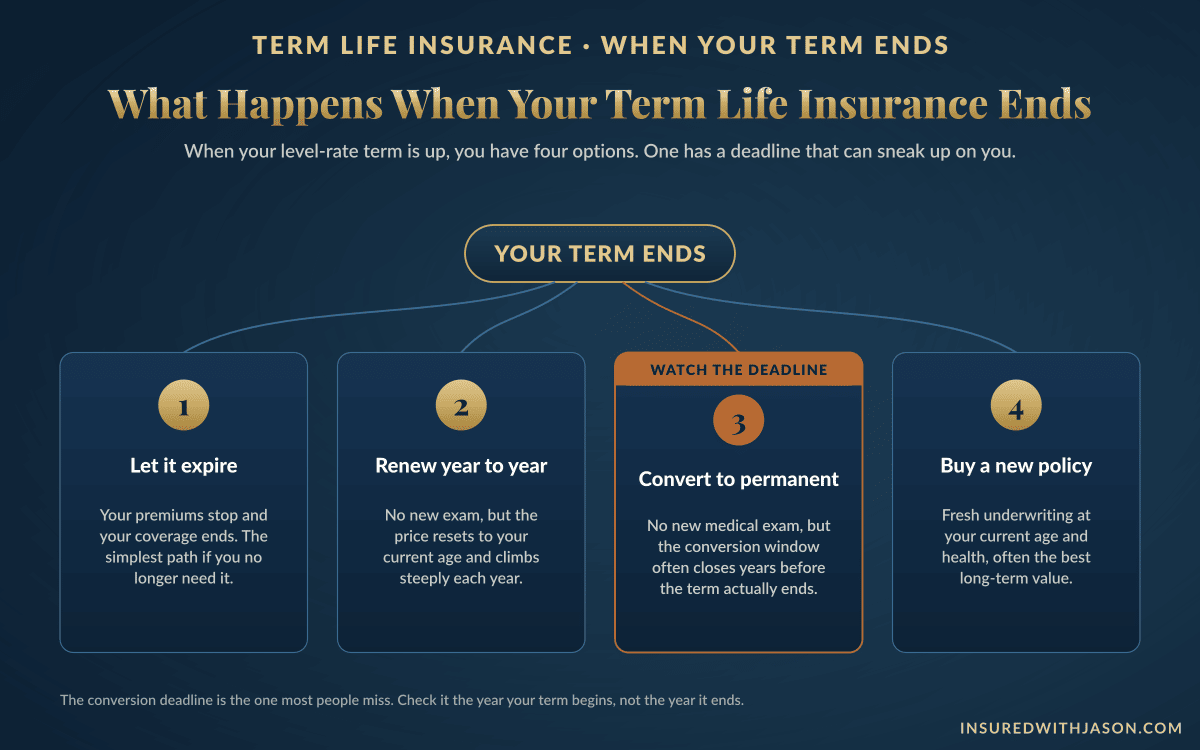

What Happens If You Outlive Your Term Life Insurance Policy?

If you outlive your term, the coverage ends, the premiums stop, and you choose one of four paths: let it go, renew it, convert it, or buy a new policy. Outliving the policy is the most likely outcome, and it’s the outcome you’re rooting for. Here’s what each path really looks like when your term life policy ends.

Let it expire. If the mortgage is paid, the kids are launched, and retirement savings can carry your spouse, the policy already did its job. Letting it go is often the right call, not a failure. Renew it. Many term policies renew year to year after the term expires, no new exam, but the premium resets to your current age and climbs steeply every year after. It’s a bridge, not a home. Convert it. The conversion privilege lets you move into permanent coverage with no medical questions, which can be priceless if your health has changed. But be prepared: permanent coverage at conversion-age pricing costs far more than the term did, and plenty of people who counted on converting decide the cost isn’t worth it once they see it. Buy a new term. If you’re still healthy and still have a need, a fresh policy at the end of your term is often cheaper than renewing or converting.

My honest advice: don’t make this decision alone or at the last minute. Sit down with a broker two to five years before the end of the term and ask the real question, which is not “should I keep this policy” but “what is the money for now?” Your needs at 55 are rarely your needs at 35. Sometimes the answer is convert, sometimes it’s a new term, sometimes it’s a different product entirely, and sometimes it’s a handshake and congratulations, you no longer need it.

On many term policies, the conversion window closes years before the term itself ends.

A 20-year policy might only allow conversion in the first ten. If your health changes in year fourteen, that right may already be gone. Find your conversion deadline now, while it’s just a date and not an emergency.

The four paths at the end of a term, and the one deadline that closes early.

Do You Get Your Money Back at the End of the Term?

On a standard term policy, no. If the term expires and you’re still here, the coverage ends and the premiums stay paid, the same way car insurance doesn’t refund you for the accident you never had. But there is a version built for people who can’t make peace with that: return of premium term, usually shortened to ROP.

ROP works exactly like level term with one addition. Outlive the term, and the insurance company refunds the premiums you paid, generally tax-free, in one lump sum at the end. You pay noticeably more for that guarantee. And I’ll be straight with you: if you ran the spreadsheet, buying cheaper standard term and investing the difference would often come out ahead. But ROP was never a play to save money, and judging it that way misses why people buy it.

