Medicare Supplement Plans: The Complete Guide for 2026

What a Medicare Supplement (Medigap) does, what it costs, when to enroll, and how to choose the right plan — explained in plain English by an independent broker.

Most people looking into a Medicare Supplement are after a few specific answers. What does it actually do? What’s it going to cost me? Can I even get one? And how is it different from a Medicare Advantage plan?

Stay with me and you’ll have all four — how a Medicare Supplement works, what it costs in 2026, who can get one and when, and where it parts ways with Medicare Advantage. Enough to make this decision sure of yourself, instead of second-guessing later whether you got it right.

A Medicare Supplement — most people call it Medigap — is a private policy that pays the part of your medical bills Medicare doesn’t. Original Medicare is great coverage. It pays most of your costs, but not all of them, and there’s no limit on what you can be left owing in a year with a lot of medical bills. Picture Original Medicare as a cloud that catches most of the storm but still lets that 20% fall. A supplement is the umbrella underneath it, between the leak and you. And because it’s your umbrella, you’re not stuck standing under one store’s awning — you can walk straight through the rain to any doctor or hospital you choose that takes Medicare.

I’ve helped a lot of families since 2005, and I’ve sat across from people in the exact spot you’re in right now — wanting to understand this and get it right the first time. I get it. Medicare isn’t anyone’s idea of a fun afternoon. But give me a few minutes and it’ll make sense, so you can act on it instead of just nodding along.

- A Medicare Supplement, or Medigap, is private insurance that pays the gaps Original Medicare leaves you — deductibles, coinsurance, and copays.

- The plans are standardized by the government. A Plan G from one company covers exactly what a Plan G from the next one covers. Only the price and the company change.

- You can use any doctor or hospital in the country that takes Medicare. No networks, no referrals, no permission slips.

- The best time to buy is your six-month Medigap open enrollment period — the one window when any company must say yes, at the healthy-person price, with no health questions.

- Miss that window and, in most states, an insurer can check your health and turn you down.

- Once you’re approved, the policy is guaranteed renewable for life. Pay the premium and they can’t drop you.

- Medicare Supplement plans don’t include drug coverage. You add a separate Part D plan for that.

- Most new buyers land on Plan G or Plan N. The right one is the one that fits you, not the one on a list.

What is Medicare Supplement insurance?

A Medicare Supplement is a private policy that pays the part of your medical bills Original Medicare doesn’t. Medicare pays first. Your supplement pays second. That’s the whole job.

People call it Medigap because that’s exactly what it does — it fills the gaps Original Medicare leaves. And those gaps are bigger than most people expect.

Original Medicare comes in two parts. Part A covers hospital stays. Part B covers doctors and outpatient care. Together they pay a large share of your bills, but they leave the deductibles, and they leave your 20% of most Part B costs, to you. Your Medicare Supplement steps in and picks up some or all of what’s left, depending on the plan.

Three things to know now, so nothing catches you off guard later. A Medicare Supplement insurance plan is sold by private insurance companies, not the government. It only works with Original Medicare — you can’t pair it with a Medicare Advantage plan. And once you’re in, it’s yours for life: as long as you pay the premium, the company can’t drop you or raise your rate just because your health changes.

Key Medicare Supplement terms, explained

How does a Medicare Supplement plan work?

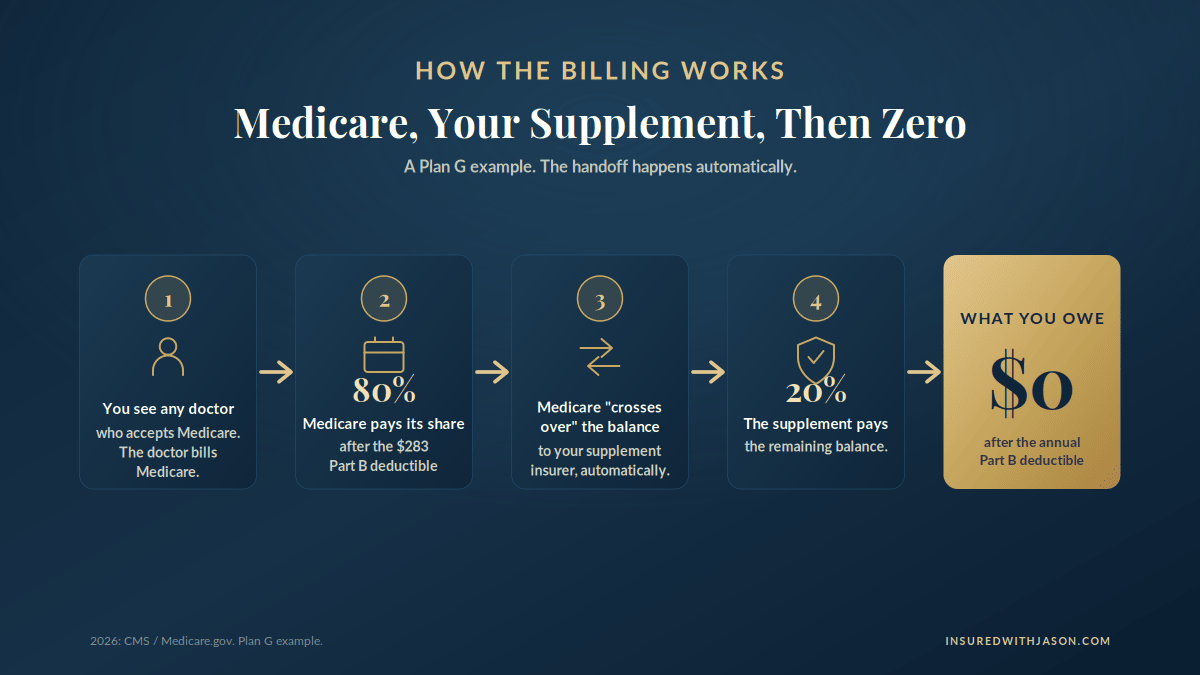

A Medicare Supplement pays second, and it happens on its own. Here’s the whole path the next time you walk into a doctor’s office.

- You see any doctor or hospital that takes Medicare, and they bill Medicare.

- Original Medicare pays its share of the approved amount.

- Medicare passes the rest straight to your Medigap insurer. They call that a crossover, and it’s automatic.

- Your Medicare Supplement plan pays its part, based on the plan you chose.

- You owe little or nothing.

You don’t file anything for most of this. The bill moves from Medicare to your supplement on its own, behind the scenes, before it ever reaches your mailbox.

