What is Life Insurance? The Ultimate Guide

What it is, what it really costs, and how to buy it right, explained by an independent broker who works for you.

Life insurance is the only thing you’ll ever buy hoping you never use it. A few dollars a month, and an insurance company puts it in writing: if you don’t come home one day, your family’s world doesn’t collapse. Picture your house at six in the evening. Lights on, dinner going, somebody arguing about homework. All of it runs on a paycheck, and this is what keeps it standing if the paycheck stops. The mortgage gets paid. The kids stay in their schools. The funeral never touches a credit card.

Nobody shops for this for fun. A baby came home, a mortgage closed, a parent is getting older, or someone died too young with nothing in place. Whatever brought you here, this page answers it all in plain English: what life insurance really costs, term or whole, qualifying with a health history, the policy at work, covering a parent. I’ve helped families through these decisions since 2005. Let’s get you your answers.

- A life insurance death benefit is generally income-tax-free to your named beneficiary under IRS rules.

- About 102 million American adults say they need life insurance or need more of it, a record high (LIMRA).

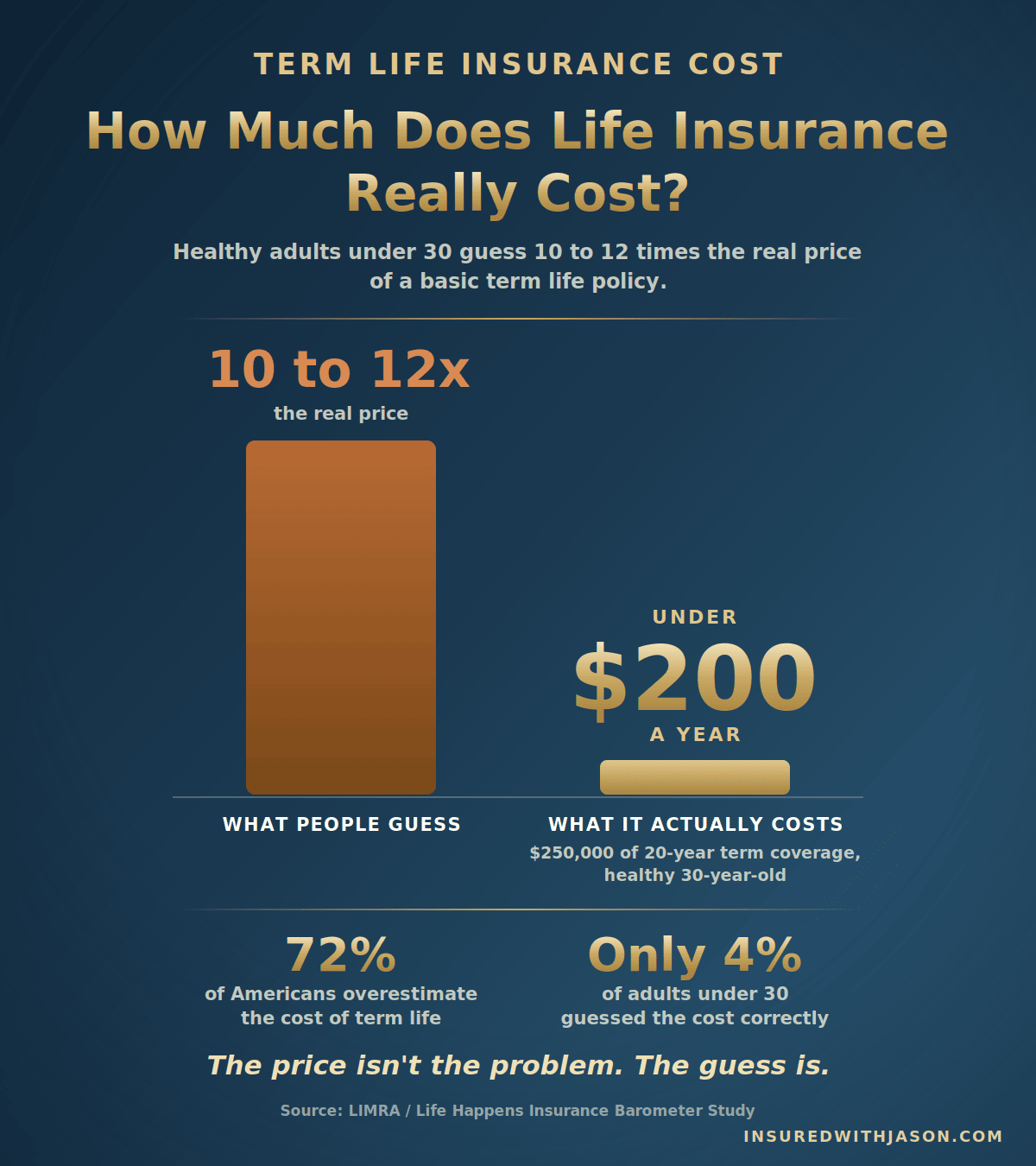

- 72% of Americans overestimate what term life costs; adults under 30 guess 10 to 12 times the real price.

- A healthy 30-year-old can often get $250,000 of 20-year term coverage for under $200 a year.

- Employer group life insurance usually covers only 1 to 2 times your salary and rarely follows you to your next job.