ROP is a comfort and certainty play. It’s for the person who has a visceral reaction to renting insurance, who wants a sure thing down to the penny, who needs more death benefit than a whole life policy fits in the budget, and who knows themselves well enough to admit the “invest the difference” money would never actually get invested. Set it, forget it, and either way the money comes back to the family: as a death benefit if the worst happens, or as a check to you at the end of the term. It’s especially popular as mortgage protection on homes under half a million, because the policy guards the mortgage years, then hands back a lump sum that can put a serious dent in the remaining balance, or clear it entirely, years ahead of schedule. For the right buyer, that’s not a consolation prize. That’s the plan working.

A homeowner who hated the idea of “throwing money away,” and the policy built for exactly that feeling.

A couple with a mortgage in the $300,000s wanted it protected, but the husband couldn’t stand the thought of decades of premiums vanishing if nothing went wrong. Whole life coverage at the size they needed was more than the budget allowed. A 30-year return of premium term threaded the needle: the death benefit guards the mortgage the whole way through, and if they outlive the term, every premium dollar comes back in one lump sum they can throw straight at whatever balance remains. He stopped seeing the premium as rent and started seeing it as money parked with a bodyguard.

ROP costs more than standard term, and for buyers who want a guarantee instead of a maybe, that extra premium buys exactly what they came for: a sure thing.

What Happens If You Miss a Premium or Want to Cancel?

Miss a payment and you typically have about a 31-day grace period to catch up with no harm done; cancel and the policy simply ends, with nothing owed. Term insurance is refreshingly clean on both counts. There’s no cash value, so there are no surrender charges, no paperwork maze, and no penalty for walking away. You can stop any time.

The real danger is the accidental lapse. If the grace period passes unpaid, coverage ends, and getting it back through reinstatement usually means back premiums plus fresh health questions. If your health changed during the gap, you may face a higher premium or no offer at all. The protection you spent years paying for can disappear over one forgotten card update. Set the payment to auto-draft the day you take the policy, and if money gets tight, call your broker before the grace period runs out, not after. There are almost always options before a lapse; there are far fewer after.

5 Term Life Insurance Myths That Can Cost You

Most of what keeps people from buying term life insurance isn’t the product. It’s a handful of myths that sound reasonable and cost families dearly. Here are the five I hear most, against the facts.

Myth 1: “It’s too expensive”

The number one reason people give for skipping coverage, and the most wrong. Seventy-two percent of Americans overestimate the cost, and the youngest buyers overestimate it by ten to twelve times (LIMRA & Life Happens). Affordable life insurance isn’t a marketing phrase here; for healthy buyers, term really is the cheapest financial protection per dollar there is.

Myth 2: “I’m young and healthy, I don’t need it yet”

Young and healthy is precisely when to buy, because that’s the version of you the price is based on, forever. Every year you wait buys a higher premium, and one unexpected diagnosis can take the best rates, or any offer, off the table. Permanently.

Myth 3: “My coverage through work is enough”

Usually one to two times salary, usually gone when the job is. You read the full story above. Keep the work benefit; just don’t build the family’s future on it.

Myth 4: “I won’t qualify”

Most applicants do, and most never touch a needle: about 59% now qualify for no-exam accelerated approval. Even with health conditions, a decline at one company is often day-one coverage at another, because every carrier’s underwriting wants different things. Don’t disqualify yourself; that’s the underwriter’s job, and they say yes far more often than people expect.

Myth 5: “If I don’t die, the money was wasted”

Nobody calls their car insurance wasted after a year without an accident. You weren’t buying a payout; you were buying the certainty that the people you love were protected through every one of those years. And if the “nothing back” part truly bothers you, return of premium term exists for exactly your wiring.

How to Apply for Term Life Insurance, Step by Step

Applying for term life insurance takes about twenty to thirty minutes of your time, and the whole process, from quote to active policy, can run anywhere from a few days to a few weeks depending on the underwriting path. Here’s the road, start to finish, so nothing surprises you.

How to buy term life insurance, from quote to coverage

The path is simpler than most people expect, and most of it happens without you.

- 1Size ItSettle your coverage amount and term length

Use the ten-times-income rule or the DIME method from above. This decides everything else.

- 2Shop ItGet a quote for term coverage across multiple companies

Prices for the same person vary widely between life insurance companies. This is where a broker earns their keep.

- 3ApplyComplete the application, honestly and completely

Health, lifestyle, medications, beneficiaries. About 20 to 30 minutes. Honesty here is what makes the claim bulletproof later.

- 4If RequiredTake the medical exam, free, at your home

About 30 to 45 minutes, paid for by the insurer. Many applicants skip this step entirely through accelerated underwriting.

- 5Wait SmartUnderwriting assigns your rate class

Days for no-exam paths, a few weeks for full underwriting. Your broker can advocate if the offer comes back off-target.

- 6ReviewCheck the offer, then use your free look

Confirm the coverage amount, term, premium, and rate class. You get at least 10 days to return the policy for a full refund.

