Whole Life Insurance: How It Works, What It Costs, and Who It’s For

A plain-English guide to permanent coverage that lasts your whole life, locks your premium, and builds cash value you can use.

More Americans bought whole life insurance last year than at any point on record. Not because it’s trendy, but because it does something no other policy can promise in writing: coverage that lasts your whole life, a premium that never goes up, and a cash value that grows steadily no matter what the market does. This guide walks through how whole life insurance actually works, what it really costs, and how to tell whether it belongs in your family’s plan.

People land on this page from every direction. Some want a policy that can never expire on them. Some want to leave their kids something guaranteed and tax-free. Some are looking at a small policy for a parent or a grandchild, and some just want to know why anyone pays more for whole life when term is so cheap. Stay with me and you’ll have all of it: what the policy guarantees, how the cash value really works, what it costs at your age, and who it genuinely fits. I’ve helped families make these exact decisions since 2005. Let’s get you your answers.

- Whole life insurance is permanent. As long as the premiums are paid, it covers you for your entire life and pays whenever you die, not only if you die within a set window.

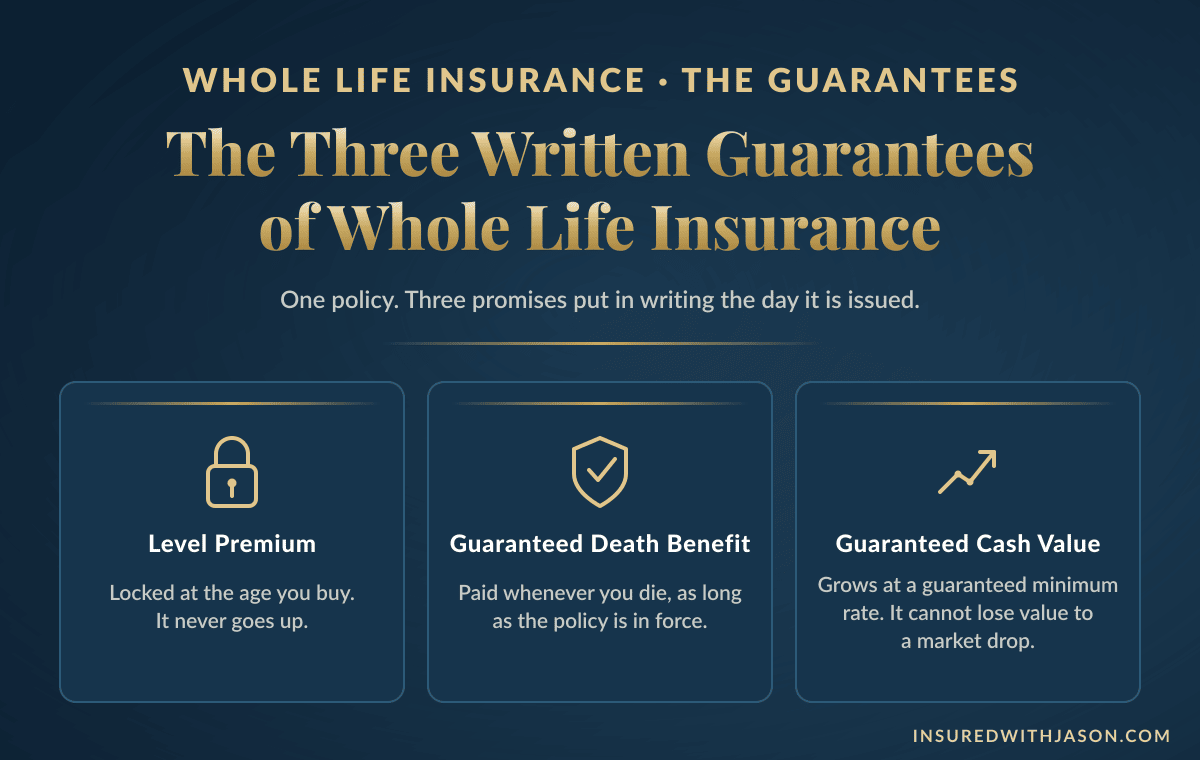

- Three guarantees are locked in writing the day the policy is issued: the premium never goes up, the death benefit never shrinks, and the cash value grows at a guaranteed minimum rate.

- The death benefit generally passes to your beneficiaries income-tax-free.

- Cash value is a living benefit. You can borrow against it or withdraw from it while you’re alive, but on a standard policy your family receives the death benefit and the insurer keeps the cash value. They aren’t added together.

- Whole life costs several times more than term for the same coverage, because the premium funds lifelong coverage and the cash account, not just temporary protection.

- Dividends on participating policies can grow both the cash value and the death benefit over time, but they’re never guaranteed.

- Whole life fits permanent needs: final expenses, a lifelong dependent, passing on tax-free money, and savers who want guarantees. For a temporary need on a tight budget, term often fits better.

What Is Whole Life Insurance?

Whole life insurance is designed to last your entire life: permanent coverage with a death benefit that pays whenever you die, not only if you die within a set window. It’s the oldest and simplest type of permanent life insurance (in older books you’ll even see it called life assurance), which is why you’ll sometimes hear it called ordinary life or straight life.

A term life insurance policy, the one most people compare it against, covers a fixed stretch of time, usually ten, twenty, or thirty years. Pass away during the term and it pays. Outlive it and the coverage ends, which is part of why term life policies cost so little. Whole life has no such window. As long as the premiums are paid, your family receives the death benefit whether you pass at 52 or 92.

Every whole life policy bundles two things into one life insurance contract. The first is the death benefit, the amount your beneficiaries receive when you die. The second is the cash value, a savings-like account inside the policy that grows over time and that you can use while you’re alive. Those two parts, and the guarantees wrapped around them, are what the rest of this page unpacks.