- There’s no discount for skipping a broker. The same policy from the same company costs the same either way.

- Estates under roughly $15 million (the 2026 federal exemption) generally owe no federal estate tax on the payout.

What is Life Insurance?

Life insurance is a contract between you and an insurance company: you pay a premium, and when the insured person passes away, the company pays the people you name a lump sum called the death benefit. That’s the whole machine. Life insurance provides money at the exact moment a family needs it most, and in nearly every case it arrives free of federal income tax; the IRS confirms it directly. And if you ever read British money advice, the same product goes by life assurance. Same promise, different accent.

Three roles sit on every life policy, and they aren’t always the same person. The insured is the person whose life is covered; their passing is what triggers the claim. The owner controls the policy and pays for it. Usually that’s the insured, but not always: an adult child can own a policy on a parent. The beneficiary is the person, trust, or charity who receives the money. Name a primary and a backup.

One rule ties the three together: the owner needs an insurable interest in the insured, a real financial or family stake in their life. You can insure your spouse or your mother. You can’t insure a stranger.

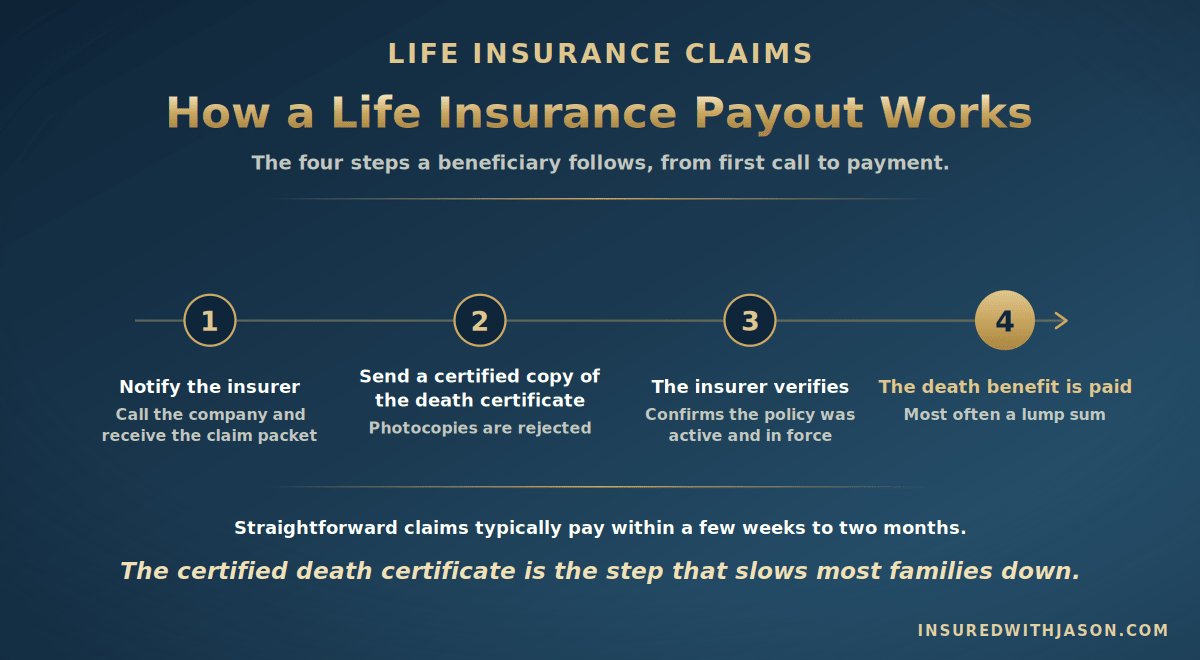

So how does a payout actually work? Almost nobody explains this part. Your beneficiary notifies the company and files a claim form with a certified copy of the death certificate; photocopies get rejected. The company confirms the policy was active and paid up, then pays, almost always in one lump sum. Straightforward claims typically pay within a few weeks to two months.

Two more things worth knowing up front. Most policies carry a two-year contestability period, a window where the company can double-check the application for honest answers, so tell the whole truth on day one. And this isn’t some new or fragile promise. Life insurance is one of the oldest financial products in America; the New York life insurance market was paying claims before the Civil War, and the life insurance industry paid $89 billion to beneficiaries in 2024 alone.

From claim to check: most straightforward life insurance payouts arrive within a few weeks to two months.

Why get a life insurance policy?