- 7Lock It InPay the first premium and set auto-pay

Coverage is live. Tell your beneficiaries where the policy lives, and never think about the price again. It’s locked.

The benefits booklet said “life insurance.” The fine print said one times salary.

A father in his forties told me he was all set; he had life insurance through work. We pulled the benefits summary together and found what I usually find: coverage equal to a single year of salary, owned by the employer, gone if he ever left or lost the job. Against a mortgage and two kids, it would have covered months, not years. He kept the free work benefit and added his own term policy sized to the real need, one that belongs to him no matter where he works.

Before you count on group life, read what you actually have. Most people who check discover the number is far smaller than the peace of mind it was giving them.

How an Independent Broker Finds You the Best Term Life Insurance

An independent broker works for you, not for any one company, which means the whole market gets shopped to fit your situation instead of your situation getting bent to fit one company’s products. A captive insurance agent can only offer what their employer sells. I can compare how dozens of term life insurance companies would treat you, and that difference shows up in dollars.

Here’s why it matters so much. Every carrier’s underwriting wants different things to grant its best rate class, the category that yields the lowest cost. A health condition that gets a decline at one company can be day-one coverage at a preferred rate at another. My job is matching your specific picture, your health, your coverage need, your budget, to the company that treats that picture best. Done right, it usually lands one of two ways: a much higher death benefit for the budget you’d already set, or the death benefit you wanted for noticeably less.

The match goes beyond price, too. Some people want every hoop jumped for the rock-bottom rate. Others would happily pay a little more to skip the blood work and the waiting entirely. Some need a straightforward level term policy; others are better served by return of premium or a decreasing term tied to a mortgage. There’s no single best life insurance company, only the best one for you, and finding it is a genuinely custom process. That’s the work, and I like the work.

In all my years doing this, nobody has ever told me they regretted buying term life insurance. The only regret I ever hear is about waiting.

Get a Quote for Term Life Insurance

Getting a quote for term life insurance takes a few minutes and commits you to nothing. To run real numbers, all I need is your date of birth, your state, whether you’ve used tobacco or nicotine in the past year, a general sense of your health, and the coverage amount and term length you’re considering. From there I can show you what the market actually offers someone in your shoes, including the no-exam options, side by side.

One thing worth knowing before you compare anything: a quote is an estimate, and the final price comes from underwriting. The advertised rates you see online assume perfect health. The number that matters is the one a real application produces, which is exactly why we select term life insurance companies based on how they’ll actually treat your application, not on whose ad is prettiest. You’ve done the reading. Now let’s get term coverage priced for the one person this page was always about: you.

Term life insurance: frequently asked questions

The questions people ask me most, answered plainly.

Is the term life insurance death benefit taxable? +

Generally no. Life insurance death benefits paid to a named beneficiary are received income-tax-free under federal law. Very large estates can involve estate tax questions, so talk with a tax professional if that applies to you.

What does term life insurance cover? Does it pay for any cause of death? +

Term life insurance covers death from virtually any cause, including illness, accident, and natural causes, once the policy is in force. The standard exceptions are suicide within the first two policy years and claims involving material misrepresentation on the application.

Is there a waiting period before a term policy pays out? +

No. A fully underwritten term policy covers you from the day it goes in force. The two-year contestability period lets the insurer verify the application was truthful if a claim happens early, but it does not delay or reduce honest claims.

Can I have more than one term life policy at the same time? +

Yes. Owning multiple policies is common and useful. Some people layer or ladder policies, pairing a large 20-year term for the heavy obligation years with a smaller 30-year term for the longer tail, which can cost less than one giant long policy.

What happens if I stop paying for term life insurance? +

You typically get a grace period of about 31 days to catch up while coverage continues. After that, the policy lapses and coverage ends. Reinstatement may be possible afterward, but it usually requires back premiums and new health questions, so auto-pay is your friend.

Can I convert my term policy to permanent insurance later? +

Many term policies include a conversion privilege that lets you convert to permanent coverage with no new medical exam, within a set window. That window often closes years before the term ends, so check your policy for the exact deadline now rather than when you need it.

What is the most popular term length? +

The 20-year term, which accounts for roughly 40% of level term policies sold in the United States according to LIMRA sales data. It lines up with the heart of most families’ mortgage and child-raising years.

If my health improves, can I get a better rate on my term life insurance? +

Often, yes. If you quit tobacco for twelve months or more, lost significant weight, or got a condition well controlled, you can apply for a new policy at a better rate class, and some insurers will reconsider your existing rate class on request. It costs nothing to ask.

Let’s find the term policy that fits your life

You came here wondering what term life insurance really costs and whether it fits you, and now you know more than most people ever learn before they buy. The next step takes minutes: tell me about your situation, and I’ll shop the market and show you real options side by side, including the no-exam paths. Your rate is set by the age and health you have today, which makes today the cheapest day you’ll ever see.

This article is for educational purposes only and is not legal, tax, or financial advice. Coverage, costs, and rules for life insurance plans vary by person, company, and state. All premium figures shown are loose estimates from published rate illustrations, not quotes. Please speak with a licensed professional about your specific situation before making a decision.