If you want the broader map of the types of life insurance first, start with the complete guide linked above, then come back. This page stays on one product, so you can learn what whole life insurance actually guarantees before anyone quotes you a price.

Every whole life contract carries the same three written guarantees, locked the day it’s issued.

How Does Whole Life Insurance Work?

A whole life policy works on three written guarantees, all locked in on the day it’s issued: the premium, the death benefit, and a minimum rate of cash value growth. Here’s what each one means for you.

Your premium stays level for life

The premium is set by your age and health on the day you apply, and it never goes up. Not when you get older. Not if your health changes. A 35-year-old who locks in a monthly premium pays that exact amount at 55 and at 85.

Here’s how the insurance company can promise that. In the early years, you pay more than it actually costs to insure you, and that extra money builds the policy’s reserves. In the later years, when insuring you costs more than your premium brings in, those reserves carry the load. You’re not getting a deal early and a penalty late. You’re paying one level price for your whole life, on purpose.

The guaranteed death benefit

The death benefit is fixed in the contract and guaranteed for life. It doesn’t shrink with the market or the economy, and your health after the policy is issued can’t touch it. When you pass, your beneficiary files a claim and receives the money, and under federal law it generally arrives income-tax-free.

How the policy builds cash value

Part of every premium goes into the policy’s cash value, where it grows tax-deferred at a rate the contract guarantees. It starts slow, because the early premiums also cover the cost of the life insurance protection itself, and then it compounds year after year. We’ll spend the whole next section on it, because it’s the feature people misunderstand most.

A whole life policy doesn’t run on forever without a finish line.

Modern policies “mature” at age 121. Live that long and your cash value will have grown to equal the death benefit, and the company pays the policy out to you, in person.

How Cash Value Works in a Whole Life Policy

Cash value is the savings side of a whole life policy: money that builds inside the contract, grows tax-deferred at a guaranteed minimum rate, and belongs to you while you’re alive. It’s also the most misunderstood thing in all of life insurance, so let’s take it apart piece by piece.

How cash value grows

Your cash value grows at a minimum rate written into the contract, and on a participating policy, dividends can grow it faster (more on dividends below). It can’t lose value to a market drop. The growth is modest in the early years and stronger every year after, and here’s the part I genuinely love about whole life: there’s no guessing about any of it. And since whole life is guaranteed top to bottom, your policy illustration shows your exact cash value for every year of your life, in black and white, including the year it crosses what you’ve paid in. You can read your own break-even point before you ever sign.

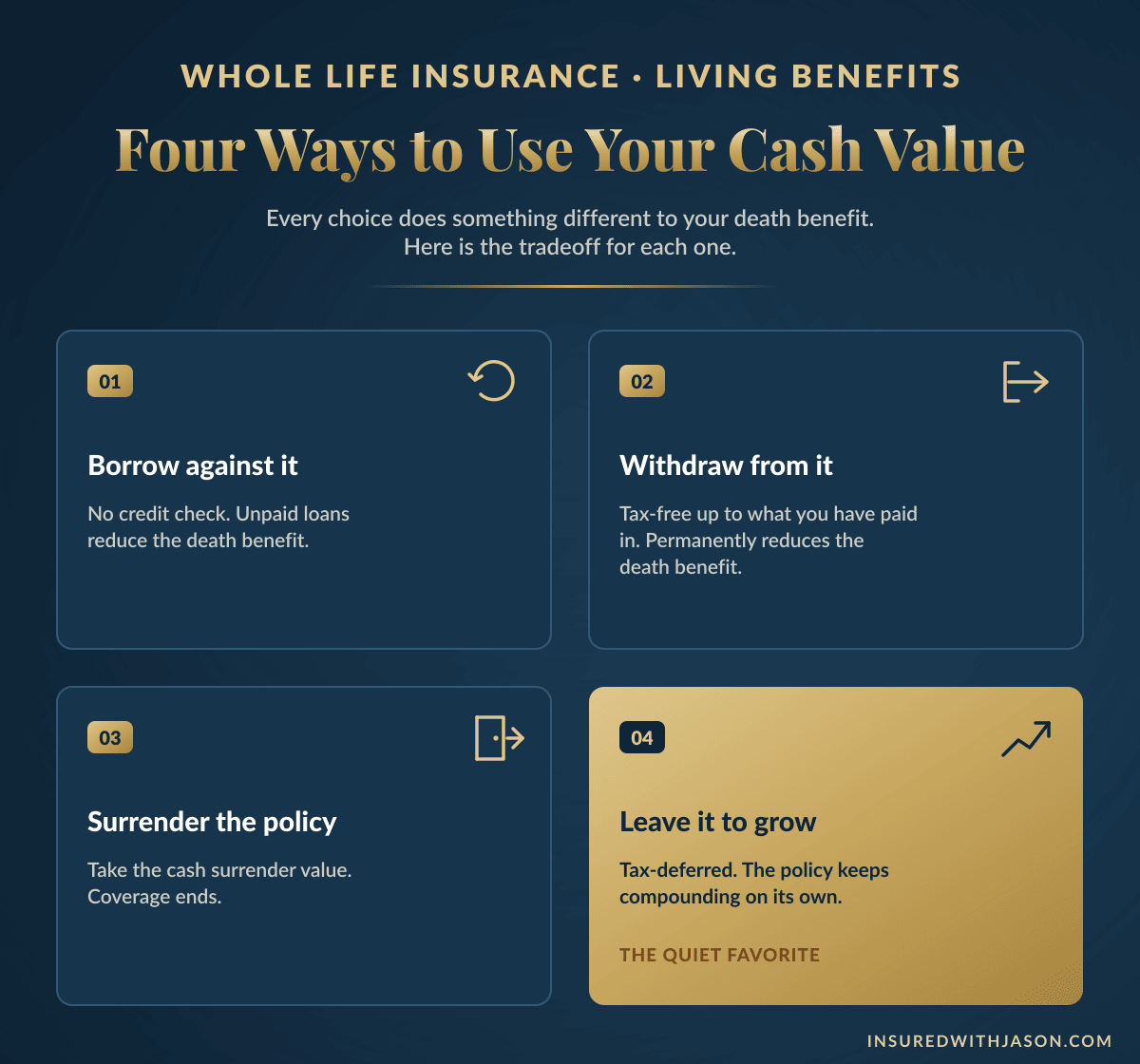

Borrowing against your policy (policy loans)