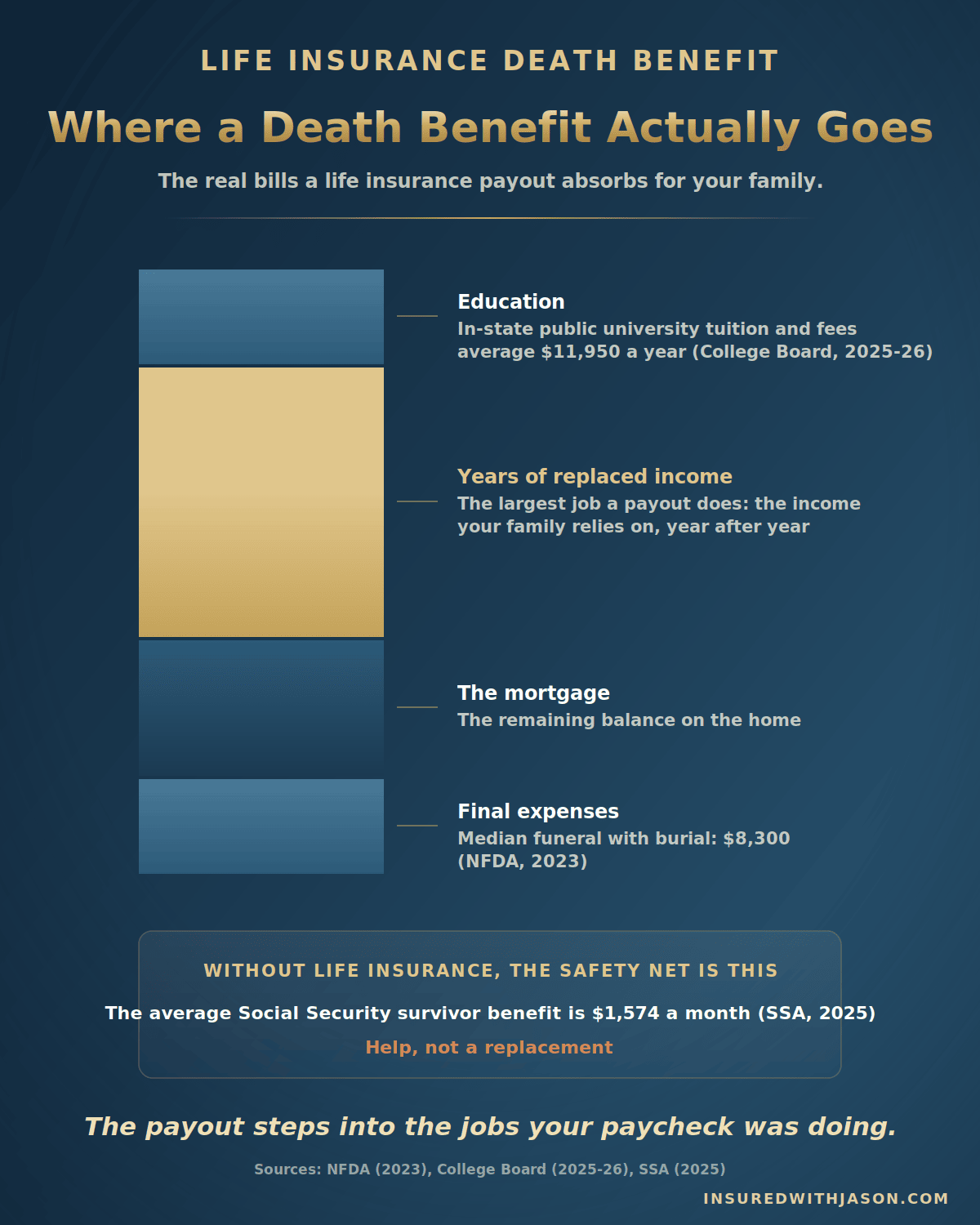

You get a life insurance policy because the bills don’t stop when a paycheck does. In LIMRA’s research, nearly half of American households say they’d face financial hardship within six months of losing their primary wage earner. One in four say within a single month. The median funeral with burial runs $8,300 before the first ordinary bill even shows up. And Social Security helps, but the average survivor benefit is about $1,574 a month, which doesn’t carry a mortgage, a car payment, and groceries in most of the country.

Life insurance can help close that entire gap at once. A death benefit can replace years of income, pay off the house, retire the debts, fund a college account, and cover the funeral, all without waiting on probate. When you purchase a life insurance policy, what you’re really buying is time. Time to grieve. Time to rebuild. Time without a financial countdown running underneath the loss.

Who should consider life insurance?

Anyone whose death would leave a financial hole in someone else’s life should consider life insurance. In practice, that’s most of us at some point.

Parents of minor children carry the classic case: income, childcare, and the cost of raising kids all land at once, and all of it needs replacing. Spouses and partners usually run the household on two incomes while the fixed bills stay fixed; losing half the income doesn’t cut the mortgage in half. Homeowners hold the biggest bill a family has, and it doesn’t pause for grief. Business owners use it two ways: key-person coverage protects the company if a vital person dies, and a buy-sell agreement funded by life insurance gives the surviving partners cash to buy out the family’s share cleanly.

Adult children planning for aging parents deserve their own line, because this one is close to my practice. You can buy life insurance on a parent: your mom or dad is the insured and answers the health questions, and you can be the owner, the payor, and the beneficiary. It’s one of the most common and least talked-about insurance needs in America, and it means the funeral never lands on the family’s credit cards. And anyone with co-signed debt should look too; a co-signed balance can outlive the borrower and land on you.

One payout, four jobs: final expenses, the mortgage, years of income, and education. Social Security’s $1,574 average survivor benefit can’t carry them alone.

What are the 3 types of life insurance?