Two things to keep straight. You still pay your monthly Medicare Part B premium — $202.90 in 2026 — because a supplement sits on top of Original Medicare, it doesn’t replace it. And there’s no network. If a provider takes Medicare, your plan works there, no matter which of the insurance companies sold it to you.

Here’s the part that matters most. On its own, Original Medicare puts no limit on your out-of-pocket costs. That 20% just keeps falling, with no bottom to it. A Medicare Supplement is the umbrella that catches it, so a year with a lot of medical bills stays a number you can plan for, instead of one that keeps climbing.

How a Medicare Supplement pays: Medicare first, your supplement second, little or nothing left for you.

What does a Medicare Supplement cover, and what doesn’t it cover?

A Medicare Supplement pays the cost-sharing built into Original Medicare. It doesn’t pay for extras like drugs, dental, vision, hearing, or long-term care. Which gaps it fills comes down to the plan letter, but the pattern is the same across all of them.

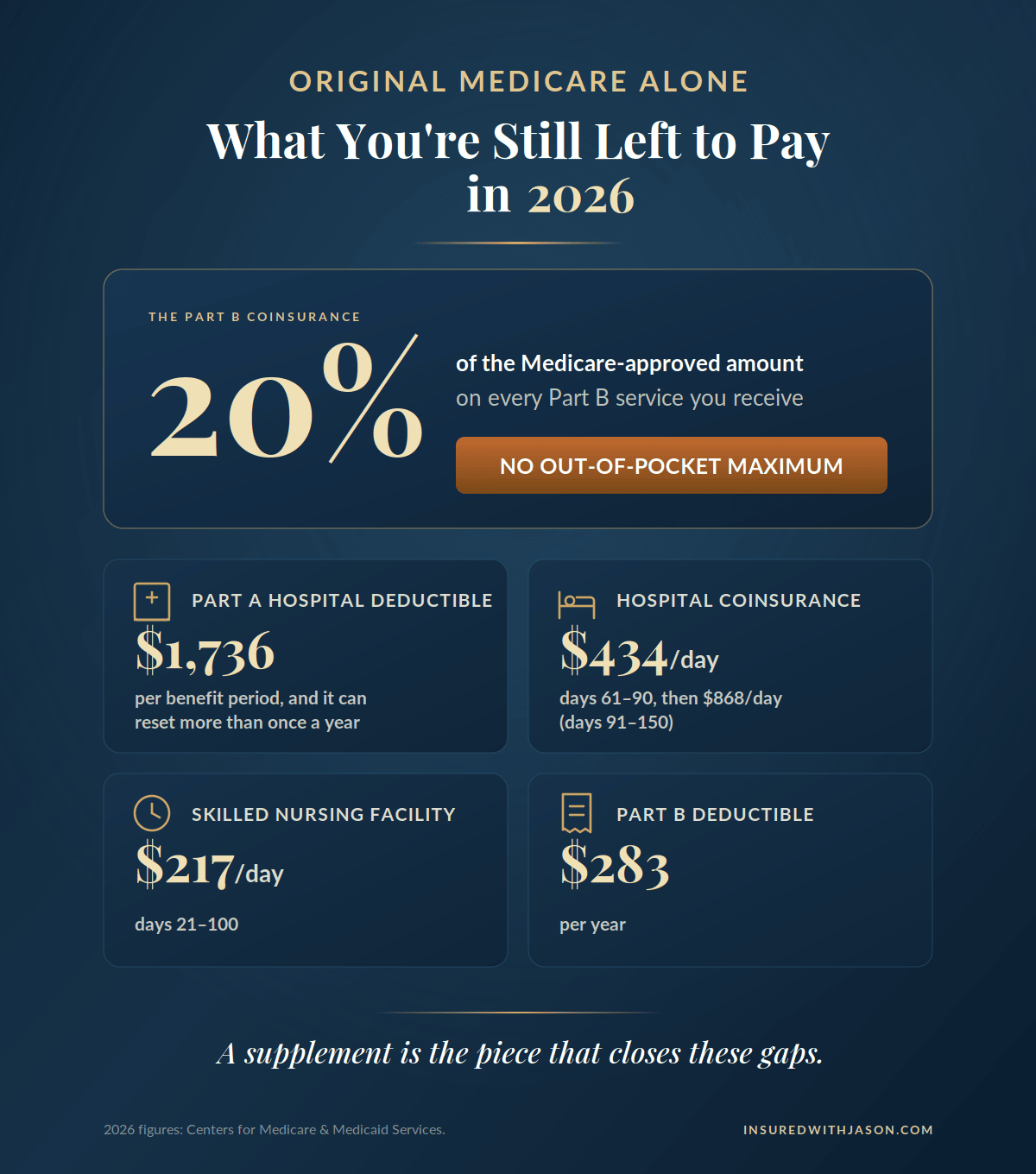

Here’s what Medicare Supplement plans cover, depending on the plan: the Medicare deductibles, like the Part A hospital deductible, plus hospital coinsurance and 365 extra hospital days after Medicare’s own run out. Your 20% Part B coinsurance. Skilled nursing coinsurance, the first three pints of blood, and hospice coinsurance. Most mid- and higher-level plans also pay 80% of emergency care when you travel outside the country, and Plan F and Plan G cover Part B excess charges.

Here’s the logic on the other side: if Original Medicare doesn’t cover something in the first place, your supplement won’t either. Anything not covered by Original Medicare is on you, or on separate coverage. That list includes prescription drugs (that’s a separate Part D plan), routine dental, vision, and hearing, long-term care in a nursing home, private-duty nursing, and cosmetic work.

One rule ties it all together. A supplement only pays after Medicare pays. If Medicare turns down a service as not medically necessary, your supplement turns it down too. So a Medigap plan isn’t a loophole around the rules — it’s the partner that covers your share of the costs that Original Medicare already approved.

What Original Medicare leaves you to pay in 2026 — including a 20% share with no yearly limit.

What are the different Medicare Supplement plans (A through N)?