You can borrow against your cash value at any point in the life of the policy, with no credit check and no required payback schedule, and the loan isn’t taxable income while the policy stays in force. Two things deserve respect: interest builds on the balance, and any loan still outstanding when you pass is subtracted from the death benefit your family receives. Manage it, and a policy loan is one of the most flexible sources of money you’ll ever have. Ignore it, and it can quietly eat the policy. The warning box further down covers the one real trap.

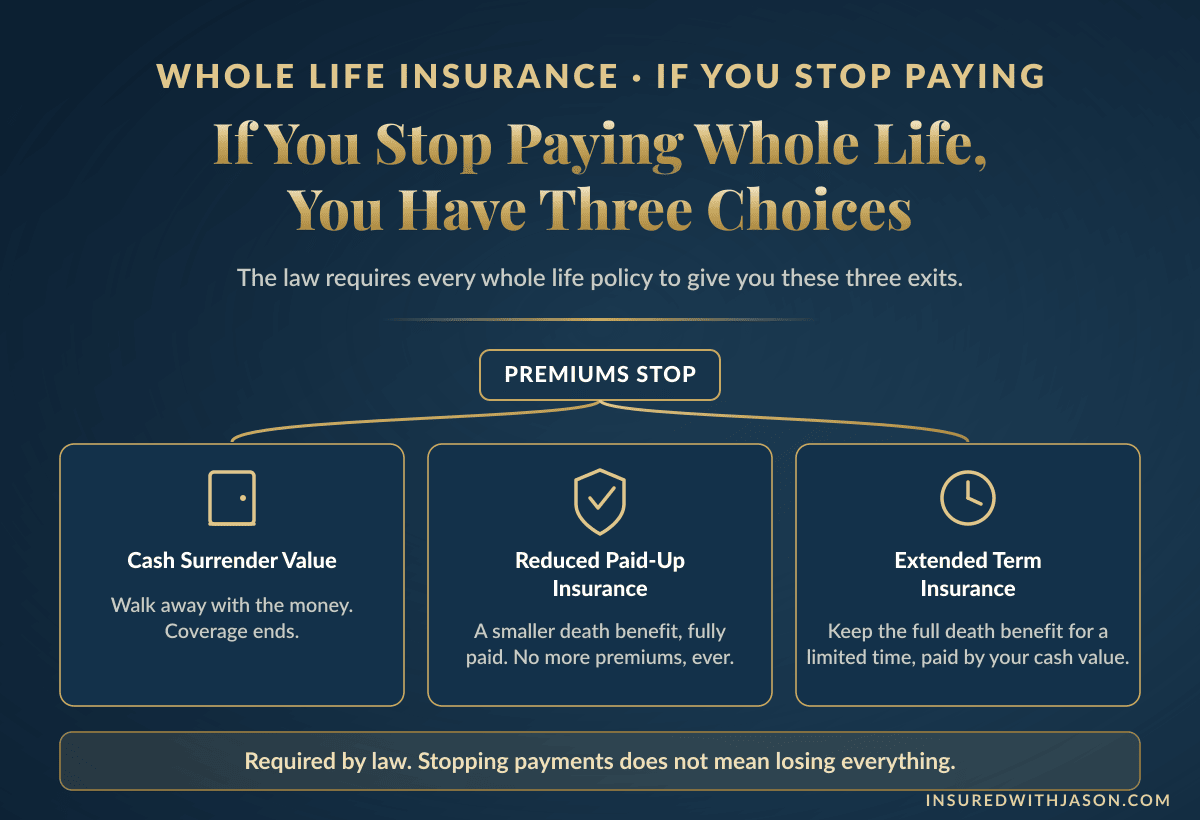

Cashing out or surrendering a policy

You can also cancel the policy and take the cash surrender value: the cash value of the policy minus any surrender charges and any loans you still owe. Cancel and the coverage ends, the death benefit is gone, and any gain over what you paid in is taxed as ordinary income. Surrendering in the early years usually means getting back less than you put in, which is why it’s a last resort, not an exit plan.

And if you ever simply can’t pay premiums anymore, you don’t lose everything. The law guarantees you three choices, called nonforfeiture options: take the cash, convert to a smaller policy that’s fully paid up forever, or keep the full death benefit for a limited stretch of time. Most people have never heard of them, and they’re some of the strongest consumer protections in the contract.

Stop paying and the law still guarantees you three choices. Losing everything isn’t one of them.