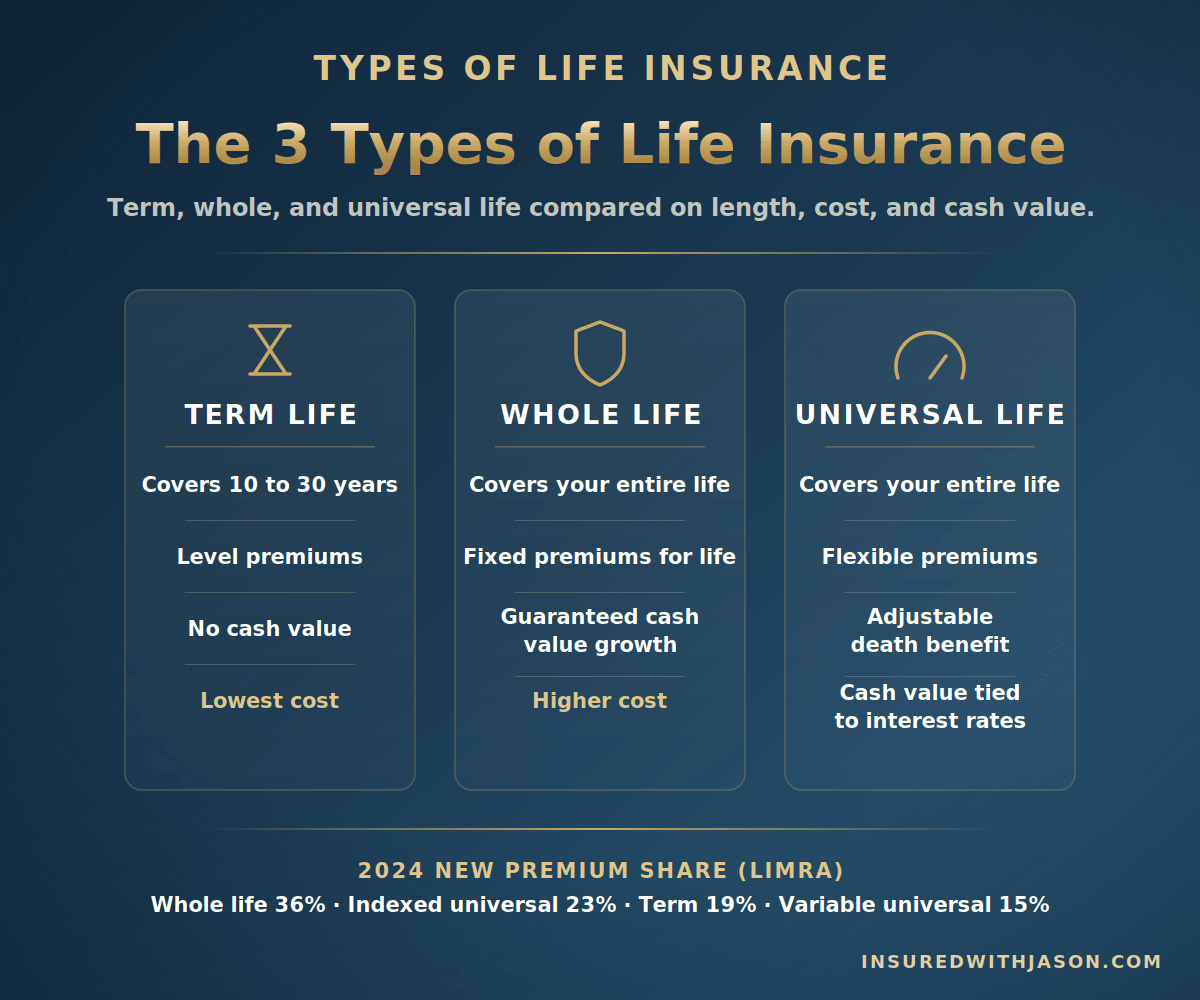

The 3 main types of life insurance are term life, whole life, and universal life. Every policy you’ll ever be offered is one of these or a variation on it, so once you know the three, the whole market gets simpler. The real fork in the road is term and permanent life insurance: coverage for a season of life, or coverage built to last as long as you do.

Term life insurance covers a set period, usually 10 to 30 years, with level premiums the whole way. There’s no cash value; it’s pure protection, which is exactly why it costs so little. Term insurance is designed for the years when the stakes are highest: kids at home, a mortgage on the house, one paycheck doing heavy lifting. Outlive the term, and coverage simply ends. (Here’s the full term life guide.)

Whole life insurance is permanent life insurance with absolute guarantees: premiums fixed for life, a death benefit that never shrinks, and cash value that grows on a guaranteed, tax-deferred basis you can borrow against. Whole life insurance policies cost more per dollar than term life insurance policies, and in exchange they never expire. People keep whole life policies for final expenses, estate planning, and the certainty itself. (Here’s the full whole life guide.)

Universal life insurance is also permanent, with flexible premiums and an adjustable death benefit. The cash value in universal life insurance policies earns interest, and each month the policy’s internal cost of insurance comes out of it. That flexibility cuts both ways: universal life policies need watching, because if the cash value runs dry the policy can lapse. Variable universal life insurance and indexed universal life tie growth to the market or an index, and variable life insurance carries real market risk. Each is its own deep subject, and this page won’t pretend to cover them in a paragraph.