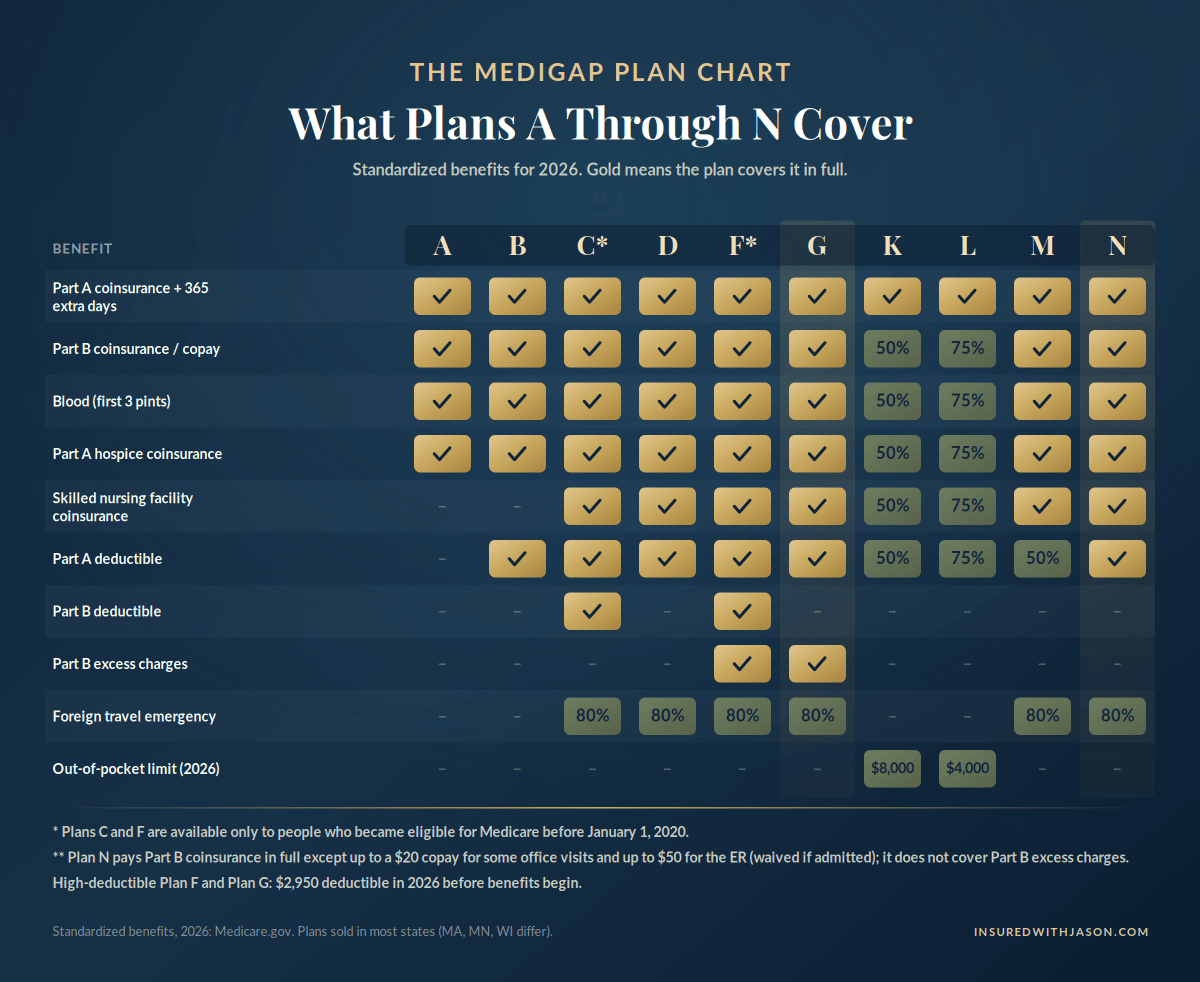

There are ten standardized Medigap plans, lettered A through N, and the law sets exactly what each plan covers. That’s the good news — you don’t have to decode anyone’s fine print. The plan type sets the benefits, not the company, so a Plan G is a Plan G no matter who sells it.

Most people shopping today choose one of three: Plan G, Plan N, or High-Deductible Plan G. Here’s the plain difference.

Plan G covers everything a supplement can, except one thing — the yearly Part B deductible, which is $283 in 2026. You pay that once, and your covered costs are handled for the rest of the year. It’s the most complete plan a new enrollee can buy, and it’s the most popular.

Plan N is much like Plan G, with two small trade-offs in exchange for a lower premium: a copay up to $20 for some office visits and up to $50 for an emergency room trip, waived if you’re admitted, and it doesn’t cover Part B excess charges. For many people those are small, predictable costs that are well worth the monthly savings.

High-Deductible Plan G keeps the lowest premium of the three. You cover your own costs up to $2,950 in 2026, and after that it pays like the standard version. It tends to fit people who are healthy now and mainly want protection against one very expensive year.

A few more details round out your plan options. Plan A and Plan B are the most basic. Plans K and L work differently — they cover a set share of your costs up to a yearly out-of-pocket cap, $8,000 for Plan K and $4,000 for Plan L in 2026. Medicare SELECT is a lower-cost version that asks you to use certain hospitals. All ten Medigap policies share the same lettered system, so the plan benefits are identical from one company to the next. Not all plans are available in every state.

Two plans come with a timing catch. Plan C and Medicare Supplement Plan F are no longer sold to anyone who became eligible for Medicare on or after January 1, 2020. If you became eligible for Medicare before January 1, 2020, you can keep — and in some areas still buy — a Plan C or Plan F. Plans C and F covered the full Part B deductible, and that’s the piece the rules changed for anyone who became eligible for Medicare on or after January of that year.

Three states — Massachusetts, Minnesota, and Wisconsin — set up their plans their own way, so the letters there don’t match the rest of the country. Everywhere else, these are the different Medicare Supplement plans available to you, the types of Medicare Supplement plans set by federal law.

So which is the best plan? It’s the same answer as the best diet: the best one is the one that fits you and that you’ll actually stick with. The right Medicare Supplement plan matches how you use care and what you’re comfortable paying. Want the fewest moving parts and almost nothing to think about? That points to Plan G. Fine with small copays to keep the premium lower? Plan N. Healthy, and mainly guarding against one bad year? High-Deductible Plan G. There’s no single best Medicare plan for everyone, and that’s exactly where a good broker earns their keep — helping you find the one that fits your life.

What every Medigap plan, A through N, covers in 2026.

Not sure which plan fits you?

No pressure · A straight comparison · A real answer

Who is eligible for a Medicare Supplement plan?

If you have Original Medicare — both Medicare Part A and Part B — you can apply for a Medicare Supplement. That’s the core rule. A few situations are worth spelling out.