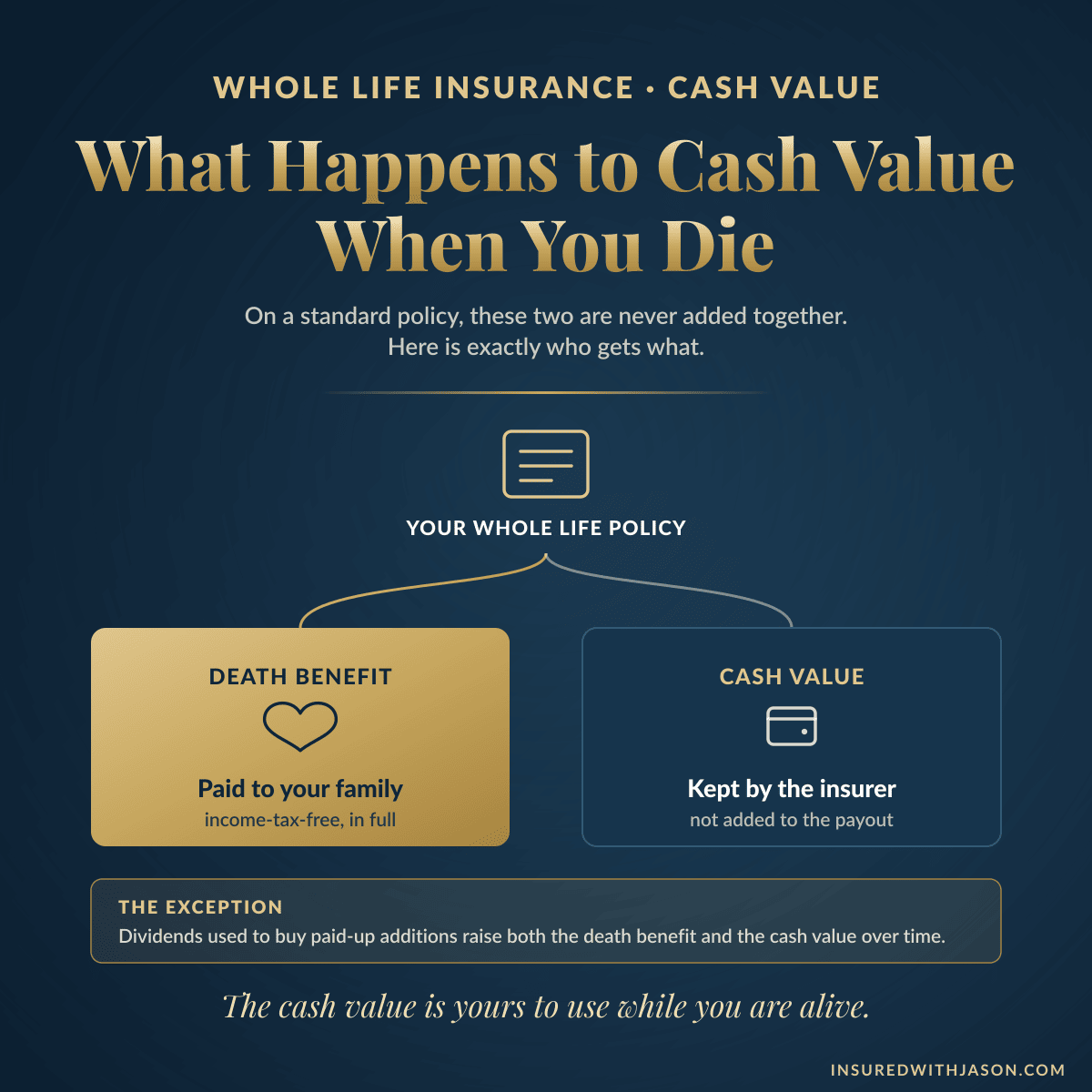

What happens to the cash value when you die

Here’s the fact that surprises more people than any other: on a standard whole life policy, your beneficiaries receive the death benefit, and the insurance company keeps the cash value. The two are not added together. The cash value was always the engine inside the policy, building toward the death benefit, not a separate pot stacked on top of it.

There’s one important exception. On a participating policy, dividends used to buy paid-up additions raise both the cash value and the death benefit over the years, so the check your family receives can grow well past the original face amount.

So the cash value is yours to use while you’re alive. That one sentence should shape how you own this policy.

The most misunderstood fact in life insurance: the death benefit and the cash value are not paid together.

Which raises the practical question: how do you actually use it while you’re alive? You have four moves, and each one touches the death benefit differently.

Four ways to use your cash value, and what each one does to the death benefit.

On a standard whole life policy, your family receives the death benefit and the insurer keeps the cash value. Knowing that before you buy changes how you use the policy while you’re alive.

Want to see your guaranteed cash value, year by year, in writing?

Real illustrations from across the market · Five minutes · No obligation

How Much Does Whole Life Insurance Cost?

For a healthy non-smoker, $100,000 of whole life insurance generally runs somewhere between $75 and $105 a month at age 30, and the range climbs with every birthday after that. These are estimates, not quotes; life insurance premiums are personal, and whole life premiums especially, because the price you lock is the price forever. Your exact price depends on your age, your health, and how the policy is designed. But the ranges below will put you in the right neighborhood.

What $100,000 of whole life insurance costs by age

Estimated ranges for healthy non-smokers. Your actual rate depends on your age, health, and policy design, and that’s exactly what a real quote is for.

What affects your premium

Your age is the single biggest factor. The price locks at the age you buy and never moves, which is why every year of waiting costs you for life. Your health comes next: insurers group applicants into health classes, and the best classes can pay meaningfully less than standard rates for the identical policy. Tobacco raises the price substantially, and yes, that generally includes vaping. Sex matters too; women typically pay less than men at every age, reflecting longer life expectancy.

Then come the design choices. The coverage amount works in your favor as it grows: the cost per thousand dollars of coverage actually falls as the policy gets bigger. And policy design moves the payment around: paying over a shorter window (a 10-pay or 20-pay design) means higher payments now and none later, while riders add cost for exactly what they add in protection.