Across the different types of life insurance, here’s how 2024’s new premium dollars split, per LIMRA: whole life 36%, indexed universal 23%, term 19%, variable universal 15%. Permanent policies dominate the dollars. Term dominates the policy count, because it costs so much less per dollar of protection.

| Term life | Whole life | Universal life | |

|---|---|---|---|

| How long it lasts | 10–30 years | Your entire life | Your entire life |

| Premiums | Level for the term | Fixed for life | Flexible |

| Death benefit | Guaranteed during the term | Guaranteed | Adjustable |

| Cash value | None | Guaranteed growth | Interest-based; can vary |

| Relative cost | Lowest | Highest | In between |

| Often fits | Young families, mortgage years | Lifelong needs, final expenses, estates | Permanent need with premium flexibility |

2024 new premium share (LIMRA): whole life 36% · indexed universal 23% · term 19% · variable universal 15%.

Term, whole, and universal life at a glance: duration, premiums, cash value, and cost.

Three ways to get life insurance coverage

You can get life insurance coverage three ways: through work, direct from a single company, or through an independent broker. The products exist either way. What changes is how much of the market you actually see.

Through work. Group life insurance is the most common starting point in America, and it’s a genuinely good perk: your employer often pays for a base amount, usually one to two times your salary, with no health questions asked. The catch? These insurance plans are tied to the job. Leave, get laid off, or retire, and the coverage usually stays behind. More on that gap in a minute, because it bites more families than almost anything else on this page.

Direct from one company. You can buy straight from a single carrier, often through a captive insurance agent who represents that company alone. The process can be quick, and the agent can know that product line cold. The trade-off is the menu: you’ll only ever see that one company’s insurance options. One honest nuance from inside the business: a few companies sell certain products only through their own agents, so a captive agent can occasionally offer something a broker can’t.

Through an independent broker. An independent broker isn’t tied to any one company. I compare the carriers you actually qualify for in your state, route your application to the company whose underwriting treats your health history best, and I work for you, not the carrier.

Skipping the broker doesn’t save you a penny.

Life insurance premiums are filed with state regulators. If the same company offers the same policy through its own agent and through an independent broker, the price is identical. Going direct doesn’t buy a discount; it only shows you less of the market.

How much life insurance do I need?

Most people need about ten times their income in life insurance, and the DIME method turns that rough guess into your real number. DIME is the math behind nearly every life insurance calculator online, and it walks your actual insurance needs one category at a time.

D is debt: every balance that wouldn’t die with you, like credit cards, car loans, and co-signed student loans. I is income: your annual income times the years your family would need it; ten years is a common starting point, and until the youngest finishes school is a better one. M is mortgage: the payoff balance on the house, so your family keeps their home free and clear. E is education: what you intend to contribute per child, knowing in-state public tuition and fees alone now average about $11,950 a year.

Add the four up, subtract what you already have in savings and coverage in force, and you’ve got your target. Two notes before you run your own numbers. You may see mortgage life insurance marketed alongside your home loan; it pays the lender the remaining balance, while a level term policy sized to the mortgage can do the same job with your family, not the bank, in control of the money. And stay-at-home parents need coverage too. Replacing the childcare, the driving, and everything else they hold up has a real price, and the surviving spouse would have to pay it.

What factors determine the cost of a life insurance policy?

Six things determine the cost of a life insurance policy, and you control more of them than you’d think.

Age is the biggest single driver. Insurance rates climb with every birthday, gently at first, then hard after forty-five, and your rate locks in at the age you apply. Health class is the biggest controllable one: underwriters sort applicants into rate classes, from Preferred Plus down through Standard, based on blood pressure, weight, cholesterol, and medical history, and that class sets your life insurance premiums more than anything else you can influence. Tobacco and nicotine change everything; smokers commonly pay two to three times what non-smokers pay, and yes, most companies count vaping the same way.

The last three are the policy itself. Coverage amount: a million-dollar policy costs more than a $250,000 one, though the cost per dollar usually drops as the amount rises. Term length: a 30-year term costs more than a 10-year term because the company carries your risk deeper into life. Type of policy: permanent coverage costs more than term for the same death benefit, because it’s guaranteed to pay eventually and builds cash value along the way. Gender plays a role too; women typically pay a bit less than men of the same age and health, reflecting longer life expectancy.

How much does life insurance cost?

Life insurance costs less than almost everyone guesses. The most reliable public number comes from LIMRA: a healthy 30-year-old can typically get $250,000 of 20-year term coverage for under $200 a year. Hold onto that anchor the next time life insurance costs come up at a kitchen table, because the debate is usually built on a guess that’s ten times too high.

Treat every number you read online, including that one, as an estimate. Your real price depends on your age, your health class, your coverage amount, your term length, and which company runs the math. That’s also why you won’t find a big rate table on this page pretending to be your price. The cost of insurance is personal, and pretending otherwise is how people end up disappointed.

Here’s the part to actually use: you don’t have to live on estimates. A licensed broker can put a real quote in front of you, down to the penny, in five to ten minutes. Not sixty minutes. Not a callback next week. Five to ten minutes to know exactly what you’d pay if approved.

How badly healthy adults under 30 overestimate the price of a $250,000 term life policy. Only 4% guessed it right.

Source: LIMRA / Life Happens Insurance Barometer Study

The guess vs. the reality: people picture ten times the price of $250,000 in term coverage at age 30.

Stop guessing your price.