You need both Medicare Parts A and B in place. You can’t hold a supplement and a Medicare Advantage plan at the same time, so if you’re leaving Advantage, you’d move back to Original Medicare first. And if Medicaid already covers your costs, a supplement is usually unnecessary.

Being under 65 changes the picture. People who become eligible for Medicare early because of a disability can often buy a Medicare Supplement, but the rules are uneven from state to state. Some states require insurers to offer at least one plan to Medicare beneficiaries under 65, sometimes at a higher price. A growing number cap that price at the standard age-65 rate. And some states don’t require an offer at all.

If you enroll in Medicare through disability, here’s the one thing to hold onto: this is a different set of rules, and they depend entirely on where you live. It’s worth a real conversation with a broker before you decide, so you keep every one of the Medicare benefits and the Medicare coverage you’re entitled to. One bright spot — when someone who came on early turns 65, they get a brand-new six-month window and a fresh chance at any plan, with no health questions.

When can I enroll in a Medicare Supplement plan?

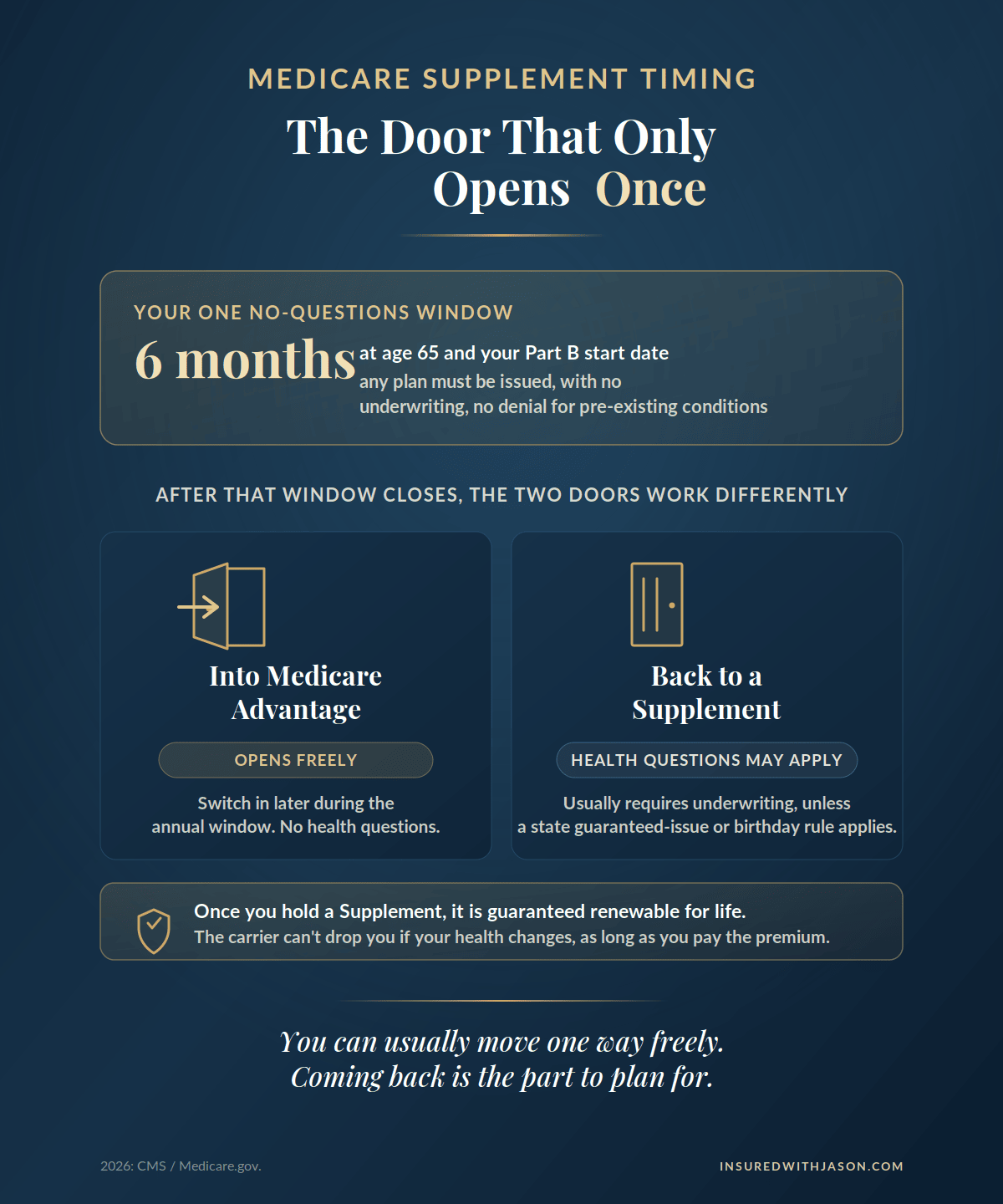

The best time to buy is your Medicare Supplement open enrollment period — a one-time, six-month window that opens the month you’re both 65 or older and enrolled in Part B. If you remember one thing from this whole guide, make it this one.

During those six months, you hold every card. No company can turn you down, ask a single health question, or charge you more because of your health. You can pick any Medigap plan sold in your state, and your coverage starts right away. This is the one stretch of time when the door is open to everyone, healthy or not.

Here’s what trips people up: this window comes once. It is not the Medicare enrollment you hear about every fall — that one is for Medicare Advantage and Part D. Your Medigap open enrollment period happens a single time, and when it closes, the rules change. In most states, an insurer can start asking about your health before they’ll sell you a plan.

There’s a backstop called a guaranteed issue right. Certain life events — losing employer coverage, a Medicare Advantage plan pulling out of your area, or a trial run that didn’t fit — open a short window, usually about 63 days, when a company must sell you a plan with no health questions. A few states go further and let you switch each year without a health review, and a couple allow it year-round. The rules vary by state, so it’s worth asking what protections you have where you live before you enroll in a Medicare Supplement.

You can move into Advantage almost anytime; coming back to a supplement usually means a health review.

A lot of people assume they can buy a supplement anytime, the way they shop for car insurance.

In most states, you can’t. Once your six-month window closes and no guaranteed issue right applies, an insurer can review your health and decide. Pick the coverage you’d want if your health changed, while the door is still open to you.

Picture someone who signs up right on time.

She enrolls in Part B at 65, feels healthy, and chooses a Plan G during her open enrollment window. A couple of years later, she gets the kind of news no one wants — a serious diagnosis that means specialists, a hospital stay, and months of follow-up care. Because she’s on a supplement, she sees the specialists she wants and gets into the hospital she trusts, with no fight for permission first. And when the bills come, her share is small — roughly her premium plus that one yearly Part B deductible, about $283 in 2026. Those numbers are an example, not a quote, but the shape of it is real.