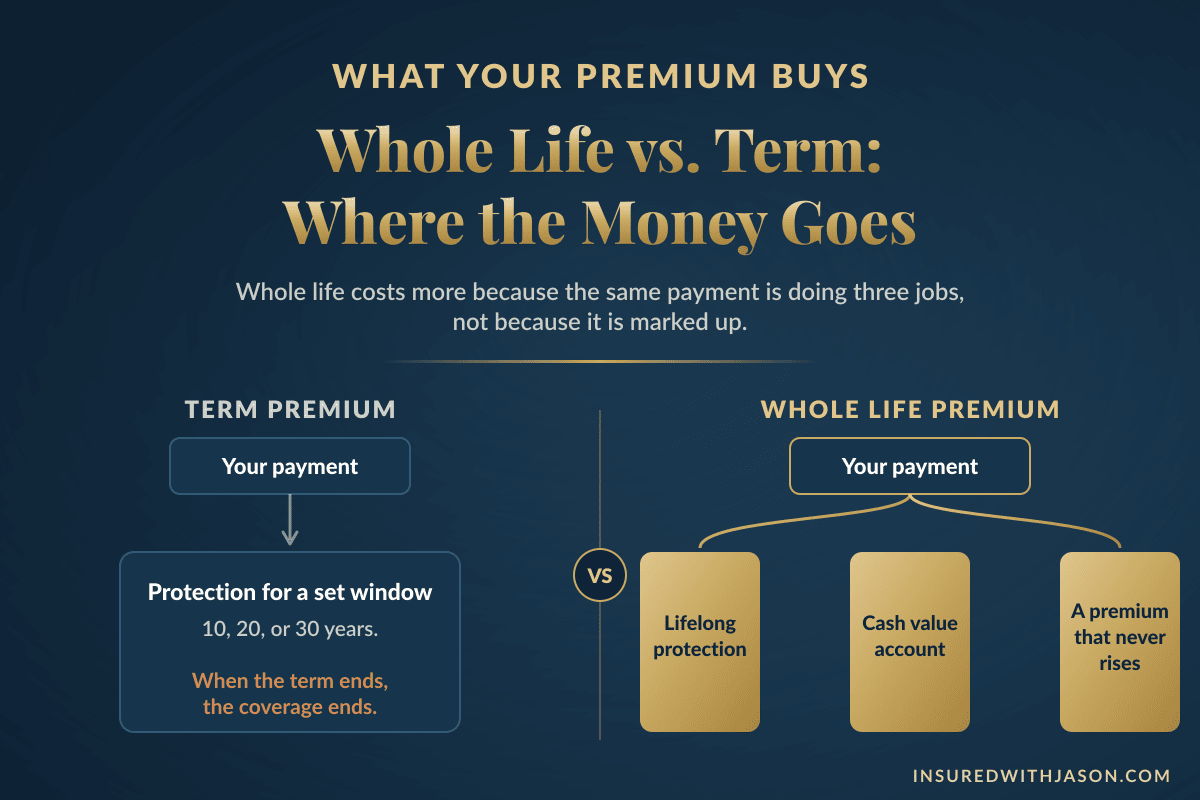

Why whole life costs more than term

Term is inexpensive because, most of the time, it never pays a claim; the majority of term buyers outlive their policies. Whole life is guaranteed to pay a claim eventually, on every single policy that stays in force. The only unknown is when. So the premium has three jobs instead of one: fund a death benefit that is certain to be paid someday, build your cash value, and lock the price for life. You’re not paying a markup. You’re paying for a promise with no expiration date.

A term premium does one job. A whole life premium does three. That’s the whole price difference.

The Benefits of Whole Life Insurance

The benefits of whole life insurance all trace back to one word: guarantees. Whole life insurance offers lifelong coverage, a locked premium, real tax advantages, and, on participating policies, dividends. Here’s what each of these life insurance benefits buys you in practice.

Coverage that can’t expire on you

Whole life coverage has no end date to outlive. It can’t run out at exactly the age when new insurance coverage gets expensive or hard to qualify for, and unlike group life through a job, it doesn’t end when the employment does. As long as you pay the premium, you’re covered. Period.

A locked premium that protects your insurability

Whole life insurance provides a second kind of protection most people miss: it protects your insurability. The person who buys at 30 in good health keeps that price and that policy even if their health changes completely at 45. The insurance company is bound to the original deal for life, and that’s worth more than most people realize until the year they need it.

Tax advantages of whole life insurance

Because whole life insurance is a permanent asset as well as a policy, it carries a tax profile few assets can match. The cash value grows tax-deferred, with no tax bill on the growth year to year. The life insurance death benefit generally passes to your beneficiaries free of income tax. Policy loans aren’t taxed while the policy stays in force. And withdrawals come out of your own contributions first, so you can typically take back what you’ve paid in before any gain is touched.

Dividends on participating policies

Participating whole life policies, usually issued by a mutual life insurance company (one owned by its policyholders), can pay an annual dividend. Dividends are never guaranteed, but when they’re paid, you choose what they do: take the cash, lower your premium, leave them to earn interest, or buy paid-up additions, the option that compounds both your cash value and your death benefit over time. That last choice is how a policy’s payout can quietly grow far past its original face amount.

What People Use Whole Life Insurance For

People put whole life insurance to work on a handful of jobs no other policy does as well, and almost all of them come down to certainty: a guaranteed amount, arriving income-tax-free, at exactly the moment it’s needed.

Protecting someone who will always depend on you

Some needs never end. A spouse who depends on your income, or a child with a disability who will need care long after your working years, can’t be protected by a policy with an expiration date. When the need is lifelong, the coverage has to be too.

Passing on tax-free money (and defusing an inherited tax bill)

Here’s a move I see more every year. A parent past retirement age is sitting on an IRA or 401(k) they don’t actually need; they live comfortably on everything else. The day their child inherits that account, every dollar that comes out gets taxed as the child’s ordinary income, and the bigger the account grows, the bigger that tax bill grows right along with it.