Down to the penny · 5–10 minutes · No pressure

Do I need a medical exam to get life insurance?

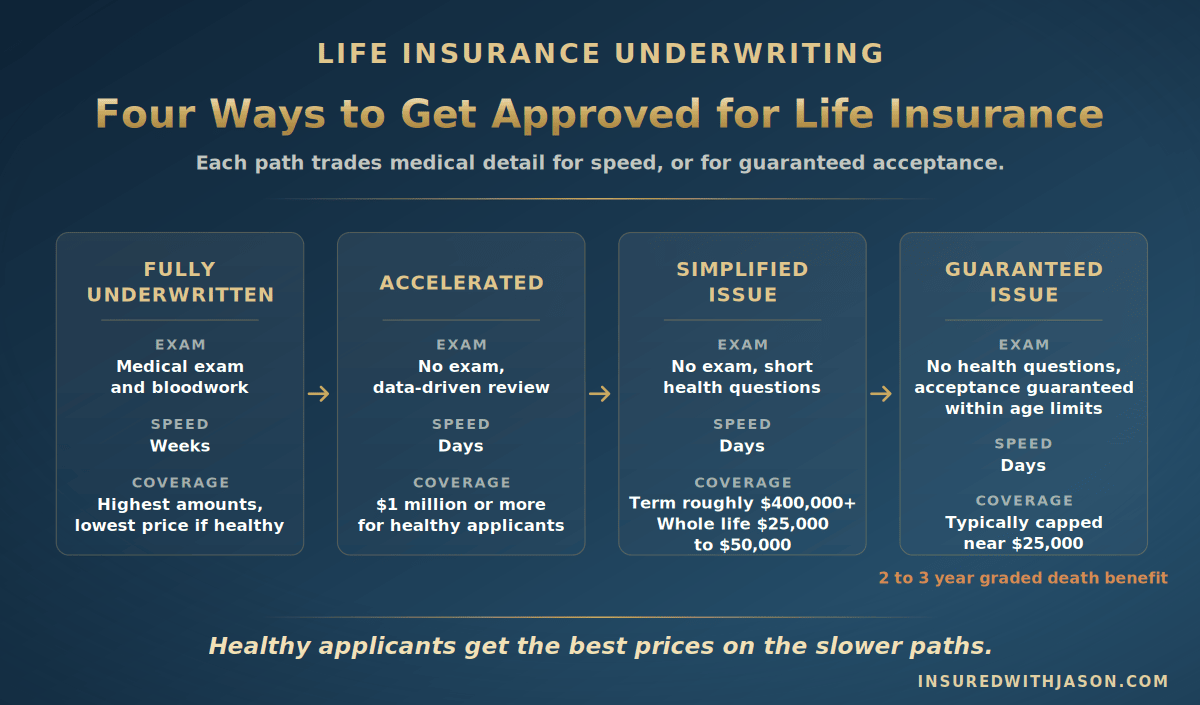

No, you don’t always need a medical exam to get life insurance. There are four paths through underwriting, and they trade thoroughness for speed or for a guaranteed yes. Pick the lane that fits your health and your patience.

Fully underwritten is the traditional path: a short paramedical exam (height, weight, blood pressure, a blood and urine draw), a detailed questionnaire, and a records review. It takes a few weeks, supports the highest coverage amounts, and delivers the lowest prices for healthy applicants.

Accelerated underwriting skips the exam entirely. The company verifies your answers against prescription and data records and can make instant term life decisions in minutes for healthy applicants, often up to $1 million or more, at pricing close to fully underwritten rates. And it’s quickly becoming the norm for younger, healthier buyers.

Simplified issue means no exam, just a short set of health questions. On the term side, no-exam term life coverage now reaches roughly $400,000 or more with some companies. On the whole life side, simplified issue policies typically top out around $25,000 to $50,000. You can still be declined based on the answers, but approval often comes in days.

Guaranteed issue asks no health questions at all; acceptance is guaranteed within the age limits, usually for smaller amounts up to about $25,000. These policies carry a graded death benefit: pass away from natural causes in the first two to three years, and the company returns the premiums paid plus interest instead of the full amount. This type of insurance is built as a guaranteed yes for people the traditional market turns away, and for the right person it does exactly that job.

Four ways to get approved: fully underwritten, accelerated, simplified issue, and guaranteed issue.

Can you get life insurance with a pre-existing medical condition like melanoma or ADHD?

Yes, you can get life insurance with a pre-existing condition in most cases. Underwriting exists to price risk, not to reject it, and the great majority of health histories are insurable. The outcome turns on what the condition is, how well it’s managed, and how much time has passed since treatment.

Here’s the mechanism. Applicants are sorted into rate classes, from Preferred Plus at the top down through Standard. If a health history pushes you below Standard, companies use table ratings, and each step on the table adds roughly 25% to the standard premium. Read that again, because it’s the most reassuring sentence in this section: a table rating is an approval at a higher price, not a denial.

Two examples people ask me about. With a history of melanoma, underwriters look at the stage at diagnosis and the time since treatment ended; many survivors of early-stage skin cancer reach standard rates a few years after treatment. With ADHD, the impact is usually minimal when you’re otherwise healthy and your treatment is stable. Managed blood pressure and well-controlled diabetes follow the same pattern. Stability and time are what underwriters reward.