Had she waited and missed her window, that same diagnosis is often the very thing that would have made a supplement hard to get later.

What is Medicare Supplement underwriting outside open enrollment?

Outside your open enrollment window, and without a guaranteed issue right, most states let an insurer review your health before they decide. That review is called medical underwriting.

When insurance companies underwrite your application, they look at your health history and ask detailed questions. From there, they can approve you, approve you at a higher rate in some states, or turn you down. Serious heart, lung, kidney, or neurological conditions, and some recent cancers, commonly lead to a decline — though every company draws the line a little differently.

I’ll tell you why this matters, plainly, without trying to scare you. The healthier you are, the more doors are open to you — and they’re open widest during your open enrollment window. If you’re well right now, that’s your moment of greatest freedom to choose.

And here’s the reassuring side. Once you’re approved and in, Medicare Supplement policies are guaranteed renewable for life. The company can’t drop you or single you out for a rate increase because your health changed. You’re in for good. There’s also a protection called creditable coverage: if you had steady health coverage before, with no long gap, an insurer generally can’t make you wait to cover a condition you already had.

How much does Medicare Supplement insurance cost in 2026?

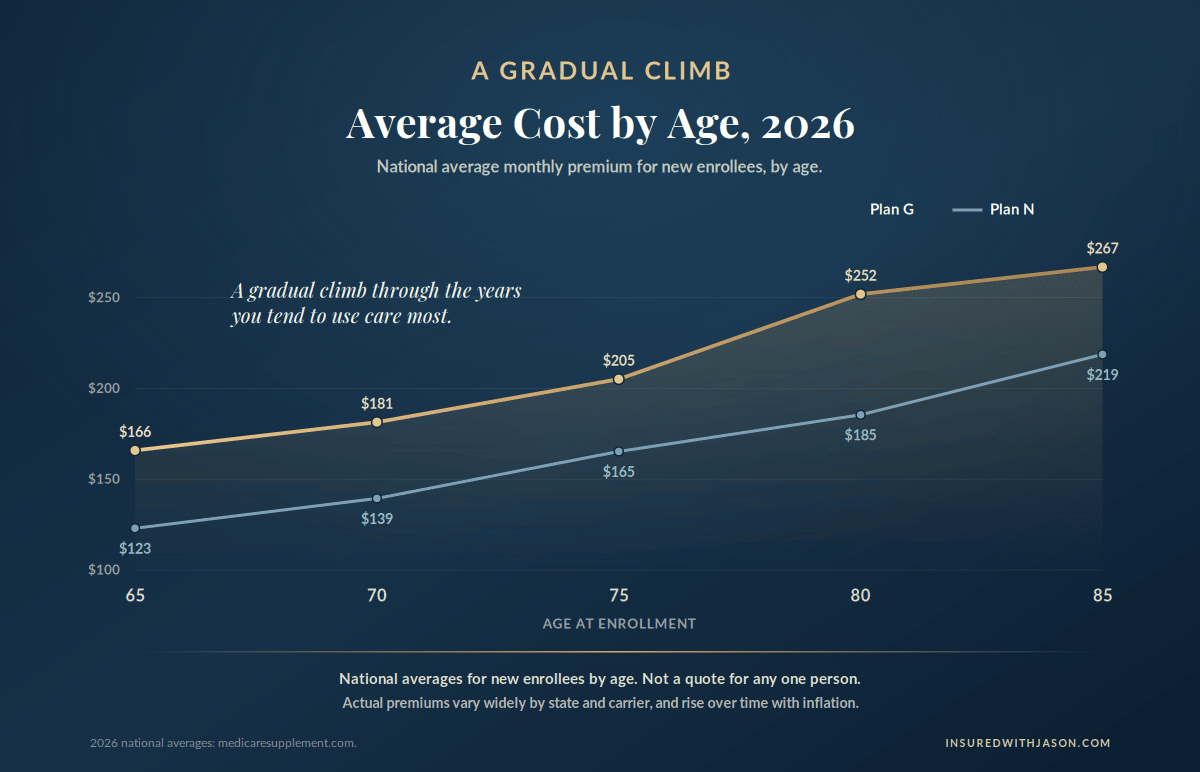

What a Medicare Supplement insurance premium costs depends on the plan, your age, your sex, whether you use tobacco, your state, and how the company prices it. As a national-average starting point for a 65-year-old in 2026, Plan G runs about $166 a month and Plan N about $123.

Treat those as averages, not a quote. Where you live moves the number a lot — some states are surprisingly inexpensive, others run high, and two people the same age in different zip codes can pay very different premiums for the exact same plan. The only way to know your real cost is to compare actual quotes for your area.

Keep your costs in three separate buckets, because they really are separate. The Medicare Supplement premium is its own payment to the insurance company. If you want the full monthly picture, here are the three pieces, side by side, so no one blurs them into a single scary number:

- The Medicare Part B premium you pay Medicare: $202.90 a month in 2026 for most people.

- Your Medicare Supplement premium, paid to the insurance company — for example, the Plan G average above.

- A separate Part D drug plan premium, which varies by plan.

One savings move people miss: many insurance companies offer a household discount, often 5% to 12%, when two adults in the same home each carry a policy. It never hurts to ask.

What stands out in those averages is how gently the cost rises with age — a slow, steady climb through the years when most people lean on their coverage the most. Two honest notes, so nothing reads the wrong way. This is what a new buyer pays at each age, not one person’s bill tracked over the years. And a real premium also drifts up over time with inflation, the way most prices do. Cost-of-living raises to your Social Security check may cover some of that increase, though that changes year to year. Either way, good Medicare Supplement coverage stays one of the steadiest costs you’ll carry in retirement.

Average Medicare Supplement premiums by age in 2026 (new enrollees; national averages, not a personal quote).

How does IRMAA affect your Medicare costs?

If your income is above a certain line, you pay an extra amount on top of your Part B and Part D premiums. That extra is called IRMAA. It doesn’t change your Medicare Supplement premium, but it’s part of your total Medicare cost, so it belongs in your planning.

IRMAA stands for the income-related monthly adjustment amount. In 2026 it starts above $109,000 in income for a single filer and $218,000 for a married couple filing jointly. The higher your income, the larger the surcharge, and at the very top the Medicare Part B premium can reach about $689.90 a month instead of the standard $202.90.