So the parent flips it. They take the money out now, pay the tax once at a rate they can see, and put what’s left into a whole life policy, often as a single payment. On the other end sits a guaranteed death benefit, larger than what they put in, arriving completely income-tax-free, whether they pass next year or in twenty. When the goal is moving money to the next generation, nothing else does this particular job quite like whole life.

The same thinking works for any money that’s already earmarked for someone you love, with two requirements: the person being insured consents, and health permits coverage. Sizes run the full spectrum here, from tens of thousands to well into the millions, because the move is the same at every size.

An IRA earmarked for their son was quietly becoming his tax bill.

A retired couple held an IRA that was always meant for their son, while they lived comfortably on everything else. Left alone, that account was a growing tax bill with his name on it. They repositioned it into a single-premium whole life policy instead. The tax got paid once, on their terms, and the policy guaranteed their son more than they put into it, income-tax-free, no matter when the day comes.

The relief in that conversation wasn’t about the math. It was about being finished.

A head start for a child or grandchild

Grandparents purchase whole life on grandchildren for the same reason in two very different sizes. Some commit serious money: a 10-pay policy funded with five figures a year for a decade, finished before the child starts middle school, and guaranteed to be a meaningful asset by the time they’re a young adult. I write those policies, and the families who buy them often do it for every grandchild. Others put in fifty dollars a month, or a thousand a year, because that’s what fits, and they’re doing the exact same smart thing.

Both are locking a premium at the cheapest age a human being will ever be, guaranteeing the child can carry coverage for life no matter what their health turns out to be, and starting a cash value that compounds for decades. With these policies, the death benefit is almost beside the point. The cash value is the gift.

Estate planning and liquidity

For most families, federal estate tax isn’t the worry anymore; the exemption now sits at $15 million per person. The real estate-planning job is liquidity: cash that arrives within weeks of a death so nobody is forced to sell the house, the land, or the business just to settle bills and split things fairly. Whole life insurance can help even the scales, too, when one child inherits the family business and the other doesn’t.

Covering final expenses

A traditional funeral with viewing and burial runs a median of about $8,300, and closer to $10,000 once a vault is added; cremation with a service runs about $6,280, per the National Funeral Directors Association. Small whole life policies, often $5,000 to $25,000, exist for exactly this bill, so it never lands on the people you love. And yes, an adult child can buy one on a parent, with the parent’s consent. We built a complete guide to burial and final expense insurance that covers it top to bottom.

The median cost of a funeral with viewing and burial — closer to $9,995 with a vault. Cremation with a service runs about $6,280.

Source: National Funeral Directors Association

Business uses

Whole life provides the permanence business planning depends on, and companies lean on it for two jobs. Key person coverage gives a company cash to stabilize and replace a vital owner or employee if they pass. And buy-sell funding guarantees the money is actually there for surviving partners to buy out a deceased owner’s share at the agreed price, instead of scrambling for it in the worst month of everyone’s life.

“Infinite banking”: the honest version

One more thing you’ll run into online: “infinite banking,” or “be your own bank.” The idea is to treat a specially designed whole life policy as your private source of financing, borrowing against the cash value to fund your life and paying yourself back. The mechanics are real; it’s the policy-loan feature you read about above, used aggressively. It can work. It’s also usually presented as simpler than it is, and it asks for heavy funding, real discipline, and years of patience before it hits its stride. I don’t push it, and I don’t dismiss it. If that strategy is what brought you here, I’m glad to walk through it honestly and see whether it actually fits your situation. I meet people where they are.

Types of Whole Life Insurance Policies

Every type of whole life insurance shares the same skeleton: lifelong coverage, a level premium, and guaranteed cash value. The whole life plans below are simply different ways of paying for the same promise.

Traditional level-premium whole life

The standard design, sometimes called straight life or level premium whole life: one fixed premium, paid monthly or annually for the entire life of the insured, with the lowest ongoing payment of the permanent designs. Traditional whole life is the baseline every other design builds on, and everything on this page describes it unless noted.

Participating (dividend-paying) whole life

Issued mostly by mutual insurers, participating policies are eligible for annual dividends. The dividends aren’t guaranteed, but applied to paid-up additions they can compound a policy’s cash value and death benefit well beyond the guaranteed columns. The guaranteed values still hold no matter what the dividends do.

Limited-pay whole life

Same lifetime coverage, compressed payments: ten years, twenty years, or paid-up at 65. Each payment is larger, the cash value builds faster, and then one day you’re done paying forever while the coverage runs on. The 10-pay is the workhorse behind those grandchild policies, finished and fully paid before the child is grown.

Single-premium whole life

One payment, fully paid forever, with substantial cash value from day one. One thing to know going in: the IRS treats nearly every single-premium policy as a modified endowment contract, a MEC. In plain English, if you pull money out during your life, gains come out first and get taxed, with a possible 10% penalty before age 59½. But the death benefit stays income-tax-free, which is exactly why single-premium remains the clean tool when the whole point is passing money on, not touching it.

Guaranteed issue and simplified issue whole life

These are the no-exam paths, built for people who can’t qualify for fully underwritten coverage or don’t want the process. Simplified issue asks a short list of health questions, skips the exam, and usually covers you in full from day one. Guaranteed issue asks no health questions at all, generally for buyers around 50 to 85, in smaller amounts, and usually with a graded period: pass away from natural causes in the first two to three years and the policy returns the premiums paid plus interest rather than the full benefit. If you can qualify for simplified issue, it’s usually the better buy. This is the final expense corner of whole life, and our burial insurance guide covers it in full.

Whole Life Insurance Riders

Riders are optional whole life insurance features that bend a policy around your actual life. A few are worth knowing by name before you shop.