But here’s the part that matters most: every company weighs the same condition differently. The same file can get a table rating at one company and a Standard offer at another. So if your health history is complicated, getting a life insurance policy is usually a matter of finding the right company, not changing your story, and simplified issue life insurance may be the right path when speed matters more than squeezing out the lowest rate. This is exactly where an independent broker earns their keep; more on that below.

Worried a health condition will hold you back?

No-exam options · Real answers · The right company for your history

Can I get life insurance if I already have employer-provided coverage?

Yes, you can get life insurance even if you already have coverage through work, and for most people, keeping both is the smarter move. Your group coverage and an individual life insurance policy do different jobs, and the difference shows up at the worst possible times.

Group coverage is usually capped at one to two times your salary. Run that against the DIME math above and the gap is obvious: a $120,000 work policy on a $60,000 salary covers about two years of income and not much else. LIMRA finds that a quarter of insured Americans have only workplace coverage, and about one in three employees with workplace coverage aren’t even fully aware they have it.

The bigger problem is portability. Group life insurance is tied to your job. Leave, get laid off, or retire, and the coverage typically ends. Some plans let you port or convert it, but conversion is priced at your current age without the group subsidy, and it usually costs far more than the coverage you remember signing up for. An individual life insurance policy you own yourself travels with you through every job, every layoff, and into retirement, at the rate you locked in when you were younger and healthier.

The work policy that “seemed like a lot” at enrollment is usually one to two years of income, not ten.

And it usually stays behind when the job ends. Treat group coverage as a bonus on top of a policy you own, never as the plan itself.

What is the best type of life insurance for me?

The best type of life insurance for you depends on your stage of life and the job you need the money to do. There’s no single best policy. But there’s almost always a best policy for a situation, so here’s the honest map of your life insurance options.

Young family, biggest obligations of your life: term life, almost every time. It buys the most protection per dollar exactly when you need the most protection: the mortgage years, the kids-at-home years, the one-paycheck-doing-everything years. (Start with the term life guide.)

Lifelong need, estate planning, or your own final expenses: permanent insurance. Whole and universal life insurance never expire as long as they’re funded, build cash value, and fit needs without an end date, like leaving money behind no matter when you pass. (Start with the whole life guide.)

Buying for a parent: this one gets its own paragraph, because if you’re researching coverage for your mom or dad, you are far from alone. The fit is usually final expense life insurance: a small whole life policy, often called burial insurance or final expense insurance, sized to the funeral and the last bills, typically $10,000 to $25,000. These are usually simplified issue or guaranteed issue, so your parent skips the medical exam. A real shape I see often: a daughter owns and pays for the policy, her mother is the insured and answers the short health questions, and the daughter is the beneficiary. When the day comes, the funeral is handled and the family grieves without a bill collector in the room. (The full burial insurance and final expense guide covers it end to end.)

Tight budget: some coverage beats no coverage, every time. A smaller term policy protects your family today and locks in your insurability at today’s age and health. You can add more later as the budget grows.

Term or whole: which way do you lean?

Most buyers land on one of these two. Here’s the honest split.

- Are the primary earner with people depending on your paycheck.

- Carry a mortgage you want paid off if you’re gone.

- Are funding kids’ futures, from childcare through college.

- Want serious protection on a working budget.

- Want a payout guaranteed no matter when you pass.

- Are covering final expenses for yourself or a parent.

- Value fixed premiums and cash value over the lowest cost.

- Are doing estate planning with money meant to land tax-free.

When should I buy life insurance?

You should buy life insurance while it’s on your mind. That’s not a sales line; it’s how the product works. Your price is built from your age and health on the day you apply, and both of those move in one direction. Premiums creep up through your twenties and thirties, then climb hard after forty-five. The cheapest this will ever be is today.

But the price isn’t really the reason. Your insurability is.

I’ve had clients put this off for a month, then walk into what they figured was a routine checkup and walk out with a cancer diagnosis. For them, traditional coverage was off the table. Permanently. There’s no applying at yesterday’s health.

And more than once in my career, someone has passed away before I could even deliver their policy in person. The only comfort in those moments, and it’s a real one, was that the first payment had cleared and the policy was approved. The family was covered.

None of us can see our own timeline. What you can control is whether the protection exists before life decides for you. So if you’re going to purchase life insurance, do it before you lose momentum: get the quote, answer the questions, and let the approval do its work while you get back to that house at six in the evening.

Is “let me think about it” a reasonable answer, or am I being managed?

Say someone tells me they want to think about it. Here’s how I think it through: there are three things in that room, and all three are legitimate. There’s you, wanting time to decide, which is reasonable. There’s me, who would like to write the policy, and pretending that isn’t in the room would be dishonest. And there’s the part I have watched happen, where people say they will think about it, then don’t, and some of them pass away in the meantime with nothing in place. That happens every day in this country. None of those three makes anyone a villain.

What would change my answer: how long thinking about it actually means. A week is thinking. A year is a decision nobody said out loud, and a year of aging plus whatever the next checkup turns up has a real price attached to it.

It’s on your mind right now.