One detail catches people off guard. IRMAA looks at your tax return from two years earlier, so your 2026 amount is based on your 2024 income. A one-time event — selling a property, a large withdrawal from a retirement account, a Roth conversion — can raise your Medicare cost two years down the road. If your income dropped because of a life change like retirement, you can ask Medicare to use your current income instead.

Why do Medicare Supplement premiums increase over time?

Premiums rise over time, and how fast they rise depends a lot on how the plan is priced. There are three pricing methods, and knowing which one you have tells you what to expect.

Attained-age pricing ties your premium to your current age, so it goes up a little every year as you get older. It usually starts the lowest, which is why it’s the most common. Issue-age pricing locks your premium to the age you were when you bought it, so it doesn’t rise just because you had a birthday — only for broader inflation. Community-rated pricing charges everyone in the area the same, no matter their age.

On top of the pricing method, insurance companies can raise rates across the board to keep up with medical costs and claims. This is where shopping smart pays off. A company with the lowest price today, but a history of steep yearly increases, can cost you more down the road — often right when a change in your health makes it hard to switch. A company’s rate-increase history is public, and it’s worth far more than a few dollars saved on day one.

There’s a quieter factor too. When a plan closes to new buyers, the way Plan F did, no younger, healthier people are joining to balance the pool, so those plans tend to climb faster over time. It’s one more reason a plan that’s still open to new buyers, like Plan G, tends to hold its rate better than an older Medigap plan that’s been closed off.

How does Medicare Supplement work with Part D drug coverage?

A Medicare Supplement doesn’t include prescription drug coverage, so you add a separate Part D plan for your medications. They’re sold apart on purpose, and they work side by side.

Part D got a major upgrade in 2026. For the first time, there’s a hard cap on what you pay out of pocket for covered drugs — $2,100 for the year — and once you hit it, your prescription drug plan covers the rest. Insulin is capped at $35 a month, and the national base premium for a Medicare Part D plan is about $38.99, though plans vary.

How do I avoid the Part D late enrollment penalty?

Sign up for drug coverage on time, even if you don’t take a single pill today. If you go 63 days or more without creditable drug coverage after you become eligible, Medicare adds a permanent penalty to your Part D premium for as long as you have a plan.

The monthly amount is small, but it never goes away, and it grows the longer you wait. A low-cost drug plan at 65 almost always costs less than the penalty would. One catch worth knowing: some coverage people assume counts, like COBRA, usually doesn’t count as creditable, so check before you rely on it.

Medicare Supplement vs. Medicare Advantage: what is the difference?

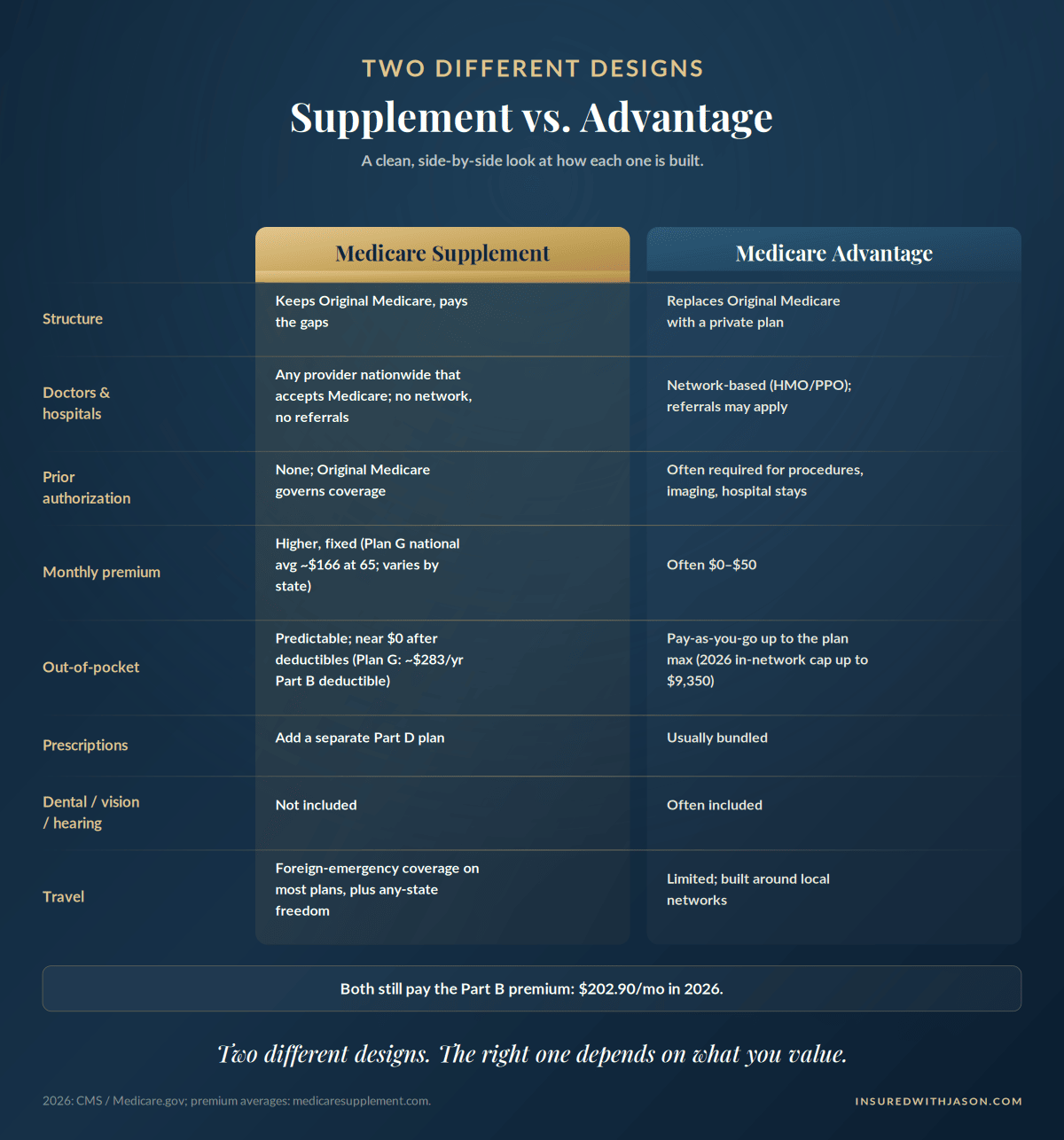

A Medicare Supplement and a Medicare Advantage plan are two different roads, not two versions of the same thing. A Medicare Supplement keeps you on Original Medicare and pays the gaps, so you can see any provider that takes Medicare. A Medicare Advantage plan replaces Original Medicare with a private health plan that bundles your coverage and usually runs through a network of doctors and hospitals.