Waiver of premium. If you become totally disabled, the company pays your premiums for you, and the policy keeps right on growing as if nothing happened.

Accelerated death benefit. Lets you access part of your own death benefit early if you’re diagnosed with a terminal illness, when the money can still help you. Many policies now include some version of this at little or no upfront cost.

Paid-up additions rider. The accelerator. It lets you put in extra money to buy small, fully paid slices of additional insurance that raise the cash value and the death benefit and earn their own dividends. If fast cash value growth is the goal, this is the rider doing the work.

Guaranteed insurability. Locks your right to buy more coverage at set future dates with no new health questions. On a child’s or grandchild’s policy, this is quietly the most valuable line in the contract.

Child and term riders. A child rider adds low-cost coverage for your kids, usually convertible to their own permanent policy later with no health questions. A term rider stacks temporary extra coverage on top of the whole life base for your heaviest years.

Whole Life vs. Term and Universal Life Insurance

Whole life, term, and universal life are the three life insurance products people weigh most often, they answer different questions, and the differences fit in one honest table.

| Whole Life | Term Life | Universal Life | |

|---|---|---|---|

| Coverage length | Your entire life | A set period, 10 to 30 years | Lifelong if properly funded |

| Premium | Level, locked for life | Level during the term, then ends or renews much higher | Flexible, adjustable |

| Death benefit | Guaranteed, fixed | Guaranteed during the term only | Adjustable, with fewer guarantees |

| Cash value | Yes, guaranteed minimum growth | None | Yes, growth varies by type |

| Dividends possible | Yes, on participating policies | No | No |

| Best for | Permanent needs, guarantees, legacy | Temporary needs, maximum coverage per dollar | Permanent coverage with flexibility |

General product features; specific terms vary by policy and insurer.

Whole life vs. term life

The honest comparison starts with the need, not the price. If what you’re protecting ends on a date, a mortgage, the years until the kids stand on their own, then term covers it for a fraction of the cost, and choosing it is the right call, not a compromise. If the need never ends, term’s expiration date is the risk, and whole life’s certainty is the point.

You’ll also hear “buy term and invest the difference.” For a disciplined investor who’s comfortable with market risk, it’s a legitimate strategy, and I’d never talk someone out of investing; I believe in it. Plenty of people land on a blend: a smaller whole life policy that’s guaranteed to be there at the very end, term to carry the heavy coverage through the working years, and investments for growth. The real decision was never whole life versus the market. It’s matching guaranteed money to permanent needs and growth money to long horizons.

Whole life vs. universal life

Whole life and universal life are both permanent; the difference is what you trade for flexibility. Universal life offers adjustable premiums, an adjustable death benefit, and cash value growth tied to current interest rates, a market index, or, in variable universal life insurance, market subaccounts. Funded well and watched closely, it can do good work. Underfunded, it can lapse. Compared to universal life in any of its forms, fixed, indexed, or variable life, whole life asks nothing of you but the premium; every other moving part is locked the day you sign. That’s the trade in one line: universal life hands you levers, whole life hands you certainty.

Is Whole Life Insurance Worth It? (Who It’s Right For)

Whole life insurance is worth it when the need is permanent, and it’s usually the wrong buy when the need is temporary. That one sentence settles most of the decision, so start there: will someone need this money whenever you die, or only if you die within the next stretch of years?

After the need comes your stomach for risk. Some people read the word “guaranteed” and exhale. They’re often the same people who like bonds, fixed rates, and paid-off houses, and a guaranteed product like whole life tends to fit them naturally. Others would rather take market risk for market returns, and for them, a smaller whole life policy to cover the permanent piece, term for the heavy years, and the difference invested is often the honest answer. Both buyers are right. The fully informed client is always right; that’s not a slogan, it’s how I run my practice. And whole life insurance may earn its place either way, as the whole plan or simply as its guaranteed corner.

Who whole life insurance is right for

Start with the need, then your comfort with risk. The lists below sort most situations honestly.

- Have someone who will depend on you for life: a spouse, or a child with a disability whose need has no end date.

- Want final expenses guaranteed to be covered, for yourself or for a parent who consents.

- Are moving money to the next generation and want it to arrive guaranteed and income-tax-free.

- Want to hand a child or grandchild lifelong insurability and decades of compounding.

- Value guarantees and fixed costs over market upside, and can carry the premium comfortably for the long haul.

- Own a business that needs key person protection or funded buy-sell money.

- Really need large income replacement for a set number of years on a working family’s budget — term protects the same family for far less.

- Would feel the premium as a strain. A policy that lapses early is the most expensive policy there is.

- Are chasing investment-grade returns. Guaranteed cash value growth is steady, not spectacular; it’s a guarantee, not a growth engine.

The loan-and-lapse trap, the graded-benefit window, and the MEC line.

Borrow heavily, stop paying, and let the policy lapse, and the loan you spent tax-free years ago can come back as taxable income in one ugly year; if you borrow, watch the balance. Die of natural causes inside the first two to three years of a guaranteed issue policy and it typically returns premiums plus interest, not the face amount; if your health qualifies you for simplified issue, take it. And overfund a policy past IRS limits and it becomes a modified endowment contract, permanently changing how money you take out gets taxed. Fine when the plan is to never touch it; a problem when it isn’t. Design this with someone who watches the line.

Not sure which side of these lists you’re on?

A ten-minute conversation · Your need and numbers first · No pressure

How to Get a Whole Life Insurance Policy

Getting a whole life insurance policy comes down to five steps, and the first one has nothing to do with insurance companies: get clear on the job the money has to do.

How to buy whole life insurance, in order

The job decides the amount, the amount decides the design, and the market decides the price.