5–10 minutes · Down to the penny · While you have momentum

Life Insurance Plan Customization

You can customize a life insurance plan with riders: optional add-ons that bend the policy around your life. Some come free, some cost a little, and these six are the ones worth knowing.

Accelerated death benefit (living benefits) lets you access part of your own death benefit while alive after a qualifying terminal or chronic illness diagnosis, and many companies include a basic version at no extra cost. Waiver of premium steps in if you become totally disabled and can’t work: the company waives your payments and keeps the coverage in force, exactly when money is tightest.

Term conversion is the right to convert your term policy into a permanent policy like whole life, with no new exam and no new health questions. If your health changes mid-term, this is the safety valve: you can move to whole or universal life based on the health you had when you first applied. A child rider is one small addition to a parent’s policy that covers every eligible child in the household, usually convertible to the child’s own permanent policy in adulthood regardless of their health.

Return of premium refunds what you paid if you outlive your term. It raises the premium meaningfully, so it suits buyers who want something back more than they want the lowest cost. And guaranteed insurability is the right to buy more coverage at set points later without proving your health again.

Benefits of using an independent insurance broker

An independent insurance broker works for you; a captive agent works for one company. Per the NAIC, that’s the defining line between the two, and I believe every client relationship should start with that clarity. I represent you, not the carrier.

Why it matters in dollars: there’s no universal best. The best life insurance companies for one person are mediocre for another, because each company’s underwriting treats the same health history differently. One may charge extra for your blood pressure history; another shrugs at it. A broker who knows those appetites routes your application to the company most likely to say yes at the best class, before a formal decline ever lands on your record. Some of the strongest names in the business are mutuals, and the label matters less than people think: a mutual life insurance company is owned by its policyholders rather than shareholders, but whether a mutual insurance company or a stock company fits you better comes down to the product and the price.

My own standard is simple. I compare as many carriers as you qualify for through underwriting that are available in your state, across all their life insurance products. If the right answer for you is something I can’t sell, I’ll tell you that and point you in the right direction anyway. And remember the pricing fact from earlier: the broker costs you nothing extra. Same company, same policy, same price, with the whole market in view instead of one corner of it.

My father had a life insurance policy, and it bailed me out during one of the hardest stretches of my life. His passing was horrific, and I missed far more work than I ever expected to miss. For a long while I was keeping the lights on at two houses, his and mine, while his bills kept arriving like nothing had changed: the estate costs, the county fees, the legal bills, the medical co-payments, the funeral.

His policy carried all of it until I could square away his affairs. He thought of me, and it saved me. That’s what I want for your family: not paperwork, a landing. If this page helps you put that in place, it did its job.

Key life insurance terms, explained

Life insurance FAQs

The questions people ask me most, answered plainly.

Is life insurance worth it?

For anyone whose death would create a financial gap, usually yes. For most families, the cost of a term policy is small next to the hardship survivors face without one; nearly half of households say they’d struggle within six months of losing their main earner.

Can you have more than one life insurance policy?

Yes. Many people stack a work policy with an individual one, or layer several term policies of different lengths so coverage steps down as the mortgage and the kids’ needs shrink. Insurers simply check that your total coverage is reasonable against your income and obligations.

What is joint life insurance?

One policy covering two people, usually spouses. First-to-die versions pay when the first spouse passes; second-to-die (survivorship) versions pay after both and are mostly used in estate planning.

Are life insurance premiums tax-deductible?

For individuals, generally no. Personal premiums aren’t deductible, though the death benefit itself is generally income-tax-free to your beneficiary.

What happens if I outlive my term policy?

Coverage simply ends, with no payout and no refund unless you bought a return-of-premium rider. Before it ends, you can often convert it to a permanent policy or apply for new coverage.

What happens if I stop paying my premiums?

A term policy lapses after a grace period, typically about 30 days. Permanent policies can draw premiums from their cash value for a while, then lapse once it’s used up.

Does vaping count as tobacco for life insurance?

With most companies, yes. Nicotine use in the past 12 months, including vaping, usually triggers tobacco rates, commonly two to three times non-smoker pricing.

Can I name a minor child as my beneficiary?

You can, but it’s usually a mistake. Insurers can’t pay minors directly, which can force court involvement. A trust or a custodian under your state’s UTMA rules keeps the money moving to your child without a judge in the middle.

How long does a life insurance payout take?

Straightforward claims typically pay within a few weeks to two months once the certified death certificate and claim form are in.

What does life insurance not cover?

Common exclusions include suicide within the first one to two years, death during certain illegal acts, and sometimes specific high-risk activities listed in the policy. Misstatements found during the two-year contestability period can also jeopardize a claim, which is why honest applications matter.

Get a quote for life insurance

You’ve done the reading; the quote takes less time than the article did. Get a life insurance quote and in five to ten minutes you’ll know your exact price, down to the penny: real numbers for your age, your health, and the coverage your family needs, compared across the companies you qualify for. No pressure, and no markup for using a broker. I work for you, not the carrier. Let’s get your family covered while it’s on your mind.

Keep reading

Each type of life insurance has its own full guide. Pick your path.

This article is for educational purposes only and is not legal, tax, or financial advice. Life insurance availability, features, and pricing vary by person, company, and state, and all figures are estimates from the cited sources. Please speak with a licensed professional about your specific situation before making a decision.