Let me be upfront about where I stand, so you know who’s talking. Medicare Supplements are what I specialize in, and what I offer across the country. I’ve worked with both Medicare Advantage and Medicare Supplements over the years, so what you’re about to read is a fair comparison, not a pitch for one side. I just want you to understand the difference well enough to make your own call.

Most people come to Medicare already knowing the Advantage name, because most new enrollees choose it — often for the low or zero monthly premium and the bundled extras like dental and vision. For a lot of people, that’s a sensible choice, especially when a supplement premium would stretch the budget too thin. There’s no wrong person here. There’s only the plan that fits your life.

When people weigh Medicare Advantage and Medicare Supplements, it really comes down to two things: how you get your care, and how your costs behave. The table lays them side by side.

| Medicare Supplement | Medicare Advantage | |

|---|---|---|

| Structure | Keeps Original Medicare and pays the gaps | Replaces Original Medicare with a private plan |

| Doctors & hospitals | Any provider nationwide that takes Medicare; no network, no referrals | Network-based; referrals may apply |

| Prior authorization | None — Original Medicare governs coverage | Often required for procedures and hospital stays |

| Monthly premium | Higher, fixed (Plan G averages about $166 at 65; varies by state) | Often $0–$50 |

| Out-of-pocket | Predictable; near $0 after deductibles (Plan G: about $283/yr) | Pay-as-you-go up to the plan max (2026 in-network cap up to $9,350) |

| Prescriptions | Add a separate Part D plan | Usually bundled |

| Dental, vision, hearing | Not included | Often included |

| Travel | Foreign-emergency coverage on most plans; any-state freedom | Built around local networks |

Both still pay the Part B premium ($202.90/mo in 2026). Cost figures: CMS / Medicare.gov. Premiums shown are 2026 national averages.

Medicare Supplement and Medicare Advantage, side by side.

One timing fact deserves its own line, because it surprises people. You can move into a Medicare Advantage plan later, during the fall enrollment window, with no health review at all. But moving back to a supplement usually means passing medical underwriting, unless your state gives you a special right. The door swings open easily one way, and not so easily back — and that’s worth knowing before you choose.

Is a Medicare Supplement right for you?

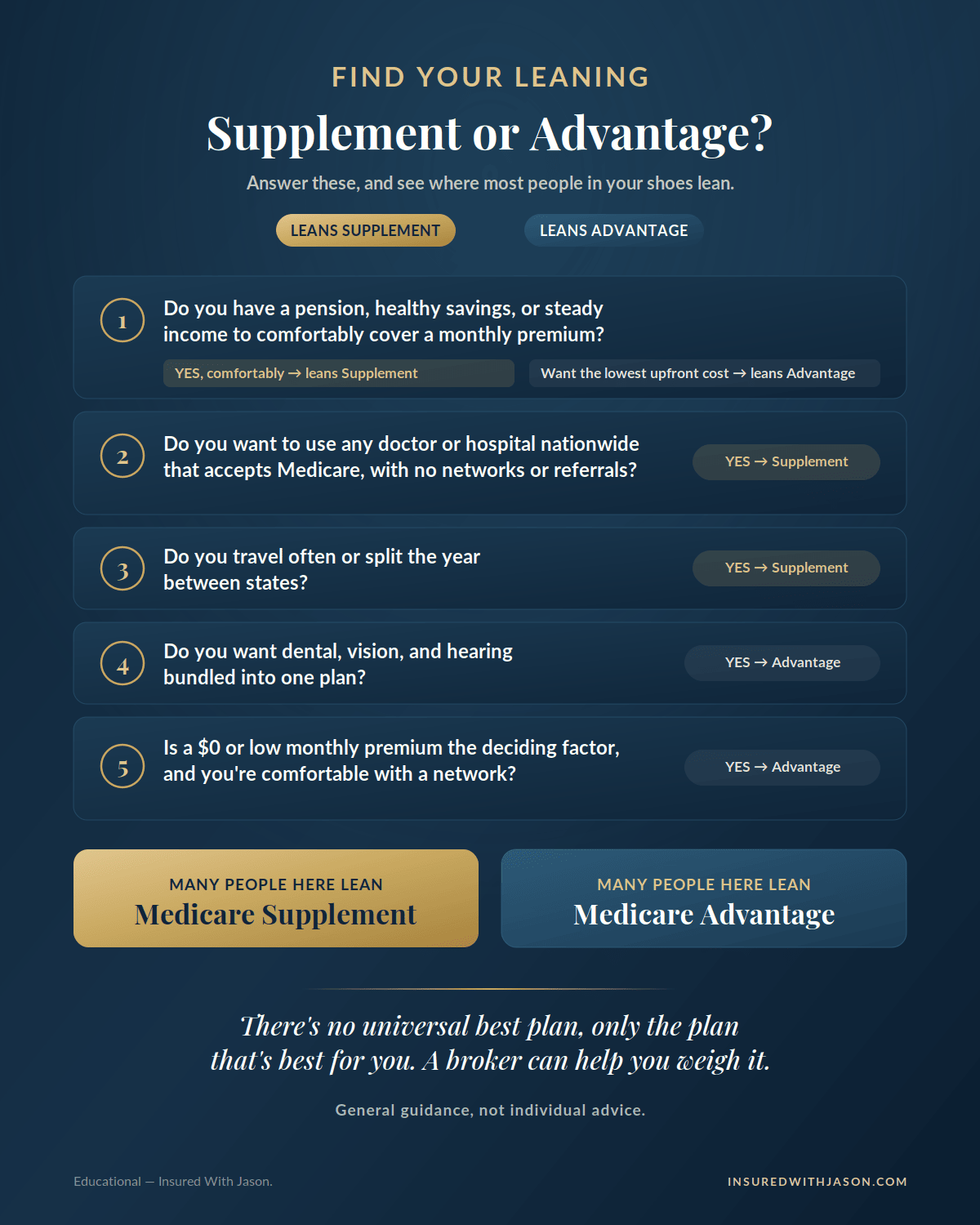

There’s no wrong person here, only the plan that fits your life. Here’s the honest read on where a Medicare Supplement tends to fit, and where another option might serve you better.