- 1Start HereDefine the job

Final expenses, a lifelong dependent, a tax-free transfer, a grandchild’s head start, or simply guaranteed coverage you own forever. The job decides everything that follows.

- 2Get The Real NumberSize the coverage

Match the amount to your real insurance needs. For income protection, add up your debts, the years of income your family would need, the mortgage, and education costs. For final expenses, it’s the funeral plus loose ends. For a transfer, it’s the amount you want to move.

- 3Shape ItChoose the design

Pay for life or pay it up early, participating or not, and which riders earn their cost for your situation.

- 4Shop ItCompare the whole market

Pricing and underwriting vary widely across life insurance companies; the same health history can be priced very differently from one to the next. This is where an independent broker earns their keep.

- 5Make It RealApply truthfully and read what you bought

Full underwriting with an exam often wins the best price for healthy applicants; accelerated no-exam decisions now come in days; simplified and guaranteed issue cover the rest. Answer everything honestly — policies carry a two-year contestability window — then use your free-look period, usually ten to thirty days depending on where you live, to read the policy and return it for a full refund if it isn’t what was promised.

Why work with an independent broker

An independent broker works for you, not for any one insurance company. I compare the same coverage across the whole market, because the difference between carriers on the identical person can be the difference between a policy you keep for life and one you resent. I’m licensed in most states, and I sit on your side of the table. That’s the whole pitch.

When Is the Best Time to Buy Whole Life Insurance?

The best time to buy whole life insurance is the youngest, healthiest version of you that will ever exist, and that’s the one reading this page. Whole life insurance rates lock at your current age and never move, so every year of waiting raises the locked price permanently and gives your health one more year of chances to change the offer. The three promises at the top of this page never change with age. Only the price does. Most people find whole life a few years later than they wish they had.

Converting term life to whole life

Already own term insurance? Most term policies carry a conversion privilege: a window during which you can convert some or all of your coverage to whole life with no new exam and no new health questions, priced at your current age. If your health has changed since you bought the term policy, this can be the single most valuable feature you own. The catch is the deadline. Many policies cut conversion off after a set number of years or at a set age, and people routinely discover the window after it’s closed. If you own term insurance, find your conversion deadline this week. It’s on your policy’s schedule page, or send it to me and I’ll find it with you.

I’ve sat on every side of this table. I’ve been the broker, I’ve been the client, and I’ve been the family member standing in the gap when everything went wrong at once. What all of it taught me is simple: the product is never the starting point. The person is. When someone sits down with me, I want to understand the family, the money, and the job that money has to do long before I say the words “whole life.” Sometimes the answer is the policy on this page. Sometimes it’s term, and I’ll say so. The only outcome I’m loyal to is you understanding exactly what you own and why you own it. That’s what I’d want for my own family, so it’s what you get.

Whole life insurance: frequently asked questions

The questions people ask most when they want to learn more about whole life insurance, answered plainly.

Is whole life insurance worth it?+

Often, yes, when the need is permanent: final expenses, a lifelong dependent, passing on tax-free money, or guaranteed coverage you can never outlive. It’s often not the best buy when the need is temporary and the budget is tight; term covers those years for far less.

How much does whole life insurance cost?+

As an estimate, $100,000 of coverage for a healthy non-smoker runs roughly $75 to $105 a month at age 30, $110 to $140 at 40, $175 to $215 at 50, and $290 to $325 at 60. Your exact rate depends on your age, health, and policy design.

Can you borrow money from a whole life policy?+

Yes. You can borrow against your cash value with no credit check and no set payback schedule. Interest accrues on the balance, the loan isn’t taxed while the policy stays in force, and any unpaid balance is subtracted from the death benefit.

Can you cash out a whole life policy?+

Yes. Surrendering the policy pays you the cash surrender value: the cash value minus surrender charges and any outstanding loans. The coverage ends, and any gain over the premiums you paid is taxed as ordinary income. Surrendering early usually returns less than you paid in.

What’s the difference between whole life and term life insurance?+

Term covers a set window of years, builds no cash value, and is the least expensive way to buy coverage. Whole life lasts your entire life, locks the premium forever, and builds guaranteed cash value, at a cost several times higher for the same amount of coverage.

Is the whole life death benefit taxable?+

Generally, no. The death benefit passes to your beneficiaries free of income tax. Interest earned on installment payouts is taxable, and only estates above the federal exemption, now $15 million per person, face estate tax.

What happens if I stop paying my premiums?+

You don’t automatically lose everything. The law guarantees nonforfeiture options: take the cash surrender value, convert to a smaller fully paid-up policy, or keep the full death benefit as extended term coverage for a limited time.

What happens to my cash value when I die?+

On a standard policy, your beneficiaries receive the death benefit and the insurer keeps the cash value. Paid-up additions are the exception; they grow the death benefit itself over time. The cash value is built to be used while you’re alive.

What are the pros and cons of whole life insurance?+

Pros: it can never expire on you, the premium never rises, the cash value growth is guaranteed and tax-deferred, and the death benefit is generally income-tax-free. Cons: it costs several times more than term, cash value builds slowly in the early years, and surrendering early usually loses money.

Let’s find your whole life number

You’ve now seen how whole life insurance works, what it costs, and the jobs it does better than anything else. The one thing this page can’t show you is your own number, and the fix is to get a quote built on your real age and health, which takes about five minutes. Send me the basics and I’ll shop the whole market for your age, your health, and your goal, with the guarantees in writing. No pressure, no homework. Just your actual answer.

This article is for educational purposes only and is not legal, tax, or financial advice. Coverage, costs, and rules for life insurance plans vary by person, company, and state. Figures shown are estimates or medians from cited sources, not quotes or guarantees. Please speak with a licensed insurance professional about your specific situation before making a decision.