- Want to see any doctor or specialist in the country that takes Medicare, with no network.

- Travel often, or split the year between two states.

- Want costs you can count on, with little or nothing owed after your deductible.

- Have serious health needs, or simply worry about what may come, and want coverage that can’t push you out once you’re in — and can carry the premium.

- Are healthy at 65 and want to lock in your options while the door is open.

- Need the lowest possible monthly cost, and a supplement premium would stretch you.

- Are comfortable staying within a local network of doctors and hospitals.

- Want dental, vision, and hearing bundled into one plan.

A quick guide to which path tends to fit — general guidance, not individual advice.

Here’s a story that plays out more often than people expect.

Someone picks a zero-premium Advantage plan at 65, because free sounds good, and who could blame them. It serves them fine for a while. Then something shifts — a referral that takes too long, or a new diagnosis — and they decide they’d rather have a supplement and the freedom that comes with it. So they apply. But now they’re outside their open enrollment window, and the health review doesn’t go their way. I’ve talked with good people who wanted to come back to a supplement and couldn’t, only because of timing.

It takes nothing away from Advantage, which did exactly what it was built to do. The lesson is just this: the move into Advantage is easy to make and harder to undo, so make it with both eyes open.

How do I shop for a Medicare Supplement plan?

Because the plan benefits in each letter are identical from one company to the next, you shop on four things — price, the company’s rate-increase history, its financial stability, and its service — not on the benefits themselves. That makes this simpler than it looks.

How to shop for a Medicare Supplement, step by step

Since the benefits are set by law, your job is to find the company that offers your plan at the best price with the steadiest rates.

- 1Start HerePick the plan letter that fits how you use care

For most new buyers, that’s Plan G, Plan N, or High-Deductible Plan G.

- 2CompareFind the companies that sell that letter in your state

Since the benefits are identical, you’re comparing price, company to company.

- 3AskAsk about pricing method and rate history

How do you price the plan, and what have your increases looked like the past several years?

- 4SaveAsk about a household discount

Many companies knock off 5% to 12% when two adults in a home each carry a policy.

- 5ApplyApply during a protected window

Your open enrollment window or a guaranteed issue period, and answer every health question honestly.

A couple of things make this easier. An independent broker or licensed insurance agent who isn’t tied to one company can compare many at once, instead of showing you a single company’s shelf. Your State Health Insurance Assistance Program offers free, unbiased state health insurance help, and Medicare’s official guide to health insurance for people with Medicare lays the plans out in black and white. And after you buy a Medicare Supplement, you generally get a 30-day free look — so never cancel your old policy until the new one is firmly in place.

What are the most common Medicare Supplement mistakes to avoid?

Most of the regret I see traces back to a handful of avoidable mistakes. Knowing them ahead of time is most of the battle.

- Waiting past your six-month window, then trying to buy after a health problem has already shown up.

- Shopping only on today’s lowest price, and ignoring the company’s rate-increase history.

- Assuming you can switch Medigap plans anytime — in most states, switching later means a health review.

- Skipping Part D when you take no medications, and triggering the permanent late-enrollment penalty.

- Choosing a plan for how healthy you are today, instead of the coverage you’d want if that changed.

- Mixing up Medicare’s fall enrollment period, which is for Medicare Advantage and Part D, with your one-time Medigap window.

A Medicare Supplement turns an open-ended medical bill into one steady monthly cost you can plan around.

Medicare was the first thing I ever specialized in, back in 2005. And I didn’t learn it from a textbook. My mom has been on Medicare since she was 31 — I was six when she was diagnosed with multiple sclerosis. I grew up inside this system, watching what it does for a family that needs a lot of care.

That’s why I care about getting it right. I’ve seen what good coverage alongside Medicare can do: the freedom to see the right specialist, to get into the right hospital, without fighting for permission first. A Medicare Supplement isn’t for everyone, and I’ll always tell you so. But for someone with serious health needs, or someone who just worries about what’s coming, and who can carry the premium, it can be one of the best calls they make — because once you’re in, no one can push you out.

No insurance touches a person’s life more than their Medicare. Helping someone make sense of it, in plain words, so they walk away steady instead of overwhelmed — that’s the part I love. It’s why this guide exists.

Medicare Supplement insurance: frequently asked questions

The questions people ask me most, answered plainly.

Is a Medicare Supplement the same as Medicare?

No. Medicare is the federal program. A Medicare Supplement is private insurance you buy separately to cover what Original Medicare doesn’t pay.

Do I need a Medigap plan if I’m healthy?

A supplement is mostly about protecting you from large, unexpected bills, not day-to-day care. Since the buying window is set by your age, not your health, many people enroll at 65 while the door is open, no matter how they feel.

Can I be charged more for my health during open enrollment?

No. During your six-month Medigap open enrollment period, a company can’t deny you or charge more based on your health.

Can I switch Medicare Supplement plans later?

Sometimes, but it’s not guaranteed. Outside your open enrollment window, a guaranteed issue right, or a state rule like a birthday rule, switching usually means passing a health review.

Does a Medicare Supplement cover prescription drugs?

No. You add a separate Part D plan for medications.

Does it cover dental, vision, or hearing?

No. Standard Medicare Supplement plans don’t cover routine dental, vision, or hearing. Those are handled separately.

Can an insurer drop me if I get sick?

No. Once your policy is issued, it’s guaranteed renewable for life as long as you pay your premium.

Can I have a Medicare Supplement and Medicare Advantage at the same time?

No. A supplement works only with Original Medicare. You can’t use both at once.

Do I still pay the Part B premium if I have a supplement?

Yes. The Medicare Part B premium — $202.90 a month in 2026 for most people — is paid to Medicare no matter which supplement you carry.

What is a benefit period?

It’s how Part A counts a hospital stay. It starts when you’re admitted and ends after 60 days out. Go in again later and a new benefit period, with a new deductible, can begin.

Let’s find the Medicare Supplement that fits you

You came here to understand Medicare Supplements, and now you know enough to make a confident call instead of a rushed one. The next step is simple: let’s look at your real situation — your health, your state, and what you want your coverage to do — and compare your actual options side by side, with no pressure either way. The best day to sort this out is while your options are still wide open.

This article is for educational purposes only and is not legal, tax, or financial advice. Coverage, costs, and rules for Medicare Supplement plans vary by person, company, and state. Please speak with a licensed professional about your specific situation before making a decision.